Timing Beats Technology: The Subtle Difference Between ITM Power and Nel ASA

Those who shift their focus from the Gulf region to the broader world will find alternative opportunities in hydrogen, which is now experiencing a renaissance. However, volatility here is also substantial. At first glance, price movements in the hydrogen sector may appear irrational, but a closer look reveals a classic pattern: investors reward visible progress and penalize operational uncertainty. A clear example of this can be seen in ITM Power and Nel ASA.

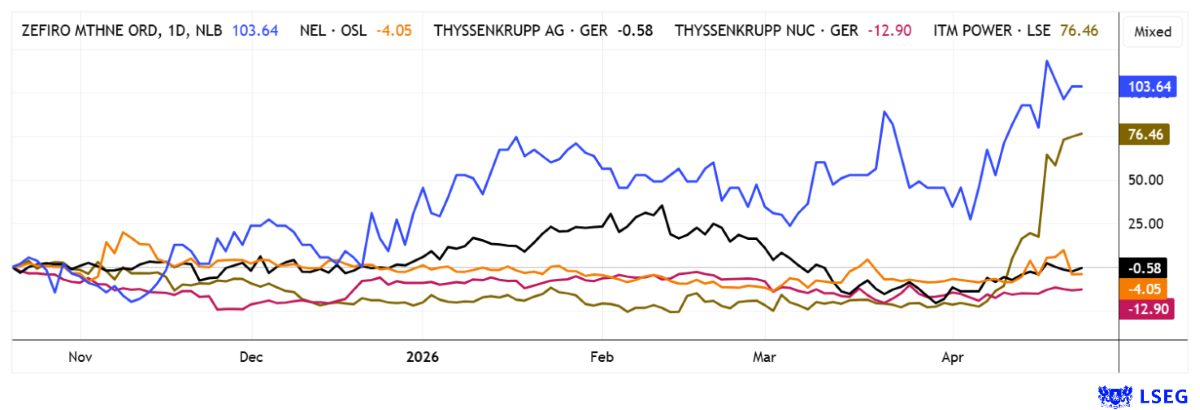

While both companies operate in the same industry, their strategic phases currently differ significantly. ITM Power is in a phase of operational stabilization, while Nel ASA is still grappling more intensely with structural adjustments and fluctuations in demand. A key driver of ITM Power’s relative strength is the perception of an emerging turnaround. In recent quarters, the company has cut costs, focused on projects, and realigned its production strategy—steps investors interpret as a sign of strong discipline. The stock market sent the stock soaring by over 130% in just three weeks; perhaps that is a bit too much. In any case, be sure to set a stop-loss order for yourself.

Nel ASA, on the other hand, is suffering more from a classic scaling problem in the hydrogen industry. While the Norwegian company has strong technological expertise and a long history, major customers have repeatedly postponed their purchasing decisions, leading to significant revenue fluctuations and uncertainty. In an environment of rising financing costs and delayed investment decisions, investors are particularly sensitive to such delays. After a more than 90% plunge since 2022, the stock price has managed to climb just 10% from its low. Technical analysts, in particular, are waiting for a breakout above the EUR 0.24 mark.

Policy Stability, Growing Backlog: The Quiet Strength Behind the Zefiro Story

From hydrogen to methane. Zefiro Methane is an agile US environmental services provider focused on a structurally growing challenge: the permanent decommissioning of legacy oil and gas wells and the measurement of methane emissions. The business model centers on supporting government programs and energy companies in the remediation of so-called “orphan wells,” which have been left without operators and pose significant environmental risks. At its core, the company generates revenue by physically plugging these wells, complemented by emissions measurement services and the generation of carbon credits from successfully completed projects. As such, Zefiro operates in a regulation-driven niche with long-term demand linked more to public funding and environmental policy than to commodity price cycles. Operationally, the company is currently in a phase of accelerated scaling, during which new projects are being executed more quickly, and the pipeline is visibly growing.

The company is currently advancing several new large-scale projects, including a government contract worth nearly USD 20 million, which should support revenue visibility in the coming quarters. At the same time, debt has been reduced, and project-level profitability has improved, strengthening operational resilience. The subsidiary Plants & Goodwin has also begun generating initial revenues from proprietary technology, following deployments of its REED tool by industrial customers in Pennsylvania. These projects mark the launch of a new revenue stream and complement a core business that has already generated more than USD 22 million in revenue and USD 3.8 million in adjusted EBITDA over the past two quarters. The technology, developed by Radial Casing Solutions, enables cost-efficient sealing of well casings, potentially avoiding repair costs ranging from hundreds of thousands to millions of dollars. Since Plants & Goodwin holds the exclusive licensing rights to these patents in the US, this creates a scalable ancillary business through further deployments or licensing agreements.

From an analytical perspective, this initial technology revenue strengthens the investment case, as it demonstrates that the business model is evolving from a pure service provider into a supplier of higher-margin solutions. With 75.68 million shares outstanding, Zefiro Methane is currently valued at just CAD 43 million. The stock can be traded in Canada under the ticker symbol “ZEFI” or in Frankfurt. The current entry point could not be better!

thyssenkrupp – Profit Warning at Hydrogen Subsidiary nucera

Hydrogen could fuel the energy transition—if only it were not so expensive! Electrolysis specialist thyssenkrupp nucera had to issue its first profit warning just three years after its initial listing at EUR 20. Internationally, it remains consistently difficult to make significant strides with hydrogen. The stock has lost over 60% since 2023 compared to its initial listing. However, there is light at the end of the tunnel. The Dortmund-based company is now feeling more positive again regarding order intake for the current 2025/26 fiscal year. The main reason for the new forecast is an order from the Spanish energy company Moeve. nucera is set to supply electrolysers with a capacity of 300 MW for a hydrogen plant in Andalusia. These are expected to reach an annual production capacity of around 45,000 tons of green hydrogen in the future.

According to reports from Dortmund, order intake will grow from EUR 348 million to between EUR 550 and 850 million in the current fiscal year, partly due to this major order. Until now, the management team led by CEO Werner Ponikwar had projected a range of EUR 350 to 900 million. Analysts would call this a wide range, but visibility is simply limited given ongoing geopolitical upheavals. “We are playing it by ear,” is the message from senior management. nucera had already scaled back its annual targets in April due to a canceled project and costly rework. The company is now targeting revenue of only EUR 450 to 550 million for the fiscal year, instead of the previously targeted EUR 500 to 600 million. Wait and see!

The capital markets currently present a different scenario every day. In the short term, hope flares up that the conflict in the Middle East might soon be over, only to be immediately followed by the next escalation. In some areas, the current doubts about fossil fuels are actually spurring growth in the alternative energy sector. Hydrogen and the methane sector, in particular, are benefiting from this environment. While ITM Power and Zefiro Methane are making headway here, caution is still advised with thyssenkrupp nucera and Nel ASA.

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as “Relevant Persons”) currently hold or hold shares or other financial instruments of the aforementioned companies and speculate on their price developments. In this respect, they intend to sell or acquire shares or other financial instruments of the companies (hereinafter each referred to as a “Transaction”). Transactions may thereby influence the respective price of the shares or other financial instruments of the Company.

In this respect, there is a concrete conflict of interest in the reporting on the companies.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is also a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.

Stockhouse does not provide investment advice or recommendations. All investment decisions should be made based on your own research and consultation with a registered investment professional. The issuer is solely responsible for the accuracy of the information contained herein. For full disclaimer information, please click here.