When it comes to producing and refining critical minerals underlying renewable energy technology, China is the clear leader, dominating the market for more than a dozen commodities, granting it outsized control over the future of our shared environment.

Given the nation’s tendency to restrict the flow of its resource base and ally itself with threat-prone governments, including Russia, Iran and North Korea, it stands to reason that Western nations are actively diversifying their critical minerals supply chains towards more reliable jurisdictions.

This article is disseminated in partnership with AE Fuels Corporation. It is intended to inform investors and should not be taken as a recommendation or financial advice.

Chief among the countries catalyzing Western critical mineral independence is the United States, China’s top economic competitor, which has made a determined push to bolster production and processing capacity over the past few years, spearheaded by:

- US President Trump’s March 2025 executive order to expedite domestic critical minerals production.

- Project Vault, an initiative to establish a US critical minerals reserve announced in February 2026 bankrolled by a US$10 billion loan from the Export-Import Bank of the United States.

- Up to US$500 million from the US Department of Energy to support critical minerals processing and battery materials manufacturing to reduce reliance on hostile foreign nations.

With growth runways de-risked by robust funding opportunities and a list of officially recognized critical minerals published in November 2025, explorers, developers and producers advancing projects with the potential to strengthen the US supply chain are as in-demand as they have ever been.

We can see this trend in effect in the growing number of projects accepted for expedited permitting under the US government’s FAST-41 program, making it high time for investors to align themselves with companies following value-maximizing pathways as they diligently usher their projects across the mining lifecycle.

Introducing AE Fuels Corporation

A junior mining company well worth highlighting is AE Fuels Corporation (TSXV:AEF | OTCQB:NRGFF), market capitalization C$8.72 million, whose stock has traded in a narrow band since listing in December 2025, despite making consistent progress towards critical minerals production and refining, granting investors undervalued, pure-play exposure to the renewable energy transition.

The company is actively advancing two projects in tier-one mining jurisdictions, including its flagship South Woodie Woodie manganese project in Western Australia and the Fluorite Ridge fluorspar project in New Mexico. Both projects are prospective for battery minerals, are designated as critical by the US, EU and Australia, and lie at the heart of the Western world’s shift away from fossil fuels towards a cleaner, more energy-efficient future.

The South Woodie Woodie manganese project

Manganese is mostly used as a desulphurizing agent in the production of steel, ensuring a product whose toughness, ductility and corrosion resistance aligns with industrial needs. But manganese has been undergoing a paradigm shift as of late as a key component in lithium-ion batteries – in both electric vehicles (EVs) and energy storage systems – enhancing energy density, performance and safety, all while lowering costs. According to Visual Capitalist, a typical EV battery requires on the order of 10 kilograms of manganese to ensure competitive performance.

This critical mineral’s ability to support long duration energy storage, in effect across a variety of battery chemistries, and especially relevant for intermittent sources of renewable energy, including wind and solar, makes China’s 96 per cent control of high-purity manganese sulphate monohydrate (HPMSM) refining capacity a particular matter of concern. This is markedly true for the US, whose near-complete reliance on imports for its manganese supply, both raw and refined, places its industrial development at the mercy of third parties, including China, its primary economic competitor, whose export controls on cathode technologies are currently under a one-year pause, though prohibitive licensing requirements remain in place.

That said, where there is an unmet need, there are likely new ventures attempting to satisfy it, and the US manganese supply chain is no exception, strongly incentivizing mining companies to step up to the plate, take advantage of billions in available government funding and reinforce national security.

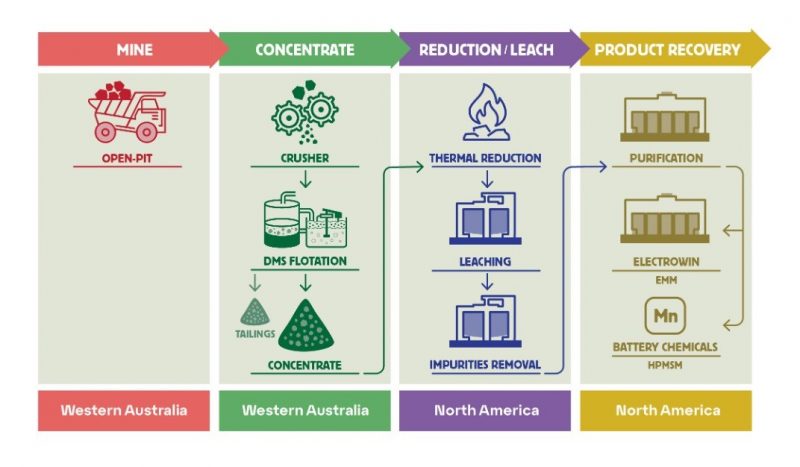

This is where AE Fuels’ 100-per-cent-owned South Woodie Woodie project in Western Australia enters the discussion, with staged development to extract and process HPMSM and electrolytic manganese metal (EMM) – the latter accounting for steel industry demand – placing the company in a prospective position to meet North American and allied EV and energy storage demand.

