As the top-performing asset class of the 21st century, gold is trading at an all-time-high of more than US$2,000 per ounce, with the current macroeconomic climate set to propel demand for the metal over the long term. Key factors include:

- Gold’s millennia of history as a source of value acting as a hedge against inflation, which only returned below 3 per cent in Canada in January 2024 after surpassing 8 per cent in 2022, exacerbated by pandemic stimulus and global, vaccine-enabled returns to normality. The precious metal returned more than 530 per cent from 2000 to 2022.

- Robust central bank purchases in the pursuit of balance sheet stability and to offset monetary policy-induced fiat currency devaluation, with the institutions having been net buyers since 2010 to the tune of more than 7,800 tonnes.

- Gold’s history making it a popular safe-haven during periods of market volatility, as well as times of heightened geopolitical risk, such as the present moment.

While the metal has rewarded long-term investors with outsized returns, the same cannot be said for junior gold stocks, with the VanEck Junior Gold Miners ETF yielding -68.89 per cent since 2009, and standout explorers dragged down with the riffraff, because of risk-off sentiment as high interest rates continue to put the brakes on the once white-hot post-pandemic global economy.

It’s precisely because junior gold stocks offer higher leverage to their target commodity thanks to an ability to generate profits from the otherwise yield-free metal, as well as the higher risk-reward trade off associated with companies in early-stage development, that retail and institutional investors have fled the space for safer assets. This has left experienced allocators to peruse the all-time-lows for unrecognized value.

A key name to consider under this thesis is Goldshore Resources (TSXV:GSHR), market cap C$23.37 million, an undervalued junior gold stock with a heavy-hitting management team, whose robust resource development at its 100-per-cent-owned Moss gold project in Ontario has been met with a 50 per cent drop in share price year-over-year, and an 86.15 per cent loss since drilling began in 2021, severely discounting the miner against its peers, representing but the tip of the iceberg in a generational opportunity in the junior gold space.

