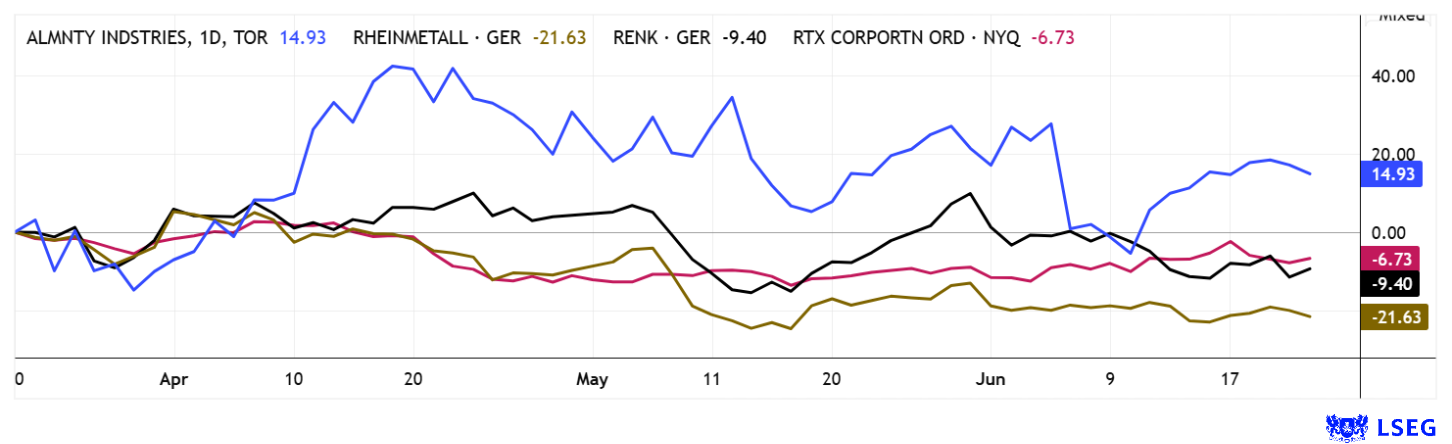

Almonty Industries: The revaluation is really gaining momentum now

Hard to believe but true: The price of tungsten (APT Rotterdam) has increased tenfold over the past 12 months, from around USD 300 to over 3,000 per MTU (Metric Ton Unit). Almonty Industries is at the center of a global tungsten market that has evolved from a cyclical commodities segment into a geopolitically driven scarcity-based system. The enormous price momentum since the fall reflects not only crisis-induced momentum but also a structural repricing of one of the planet’s most critical metals. Due to its extreme physical properties, tungsten is virtually irreplaceable in defense, aerospace, semiconductors, and high-temperature applications, and has thus become highly relevant to national security. Even with the addition of production from the reopened Sangdong Mine in South Korea, China continues to control the majority of global production and nearly all downstream processing. Time is running out for the West!

Against this backdrop, supply chain issues have shifted from an industrial topic to a core security policy issue. On the demand side, several supercycles are occurring simultaneously, as the defense sector as well as the semiconductor and high-tech industries are significantly expanding their volumes. Low price elasticity is particularly crucial because alternative materials cannot meet the technical requirements of many applications. This creates markets in which rising prices do not lead to falling demand but instead further exacerbate scarcity. In this environment, the mere availability of materials is clearly gaining importance over cost optimization. CEO Lewis Black has provided investors with this assessment of the situation at numerous conferences; nevertheless, it took 12 years before Almonty’s stock finally made its breakthrough in 2025. The company fills the gap among the few relevant non-Chinese producers with scalable prospects. And the transition from a development story to industrial production has now been completed amid significant attention.

Given comparatively low production costs, the current market environment creates significant margin leverage in the face of rising prices. In addition, long-term offtake agreements secure stable minimum prices while simultaneously allowing the company to benefit from market peaks. Analysts have had to repeatedly adjust their cash flow projections, which has consistently pushed the company’s net present value (NPV) higher. The adjacent molybdenum project will become an additional strategic component in the coming years, as molybdenum is used as an alloying metal in similar high-temperature applications. Almonty intends to begin production without delay once the deposit is confirmed and views the project as a contribution to South Korea’s security of supply. So the next gear is already engaged!

The current drilling program indicates that historical resource models can be both validated and expanded. Of the planned 26 drill holes totaling approximately 12,000 m, about 37% have already been completed. The capital market has begun to increasingly price in Almonty’s transformation but is also prepared to allow for minor corrections during interim highs. Research firms such as GBC and Sphene Capital have significantly revised their models upward and are increasingly working with structurally higher price assumptions for tungsten. Following its recent USD 800 million convertible senior notes offering, a re-rating scenario is emerging for Almonty, where operational execution and geopolitical relevance are directly translating into higher valuation multiples. Because the notes feature a high initial conversion price, they avoid immediate equity dilution, protecting shareholders while reinforcing both the stock and the balance sheet. With price targets of CAD 28.60 and CAD 37.40, respectively, there is again an opportunity to act following the recent correction to CAD 26. Risk-conscious investors should take advantage of this situation to buy more shares!