The 525.5-square-kilometre project, located near infrastructure and port facilities in the prolific Pilbara mining district, derives its name from the nearby Woodie Woodie manganese mine, one of the world’s highest-grade exemplars, an association it backs up with:

- Two known deposits, including an NI 43-101 inferred historical resource of 11.3 million tons grading 15 per cent manganese (1,695,000 tons of contained Mn metal) with test work indicating that manganese is upgradeable to more than 31 per cent with simple beneficiation. At current prices according to Trading Economics, the historical resource represents almost US$200 million in potential commodities in the ground, more than 20 times AE Fuels’ current market capitalization.

- Regional geology is prospective for high-grade manganese targets, supported by historical drilling spanning 418 drillholes and 39,920 m yielding up to 42.8 per cent manganese.

- An internal mine planning review considered future mining scenarios and associated engineering work, clarifying the project’s path through feasibility and construction.

AE Fuels began work on South Woodie Woodie’s end-to-end processing pathway in 2024, keen to align the project with HPMSM and EMM demand, laying out its plan in a conceptual flowsheet to guide technical studies.

Initial success came in the form of a reduction and leaching test work program, which achieved a manganese recovery rate of more than 90 per cent, producing the first manganese sulfate from South Woodie Woodie mineralization (see slide 9 of the March 2026 investor deck).

The company took an additional step towards production in 2025, partnering with CSIRO, Australia’s national science agency, to bring to market a manganese purification program suitable for HPMSM.

Phase 1 of the partnership involved bench-scale solvent extraction test work that produced a manganese sulphate solution exceeding lithium-ion battery specifications for HPMSM, with optionality for EMM, validating the conceptual flowsheet.

Phase 2 proceeded to mini-pilot test work simulating continuous processing using synthetic liquor matching South Woodie Woodie’s chemistry, with purity results also exceeding lithium-ion battery specifications.

An agreement for phase 3 test work, signed in February 2026 and co-funded through CSIRO’s Kick-Start program, was aimed at further scaling, optimizing and de-risking the project on the path to fully integrated production. AEF technical personnel participated directly in the program. Work is now complete and the results seen to date confirm, and in some respects better, the Phase 2 outcomes. Full details will be released once the formal final report has been received. Looking ahead, development work will include bulk sampling to facilitate ore sorting trials, a larger-scale continuous pilot program and drilling to underpin a resource update, all of which is setting AE Fuels up to finalize a pre-feasibility study in 2027 to transform South Woodie Woodie’s flowsheet from concept to reality.

The Fluorite Ridge fluorspar project

Like manganese, fluorspar plays critical roles across the battery value chain, from cathode to electrolyte to anode, with 5-10 times more fluorspar used in the manufacturing of a lithium-ion battery than lithium itself, according to data from The Oregon Group.

This is in addition to several applications across essential industries, listed below, which begs the question of why the critical mineral ranks among the United States’ most import-reliant commodities, with predominantly underground domestic production ceasing more than 50 years ago:

- Lowering the temperature of raw materials during steel and iron production, reducing costs, improving efficiency and enhancing product quality.

- Reducing energy consumption and increasing yield purity during aluminum production, helping to meet demand for the lightweight metal in the aerospace and defense industries.

- Serving as a protective coating for solar panels and wind turbines.

- Facilitating the conversion of solid uranium into gas, an essential step in the production of nuclear fuel.

Fluorspar’s diversified use-cases are also constrained by heavily concentrated supply, with China accounting for more than 60 per cent of global production and the critical mineral falling under the country’s aforementioned licensing requirements, raising the potential for near-term industrial bottlenecks to push prices beyond their December 2025 average of more than US$518 per ton.

While alternate sources of fluorspar are being developed in Mexico and Mongolia, these resources are limited, with demand forecasted to exceed production capacity by 40-70 per cent by 2035, presenting mining companies in Western-allied jurisdictions with an attractive opportunity to bring high-quality projects to market.

AE Fuels believes it has a worthy candidate with the 1,629-acre Fluorite Ridge project in Luna County, New Mexico, a singular asset that includes more than eight past-producing mines, yielding more than 106,000 tons in historic production (US$54 million at the aforementioned price), as well as numerous prospects over a 7 km strike length hosting what the company believes to be the first fluorspar zones in the US with open-pit mining potential (see slide 13 of the investor deck). Standout leads include:

- Historic fluorite production at the Greenleaf mine grading 50-92 per cent CaF2.

- The recent discovery of two zones averaging 23.5 per cent fluorspar across widths of 15 m and 22 m, respectively, with outcrops indicating substantial strike length and tonnage potential.

With a study by the New Mexico Bureau of Mines demonstrating that Fluorite Ridge’s low-grade ore (6 per cent fluorspar) can be refined into a commercial-grade product (55 per cent fluorspar) through a simple flotation process, AE Fuels is keen to further explore the project’s numerous vectors for expansion, aiming to advance it towards pre-feasibility to capitalize on a resource of potential global relevance.