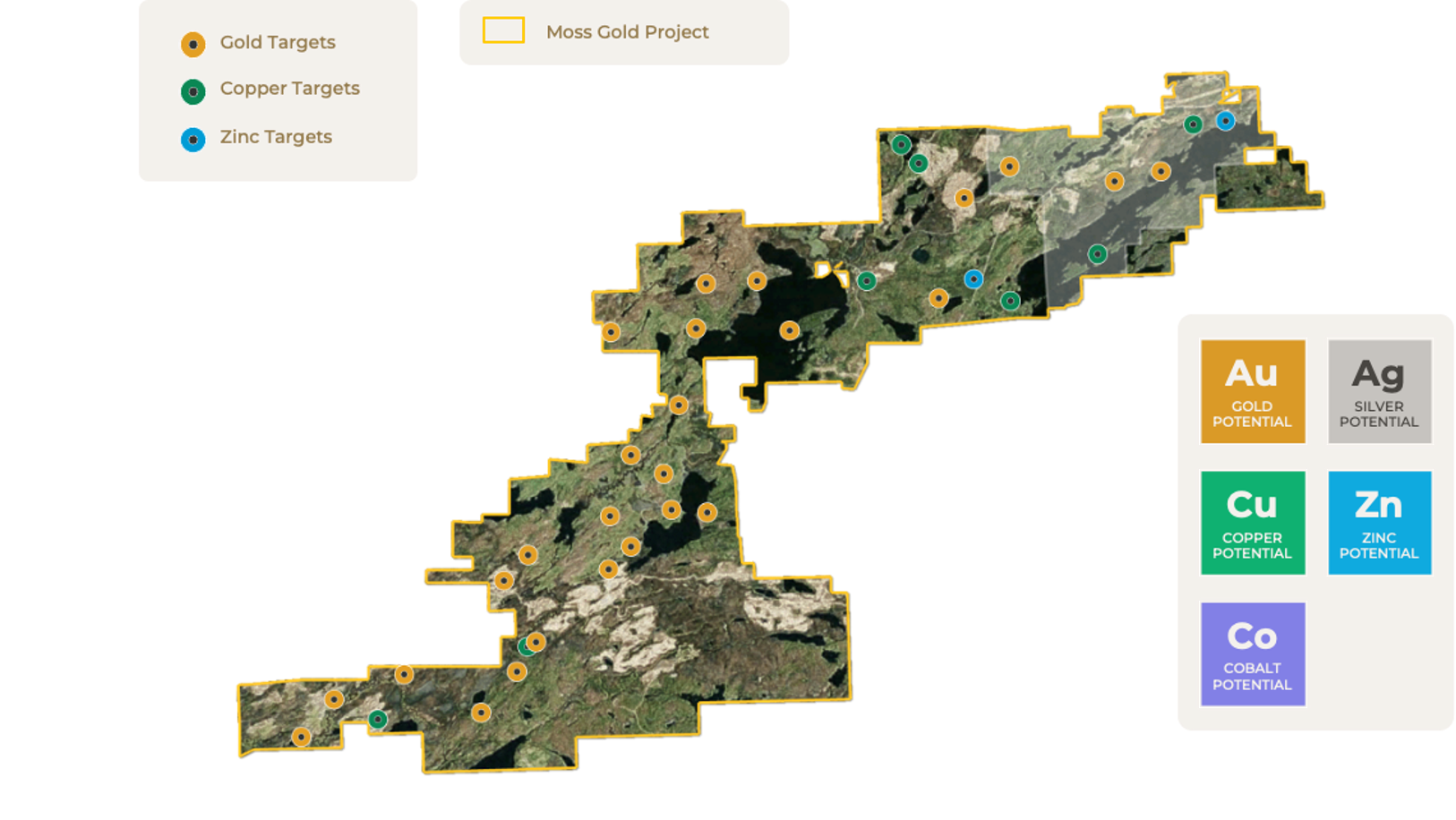

The Moss gold project

Backed by extensive historical exploration dating back to the 1800s, and three years of high-grade drilling during Goldshore’s recently completed 100,000 m campaign, the Moss gold project is composed of no less than 36 satellite targets prospective for gold, silver, copper, zinc and cobalt across a more than 35 kilometre mineralized trend.

Drilling is most recently highlighted by 1.34 g/t gold over 90.95 m (2022) and 2.17 g/t gold over 50.35 m (2023), with results as high as 6.30 g/t gold over 56.85 m (slide 24), and multiple high-grade structures to be explored in 2024 and 2025, including five promising gold trends identified during a summer 2023 field program.

The project enjoys access to all the infrastructure required to support a district-scale mining camp, including readily accessible talent, water, natural gas, rail transport and cheap electricity priced at C$0.10/kwh, with the undervalued junior gold stock well-financed for further resource delineation.

Moss’ 2024 mineral resource estimate

Goldshore’s history of economical drilling grades is most recently highlighted by a 2024 mineral resource estimate (MRE), which details an open-pit mining scenario at the Moss project’s Moss deposit, and the East Coldstream deposit 13 km to the northeast, two structurally controlled targets with a combined 5.7 km of modelled strike length.

The MRE – which relied on 538 drill holes that intersected the Moss deposit, and 156 that intersected the East Coldstream deposit – estimates the deposits to contain:

- Indicated mineral resources of 1.535 million oz. grading 1.23 grams per tonne gold (g/t Au) within 38.96 million tonnes, representing 23 per cent of total resources.

- Inferred mineral resources of 5.198 million oz. grading 1.11 g/t Au within 146.24 million tonnes.

- These include 3.35 million oz. of high-grade gold grading 1.84 g/t gold, and represent an overall grade increase of 11 per cent compared with the 2023 MRE, which estimated an inferred resource of 6 million oz. of gold grading 1.02 g/t gold.

- Preliminary metallurgical results came in at a spectacular 93 per cent gold recovery for the Moss deposit and 98 per cent for the East Coldstream deposit using a flotation-regrind-leach process, including gold recoveries between 53-64 per cent supporting a low-recovery heap leach solution for low-grade mineralization to bolster production and reduce tailings.

The shears that contain Moss deposit mineralization extend well beyond the MRE’s parameters, as historical drilling has intercepted gold mineralization over a total strike length of 8 km, which the undervalued junior gold stock validated during 2023 soil geochemistry and structural mapping. To date, the company has identified and modelled about 4 million tonnes of gold mineralization inside the conceptual open pit for future resource development on the road to another MRE slated for year-end 2025.

Similarly, the shears in East Coldstream extend far below the reported MRE and are distinguished by a shallow easterly plunge tested at depth by Goldshore, with ample potential for additional gold mineralization.

The MRE assumes a reasonably conservative sales price of US$1,850 per oz. of gold, creating just under a 10 per cent margin from the current price of US$2,019 as of Feb. 27, and uses improved modeling that shows 94 per cent of the tonnage (96 per cent of metal content) stem from high-grade gold-hosting shear zones, which is up from only 35 per cent in the 2023 MRE.