CEO Lewis Black spoke at the 19th International Investment Forum (www.ii-forum.com) in May about Almonty’s opportunities during challenging times.

Rheinmetall and RENK: Defense Sector Blockbusters in Correction Mode

The gradual correction in the German defense sector coincides with some critical voices regarding the pace at which the market is adjusting to operating figures. With medium-term revenue forecasts of EUR 33 billion by 2029, the German defense conglomerate Rheinmetall had been assigned an average price target of EUR 2,195 in November 2025. Unfortunately, the Düsseldorf-based company’s share price had already surpassed EUR 2,000 in October. New investors were subsequently forced to watch as skeptical market commentary regarding the approach to the consensus price target became increasingly frequent. Finally, during the last phase of euphoria, the share price reached EUR 1,950 once again; in the period that followed, it corrected by 40% to EUR 1,170. In reality, this has not changed much, as long-term investors are still looking at a twelvefold increase; as always, it is the hesitant and indecisive investors—who spent months watching the price from behind—who are left behind. The upside: the 2029 P/E ratio has fallen to 18, and the corresponding price-to-sales (P/S) ratio is now below 2. Anyone betting on rising volatility in the coming weeks should place limit orders in the EUR 750-1,000 range.

The story at RENK is similar, except that the Augsburg-based company did not become a full-fledged defense contractor until 2026. A change in management and a new strategic focus have brought the share of revenue from defense systems to over 75% of total revenue. Prices around EUR 45 indicate a halving from current levels; on the P/S front, the rat2029 ratioso falls below 2. However, since the company is growing at only half the rate of Rheinmetall, the more dynamic option from Düsseldorf is preferable in sell-offs. On the LSEG platform, RENK is shown to have an average 12-month price target of just under EUR 68—representing 50% upside potential in the medium term. The chart is not very informative given the company’s initial listing in 2024, but it does show good support levels in the EUR 35-40 range. No fewer than 15 out of 18 analysts are giving it a thumbs-up!

RTX Corporation: Patriot and Tomahawk in Higher Demand Than Ever

Now, a quick look across the Atlantic. RTX (formerly Raytheon) is of extreme importance to the US government, Israel, and ultimately Ukraine. The Arlington, Virginia-based company is an aerospace and defense conglomerate that also includes the turbine manufacturer Pratt & Whitney. Its business model is based on long-term government, military, and industrial contracts. The company is best known for the development and production of defense systems, aircraft engines, and aerospace technology. Key products include the Patriot missile defense system, the AMRAAM air-to-air missile, the SM-3/SM-6 interceptor missiles, and the Tomahawk cruise missile. In addition, Raytheon—as a division of RTX—develops guided missiles, sensors, and defense systems for air, land, and sea targets. A significant part of the business involves maintaining and technologically upgrading existing platforms over decades. This makes RTX less of a traditional weapons manufacturer and more of a diversified defense and technology systems provider. In the current budget discussions, however, there is consensus that congressional talks will yield a positive outcome, as Patriot systems, in particular, are in high demand across a wide range of fronts. A 2027 P/E ratio of 24 and a P/S ratio of 2 are likely good entry points, provided the geopolitical situation does not change significantly in the foreseeable future. RTX is exceptionally well-positioned and has become as important as Johnson & Johnson’s cosmetics division. For long-term investors, USD 185 is a good entry point; the all-time high in 2026 stands at USD 214. 17 out of 23 analysts on LSEG rate it a “Buy.” A safe bet in the long run!

After long bull runs, the market is taking a brief pause in the defence and strategic metals sectors. After gains of over 2,000% for Almonty and Rheinmetall, this is only to be expected, since all companies under review have seen a fundamental decline in valuations; a further repricing can be expected as the year progresses! Buy on dips—this applies in particular to Almonty and Rheinmetall, the long-term blockbusters of their respective sectors.

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as “Relevant Persons”) currently hold or hold shares or other financial instruments of the aforementioned companies and speculate on their price developments. In this respect, they intend to sell or acquire shares or other financial instruments of the companies (hereinafter each referred to as a “Transaction”). Transactions may thereby influence the respective price of the shares or other financial instruments of the Company.

In this respect, there is a concrete conflict of interest in the reporting on the companies.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is also a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.

Stockhouse does not provide investment advice or recommendations. All investment decisions should be made based on your own research and consultation with a registered investment professional. The issuer is solely responsible for the accuracy of the information contained herein. For full disclaimer information, please click here.