Shell and BP – A warm rain for the multinationals

The global energy market is currently under exceptional strain as strategic reserves dwindle and key export routes remain blocked. The market is particularly sensitive to developments around the Strait of Hormuz, through which around 20% of global oil trade passes. Even limited restrictions on this route can create significant supply risks and trigger short-term price spikes. In this environment, the price of oil climbed again yesterday towards USD 100 per barrel. Several investment banks believe it is possible that crude oil could establish itself permanently above the USD 100 to 120 mark if the escalation continues, which is also likely to push up medium-term price forecasts for 2026. What madness for the global economy! Experts already predict growth losses of 0.15 to 0.30% due to the Iran conflict alone. The biggest loser is likely to be Europe, which is suffering from high inflation.

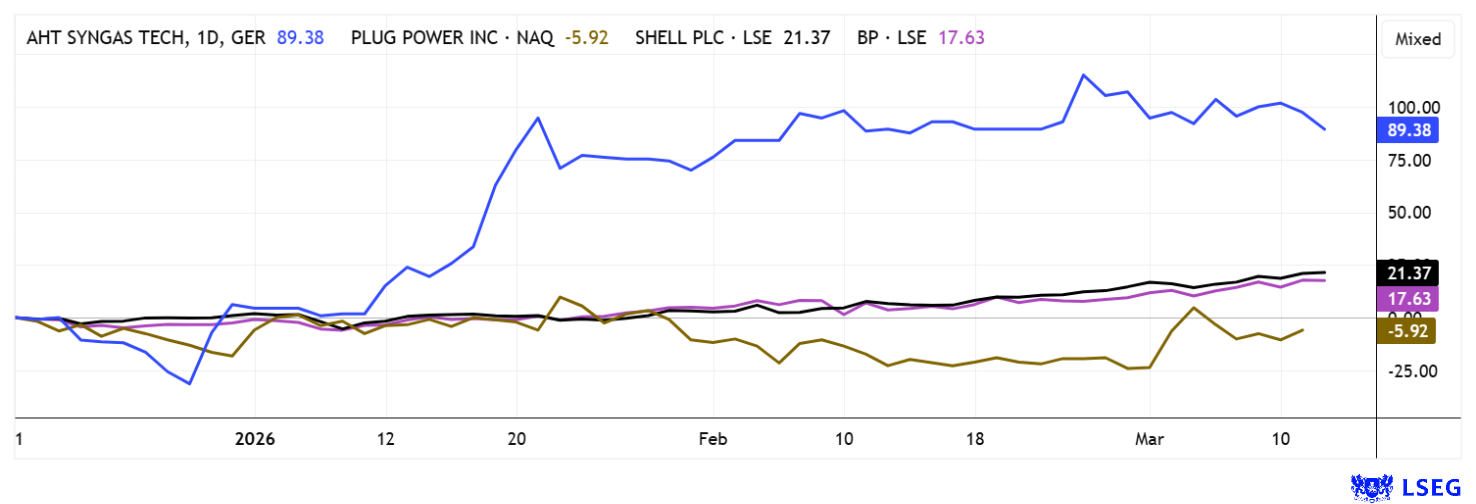

Global energy companies with a broad production base and high cash flow generation are the main beneficiaries of such market phases. One example is the Shell Group, which is strongly positioned in both the traditional production business and international LNG trading. Rising energy prices, therefore, have a direct impact on revenue and operating results. Analyst estimates predict an increase in profits of up to 25% for 2026 to 2028. In Shell’s case, this would mean EBIT of approximately USD 30 to 35 billion for 2026, which would bring the 2026 P/E ratio down further from the most recently calculated 13.2 and could enable a dividend increase to USD 1.70 from USD 1.50. The announced share buyback programs are also likely to be further increased. The share price reached a new all-time high of around EUR 38.30 yesterday.

British Petroleum plc (BP) is also in the spotlight for investors. The group has significantly streamlined its cost structure in recent years. It continues to focus on improved cash flows from its oil and gas business, while at the same time investing in new energy technologies. Due to relatively low production costs, BP can benefit disproportionately from rising crude oil prices in a high-price environment. From a historical perspective, the current price of around EUR 6.10 remains well below the high of EUR 11 in the early 2000s, which some analysts interpret as leaving room for further upside. The 2025 figures on April 23 may well contain plenty of good news for higher prices. Shell and BP are tempting investors to increase their holdings!