The Moss and East Coldstream deposits encompass only a fraction of the entire Moss gold project, whose five aforementioned trends, as well as eight well-drilled candidates for resource development (slide 15), could mean millions in potential gold ounces to be discovered and efficiently brought to market.

Considering the company has drilled less than 10 per cent of identified targets on its land package, all mineralized zones within the Moss gold project remain open to potential expansion, and plans are in place to relog and resample historical drill holes over the next few years, we support a recent statement by Peter Flindell, Goldshore’s vice president of exploration, who believes that Moss is “a much bigger mineralized system than is appreciated.”

A tried-and-true management team

Moss owes its prospective early-stage development to a team of mining industry veterans with shareholder-aligned interests, to the tune of 26 per cent insider ownership, and development and production experience that spans the mining life cycle from beginning to end.

Brett Richards, Goldshore’s interim chief executive officer, has built a more than 34-year career in mining and metals across financing, development, senior level operations and M&A, including stints as CEO of Roxgold and a senior executive at Kinross Gold and Katanga Mining. He views Moss as “a sector anomaly,” according to the 2024 MRE news release, which will yield “top-quartile grade and top-quartile size and scale within its comparable peers.”

Richard’s leadership is complemented by Flindell’s 35 years of experience in mineral exploration and feasibility studies, including leading teams through the discovery, development and expansion of numerous gold and copper mines in Southeast Asia, Central Asia, West Africa, Central Africa, Europe and Central America. His most notable tenures include 12 years with Newmont Mining, 11 years with Avocet Mining and eight years with Signal Delta.

Keeping the books in order, Marlis Yassin, CPA, CA, Goldshore’s chief financial officer, rounds off the senior management team with more than 15 years of experience working in her field across mining, technology and industrial companies, including senior finance management positions at public mid-tier mining companies and a long tenure at Deloitte providing reporting, advisory and assurance services to publicly traded natural resources companies.

Goldshore’s directors and strategic advisors are equally, if not more impressive in their laurels, as highlighted by director Joanna Pearson, the current CFO of the C$5.53 billion market cap Endeavour Mining (TSX:EDV); chairman Galen McNamara, the CEO of Summa Silver (TSXV:SSVR); and director Shawn Khunkhun, the CEO of Dolly Varden Silver (TSXV:DV), who has raised more than US$1 billion in equity for resource companies over the past 17 years.

Supported by strong drill and engineering results, as well as a seasoned executive team that knows how to build projects from the ground up, it’s no surprise that Goldshore’s value proposition has attracted 29 per cent institutional ownership, including Sprott (TSX:SII), Wesdome Gold Mines (TSX:WDO) and Ninepoint Partners, de-risking allocations from retail investors.

A stock with clear signals for considerable upside

Goldshore stock’s more than 86 per cent drop has caused Moss to be severely undervalued against comparable projects (slides 28-29) – such as Kinross’ Great Bear (2.7 million oz. M&I), B2Gold’s Back River (6.3 million oz. M&I), Calibre Mining’s Valentine (4 million oz. M&I), Mayfair Gold’s Fenn-Gib (3.062 million oz. M&I) and Perpetua Resources’ Stibnite (6.034 million oz. M&I) – which trade or were acquired for anywhere between 6x and 81x Goldshore’s market cap/mineral resources.

Additionally, Moss’ resource grades are in the first quartile among peer open-pit projects near or in production (slide 31) – including New Gold’s Rainy River, IAMGOLD’s Côté Lake, Agnico Eagle/Yamana’s Canadian Malartic, Argonaut Gold’s Magino and Equinox/Orion’s Greenstone – affording it a leading economic profile from an earlier development stage at an out-of-favour price.

These price-value dislocation metrics, supported by gold’s macro tailwinds, solid exploration and engineering results, and established leadership, are icing on the cake in our substantiation of a long-term investment in Goldshore. The undervalued junior gold stock’s case is strengthened as it further expands mineralization and enhances its prospects for a re-rating through ongoing environmental baseline studies and another MRE slated for year-end 2025, followed by a preliminary economic assessment, eventual feasibility work, permitting and mine construction or an asset sale.

Readers under-allocated to the mining sector would be best served by running Goldshore through a full due diligence process while market sentiment remains pessimistic, and entry points retain the potential for outsized returns.

Join the discussion: Find out what everybody’s saying about this undervalued junior gold stock on the Goldshore Resources Bullboard, and check out the rest of Stockhouse’s stock forums and message boards.

This is sponsored content issued on behalf of Goldshore Resources, please see full disclaimer here.