Almonty Industries and the Leap into Profitability

The latest quarterly figures confirm that Almonty has left the capital-intensive project development phase behind. In the first quarter of 2026, the company recorded a significant increase in operating cash flow to CAD 9.7 million. It optimized its operating margin to 31% through efficiency gains at its existing mines. Due to the ramp-up at Sangdong, which is not yet reflected in the quarterly figures, the coming quarters are likely to deliver even better results. The company’s capital position is also impressive. “With cash of CAD 259.9 million and working capital of CAD 169.5 million, we continue to have a solid capital base to drive our extensive development pipeline,” said Interim CFO Guillaume de Lamaziere in a company statement.

Almonty is now benefiting from the scaling of its operational capacities, particularly through progress at the Panasqueira mine in Portugal and the start of production at the flagship Sangdong project in South Korea. Almonty significantly increased its cash flow in the first quarter of 2026, paving the way for further growth. The move to the US has proven to be a masterstroke. Almonty has now finally arrived in the “Land of Opportunity” and is directly benefiting from the US government’s subsidy programs aimed at securing critical raw materials. Analysts at renowned investment banks such as Bank of America and Oppenheimer are currently pointing out that Almonty enjoys preferential status in government procurement decisions due to its presence in the US.

The Strategic Alliance: Lockheed Martin and Bank of America

The depth of Almonty’s integration into the US defence ecosystem is evident in its close ties to industrial heavyweights and financial institutions. At a digital event hosted by Bank of America on Wednesday, CEO Lewis Black will once again highlight Almonty’s role as a guarantor of the US’s security of supply for the key raw material tungsten. In its latest commentary on Almonty, Bank of America highlighted that Almonty’s valuation does not yet fully reflect the potential of the Sangdong mine, which, upon completion, is expected to cover approximately 40% of the tungsten supply outside of China.

For end-users such as Lockheed Martin, a reliable partner like Almonty is vital. Tungsten is irreplaceable for vehicle armour, the manufacture of turbine components, and, above all, for modern precision munitions. Almonty serves as a robust link in a supply chain that is increasingly breaking free from dependence on China. Since this will also be required by law in the US starting in 2027, there is no way around Almonty. The fact that the only Western tungsten producer bringing significant new capacity to market in 2025 and 2026 has long-term off-take agreements—often spanning decades and with no upper price cap—provides planning security for both the company and its customers. This reliability, combined with high-grade material and conflict-free, sustainable mining, defines Almonty’s unique profile.