A.H.T. Syngas Technology – Biomass technology for industry and the hydrogen economy

With Europe’s gas problems, a new technology provider is entering the scene. A.H.T. Syngas Technology N.V. is a provider of decentralized energy solutions that converts biogenic residues into climate-friendly forms of energy, thereby making a solid contribution to industrial decarbonization. In the right place at the right time! At the heart of the company’s technology is a patented gasification process that can be used to thermochemically convert various biomass residues, such as wood waste, sewage sludge, or fermentation residues, into synthesis gas. The resulting gas mixture of hydrogen and carbon monoxide can be used both as a process gas in industrial applications and for power and heat generation. The rapidly growing market for synthesis gas is considered a bio-based alternative to fossil fuel energy supplies and is rapidly gaining in importance. A.H.T. technology is aimed in particular at industrial applications where energy needs to be generated as close as possible to the point of consumption. Standardized plant concepts allow projects to be implemented more quickly and investment costs to be calculated more accurately, which increases the scalability of the technology.

At the same time, the company has expanded its strategic focus and is evolving from a traditional plant manufacturer to an operator of its own energy plants. This contracting model extends the value chain and enables long-term recurring revenue streams. An additional technological development step was achieved with the completion of the publicly funded BiDroGen project, which deals with the decentralized production of climate-neutral hydrogen from biogenic residues. A process chain was developed and demonstrated on a container scale that converts wood residues into high-purity hydrogen for fuel cell applications. A specially adapted water-gas shift stage plays a central role, increasing the hydrogen content in the synthesized gas and thus improving the efficiency of the entire plant.

CEO Gero Ferges explained his corporate strategy at the 18th International Investment Forum.

The A.H.T. approach addresses a market with significant demand prospects: forecasts predict that annual hydrogen demand in Germany could rise to several hundred terawatt hours by 2050. In addition to the chemical industry, the transport sector and energy-intensive manufacturing industries are considered to be key drivers of demand. Production costs for the process described are expected to be in the range of around EUR 4 to 8 per kilogram of hydrogen, which could result in potential cost advantages compared to many electrolysis-based processes. Additional revenue opportunities are expected to arise from CO₂ reduction instruments and markets for emission certificates.

Operationally, the company is currently focusing primarily on European projects, while at the same time continuously developing its technology platform to enable it to process a wider range of biogenic waste streams. At a share price of around EUR 4.20, A.H.T. Syngas is worth around EUR 7 million. Research firm GBC started its coverage with a 12-month price target of EUR 8.50. A clear 100% gain with double tailwinds from the Middle East and Brussels!

Plug Power – Andy Marsh bids farewell, José Lui Crespo takes the helm

Is this a turning point for Plug Power? After a euphoric surge in 2021, the company underwent a massive revaluation in 2025, with a 95% drop in its share price from its peak. This was triggered by capital requirements, operational setbacks, and an increasingly harsh funding environment in the US. Now there is renewed hope, as the figures for Q4 2025 were better than expected. There was a 12.9% increase in revenue, bringing annual revenue to USD 710 million, and in the last quarter, analyst estimates were even slightly exceeded with USD 225 million. Although the gross margin, which was still negative in the previous year, is positive for the first time at 2.4%, there is still a loss of USD 1.69 billion for the year as a whole, compared to a loss of USD 2.1 billion in 2024. CEO Andy Marsh, who became more famous for his inaccurate forecasts than for positive performance, handed over the baton to his successor, José Luis Crespo, on March 2. The former Chief Revenue Officer is to focus in particular on international business, especially in Europe, and lead the hydrogen specialist to an operational turnaround. However, analysts on the LSEG platform continue to expect significant losses for 2026 to 2028. After a brief rally of hope to the resistance level of around USD 2.50, the share price fell back below USD 2.20. Let’s see what the new CEO has up his sleeve. Wait and see!**

Few would have expected the Iran conflict to throw the world so far off balance. However, this is also due to the bold rhetoric of the president, who spoke of a blitzkrieg shortly after the hostilities began. As we now know, that was nonsense. In the medium term, oil prices could therefore rise significantly further. For investors, this initially shifts attention to the oil majors, but increasingly also to companies such as A.H.T. Syngas or Plug Power, which can offer viable technological alternatives to fossil fuels during such energy crises.

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as “Relevant Persons”) currently hold or hold shares or other financial instruments of the aforementioned companies and speculate on their price developments. In this respect, they intend to sell or acquire shares or other financial instruments of the companies (hereinafter each referred to as a “Transaction”). Transactions may thereby influence the respective price of the shares or other financial instruments of the Company.

In this respect, there is a concrete conflict of interest in the reporting on the companies.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is also a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.

Stockhouse does not provide investment advice or recommendations. All investment decisions should be made based on your own research and consultation with a registered investment professional. The issuer is solely responsible for the accuracy of the information contained herein. For full disclaimer information, please click here.