A well-rounded leadership team with skin in the game

AE Fuels’ battery minerals value proposition is in the hands of an accomplished leadership team, whose global supply chain experience, calibrated by more than 50 per cent insider ownership, highly aligns the company’s path forward with investors’ best interests. Let’s meet key members now:

- Melissa Sanderson, Chair, is a former diplomat in the US Foreign Service who oversaw conflict resolution and strategic negotiations in Africa, Europe and Latin America. She also led global government relations and sustainable development initiatives for major miner Freeport-McMoRan (NYSE:FCX). She is currently Co-Chair of the Critical Minerals Institute and a Director of American Rare Earths (ASX:ARR).

- Gary Lewis, Founder, Executive Director and Chief Executive Officer (CEO), brings more than 30 years in capital markets, business and strategy development, having founded, invested in and operated more than US$400 million in resource projects spanning Australia, the UK, Asia and the Americas. He was the founder of both Robust Resources Limited (ASX:ROL) and Electric Metals (TSXV:EML).

- Mitchell Smith, Independent Director, complements AE Fuels’ leadership team with 15 years of executive leadership, entrepreneurship and capital markets experience focused on battery and energy metals. Mitchell has sourced and negotiated mining project acquisitions in North America, Europe and Australia, and has established offtake agreements with top lithium-ion battery cathode material companies. He is also Founder, CEO and Director of Global Energy Metals (TSXV:GEMC) and Director of the Battery Metal Association of Canada.

- Derek Marshall, Independent Director, has been a geologist for almost 20 years, specializing in both mining and exploration. Marshall currently serves as CEO of Trek Metals (ASX:TKM), which sold the South Woodie Woodie project to AE Fuels, and was previously at Solution Mining and Matrix Mining, the latter a US-focused manganese explorer. He also held senior technical roles at Newcrest Mining (now Newmont Corporation (NYSE:NEM)).

- Brandon Bonifacio, Non-Executive Director, is a proven mining executive with expertise in project assessment, M&A and project development. Bonifacio was the Finance Director of the Norte Abierto Joint Venture (Cerro Casale/Caspiche) in Chile’s Maricunga Region and was part of the corporate development team at Goldcorp (now Newmont Corporation). He is currently President, Director and CEO of NevGold and a director at both Aero Energy and Terra Balcanica Resources.

- John Levings, Technical Director, is a geologist with more than four decades of experience in the mining industry across exploration, project development and corporate roles. He has worked extensively in critical minerals, manganese, base metals and gold in Australia, Europe, Asia and North America. He has held senior technical and board positions with listed and private resource companies and has broad experience in geological evaluation, technical reporting, due diligence and advancing projects from exploration to development. He brings to AEF strong technical and strategic expertise, including direct involvement in manganese project assessment and development.

These formidable executives are complemented by a technical team with experience across the mining lifecycle, including multiple discoveries to their names, as well as robust backgrounds in critical minerals exploration, engineering and development, including manganese, de-risking AE Fuels’ ability to remain on an efficient production pathway.

The company rounds off its supporting cast with a recently formed Commercial Advisory Board, which will provide it with independent guidance to garner market share in the ex-China battery materials supply chain.

The Advisory Board will operate under the leadership of Joe Kaderavek, whose more than 30 years of advising, developing and investing in energy transition metals, battery technologies and disruptive technologies more broadly has afforded him key industry and government connections in Australasia and North America.

Kaderavek will be joined by Tyson Hall, one among numerous appointees expected to be made over the coming months, whose extensive US executive, commercial and technical experience in specialty chemicals and advanced materials will be invaluable to Fluorite Ridge’s go-to-market strategy. Hall has led businesses generating from US$100 million to US$3 billion in revenue per year, highlighted by Albemarle‘s bromine and lithium franchises, the latter standing as the largest in the world.

This emerging battery minerals producer has ample room to run

While it’s reasonable for investors to ask if shares of AE Fuels, down by 20 per cent since inception, are accurately reflecting the underlying company’s future growth potential, the data shows that the only reasonable answer is a resounding ‘no’.

Readers will quickly see why when we compare AE Fuels’ market cap of C$8.72 million with the value of South Woodie Woodie’s historical resource of almost US$200 million, entailing a more than 20x dislocation that would likely result in exponential returns, should the company deliver development milestones over the next few years and successfully demonstrate a value-added construction plan.

This dislocation only grows more robust when we consider Fluorite Ridge’s upside potential, where high-grade targets and production, spanning eight historical mines across more than 7 km of mineralization, position the company to apply modern exploration techniques and add tens of millions of dollars in potential commodities to its resource base.

With development and potential construction likely seeing the company through the end of the decade, momentum building from a broader investor base following an OTCQB listing in February, and a tight capital structure of 47.9 million shares fully diluted offering a flexible path to delineating production parameters, the thesis for building a position in AE Fuels today is undoubtedly one of high conviction.

Join the discussion: Find out what investors are saying about this critical minerals mining stock on the AE Fuels Corporation Bullboard and make sure to explore the rest of Stockhouse’s stock forums and message boards.

Stockhouse does not provide investment advice or recommendations. All investment decisions should be made based on your own research and consultation with a registered investment professional. The issuer is solely responsible for the accuracy of the information contained herein.

For full disclaimer information, please click here.