Nevada Gold Mines: Efficiency and Internal Conflicts

Nevada Gold Mines, the joint venture between Barrick Mining and Newmont, is a key player in the region. Its business model is based on consolidating world-class assets in the Carlin and Cortez trends to leverage economies of scale in processing and logistics. For the full year 2025, Barrick Mining reported strong gold production of 3.26 million ounces. However, these stable operating figures are currently overshadowed by a challenging legal dispute in which Newmont accuses its partner Barrick Mining of so-called resource piracy and claims that key personnel and equipment have been systematically withdrawn from the joint venture. This dispute over the high-grade Fourmile project is symptomatic of the scarcity of high-quality reserves across the entire industry and is forcing players to look for new, conflict-free deposits.

Kinross Gold: Aggressive Search for Reserves

Meanwhile, Kinross Gold is pursuing a strategy to secure its long-term production in Nevada and is focusing on leveraging existing infrastructure to develop new, higher-grade zones. Just last January, the company announced it would continue with the phased development of projects such as Round Mountain Phase X to counteract cost inflation driven by higher ore grades. Since the group is benefiting significantly from the current market environment and was able to increase its margins by 66% in 2025, management has ample free cash flow available for targeted acquisitions. Analysts cited by Bloomberg and Reuters largely rate the stock with clear “Buy” recommendations, but point out that the hunger for new high-quality reserves in the Walker Lane trend must be satisfied in the near term through external acquisitions. This is where Lahontan Gold could come into play.

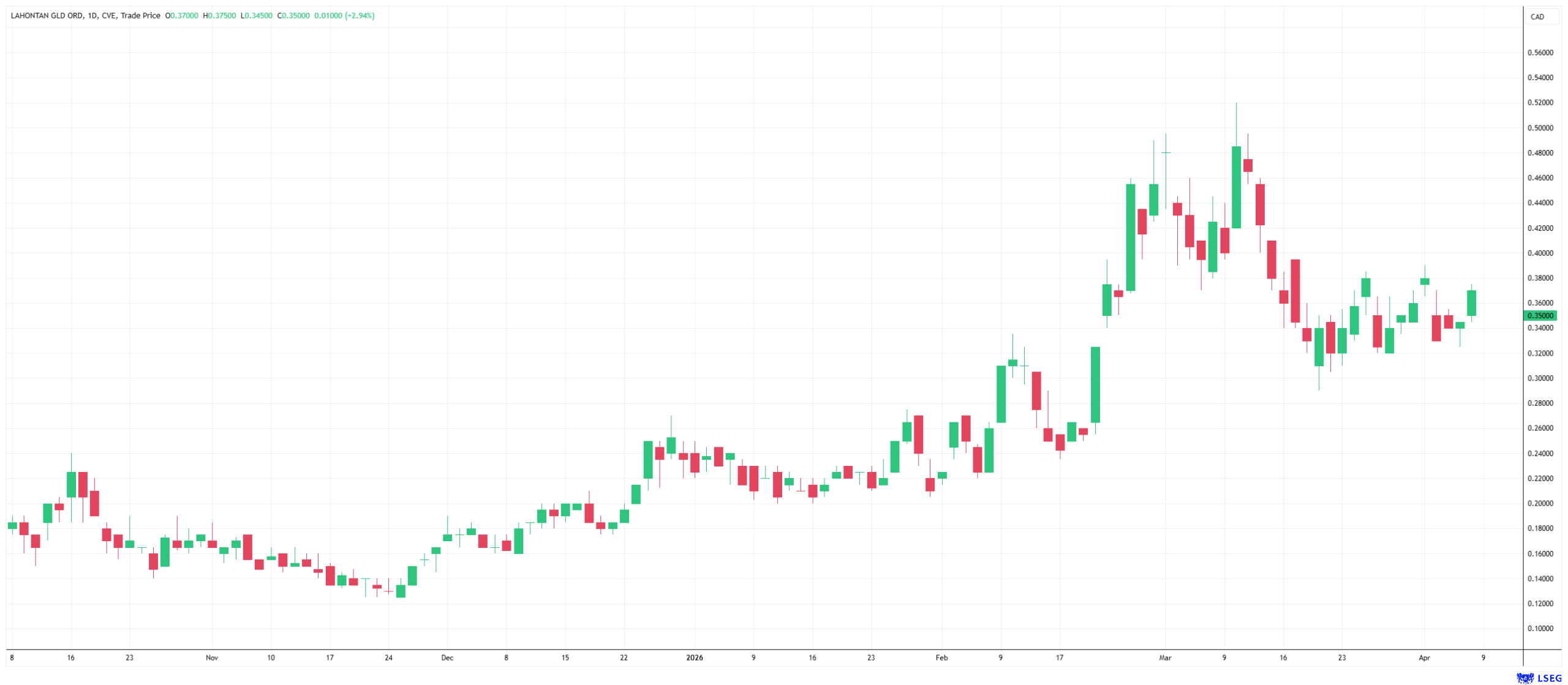

Lahontan Gold: A Jewel in the Walker Lane Trend

Amid consolidation pressure from major commodity conglomerates, Lahontan Gold is proving to be a particularly promising target. Its business model focuses on revitalizing former producing mines, with the flagship Santa Fe project at its core. Most recently, the company reported clear successes through an expanded drilling program. The company’s geologists confirmed the existence of a high-grade oxide core through outstanding drill results, which included 3.11 g/t AuEq (gold equivalent) over 36.6 m directly from surface. Since Santa Fe is a former mine, the project already has existing permits and production areas, which accelerates environmental impact assessments and paves the way for a rapid production decision. The recently completed financing of CAD 13.6 million also ensures that management can fully implement its exploration targets by 2027.

A Logical Takeover Candidate Given These Conditions

Lahontan Gold could prove to be particularly promising among all Nevada plays. A technical report already valued the project at USD 471.6 million based on a gold price of USD 4,000, a figure that could be significantly exceeded again based on price forecasts. Led by CEO Kimberly Ann, the company is large enough to be relevant to giants like Kinross with its existing resources, yet small enough for investors to benefit massively from new discoveries—as experience shows, good drilling results rarely make a difference for large corporations. At a time when major producers are seeking approved and scalable projects in the US, Lahontan Gold is emerging as one of the most obvious acquisition candidates.

Another competitive advantage for Lahontan Gold is the combination of modern, environmentally friendly exploration and regulatory tailwinds. The company uses advanced technologies such as AI-powered geological modeling and satellite monitoring to reduce the environmental footprint of exploration to an absolute minimum. At the same time, the Santa Fe project benefits from US government initiatives such as FAST-41, which aim to streamline permitting processes for strategically important infrastructure and mining projects. Given these conditions, coupled with further promising drill results such as 0.45 g/t AuEq over 69 m in the extension of the York and Slab zones, analysts from platforms like Stockopedia and Investing.com rate the stock as a clear “Buy”. With a consensus price target of around CAD 0.75, experts see significant upside potential of more than 100% relative to the current valuation level. Lahontan Gold is therefore a stock that investors should take a closer look at.

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as “Relevant Persons”) may hold shares or other financial instruments of the aforementioned companies in the future or may bet on rising or falling prices and thus a conflict of interest may arise in the future. The Relevant Persons reserve the right to buy or sell shares or other financial instruments of the Company at any time (hereinafter each a “Transaction”). Transactions may, under certain circumstances, influence the respective price of the shares or other financial instruments of the Company.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.

Stockhouse does not provide investment advice or recommendations. All investment decisions should be made based on your own research and consultation with a registered investment professional. The issuer is solely responsible for the accuracy of the information contained herein. For full disclaimer information, please click here.