Analyst Comments: Focus on Undervaluation and the Tungsten Supercycle

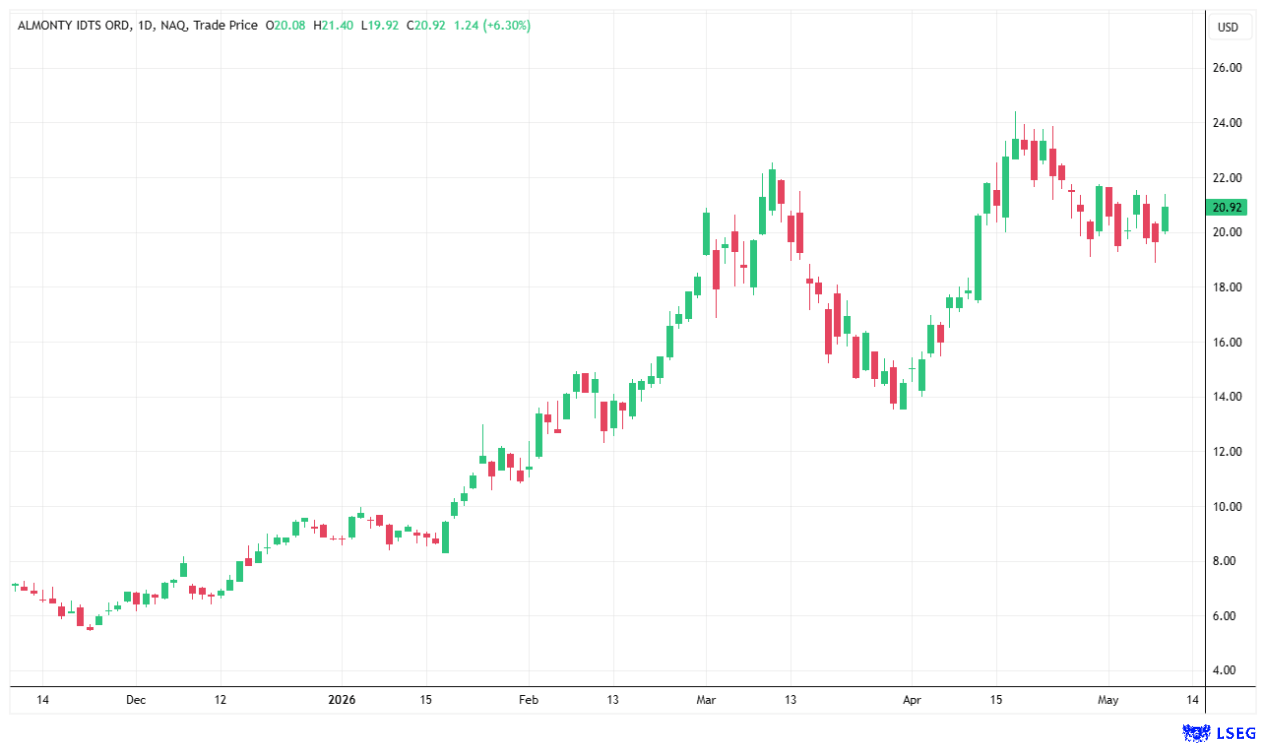

Analysts’ views on the company’s current position are clear: the combination of rising tungsten prices and falling production costs creates enormous leverage. Bank of America emphasizes that tungsten is currently undergoing a supercycle similar to those seen with lithium and uranium, as global reserves outside China are limited. Almonty controls the largest and highest-quality deposits in the Western world, securing the company a near-monopoly position. Analysts particularly highlight the company’s risk management. By diversifying its mine locations across different continents, Almonty has built a robust portfolio. Bank of America’s experts, therefore, see significant upside potential in the current market capitalization once full production capacity is reached in South Korea. Bank of America’s new price target for Almonty shares is USD 23.

Conclusion: Almonty as a Winner of the New US Industrial Policy

Almonty is not just a mining company, but one of the key players in the new Western industrial policy. The move to the US was the final piece of the puzzle to benefit from government support and demand from the US defence industry. Investors looking to bet on critical mineral sovereignty will find a unique opportunity in Almonty. Tungsten is scarcer than ever, and Almonty is the only major Western producer expanding its capacity. Added to this is proven expertise in this complex element, which is also essential for future-oriented industries such as aerospace and fusion energy. According to its own statements, Almonty operates the world’s most advanced tungsten laboratory in Portugal.**

Following the release of its quarterly results, Almonty is likely at the beginning of a long-term growth phase characterized by scarcity and exploding demand from the high-tech sector. The company has done its homework. Production is underway, financing is secured, and renowned customers in the defence and aerospace sectors are eager for reliable supplies. In a world where the supply of critical raw materials determines victory or defeat, Almonty holds the tungsten trump card.

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as “Relevant Persons”) currently hold or hold shares or other financial instruments of the aforementioned companies and speculate on their price developments. In this respect, they intend to sell or acquire shares or other financial instruments of the companies (hereinafter each referred to as a “Transaction”). Transactions may thereby influence the respective price of the shares or other financial instruments of the Company.

In this respect, there is a concrete conflict of interest in the reporting on the companies.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is also a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.

Stockhouse does not provide investment advice or recommendations. All investment decisions should be made based on your own research and consultation with a registered investment professional. The issuer is solely responsible for the accuracy of the information contained herein. For full disclaimer information, please click here.