Intel: Operational Pressure Forces Smart Capital Model

As an integrated chip manufacturer, Intel serves the PC and server market with its own processors and also acts as a contract manufacturer for external chip designers. To relieve pressure on the balance sheet amid high operating losses in the foundry business, the group, under the leadership of Lip-Bu Tan, is adopting a smart capital model. Due to changed market expectations, management has cancelled the projects in Germany and Poland despite high subsidies and is consolidating European manufacturing in Ireland. Financially, the US government’s investment supported the company by converting subsidy commitments into a direct government equity stake of approximately 10%. Nevertheless, massive write-downs of assets under construction are weighing on profitability, resulting in a GAAP net loss of USD 3.73 billion in the first quarter of 2026.

Marvell Technology: AI Order Surge and Collapsing Margins

Marvell Technology offers solutions for data infrastructure and semiconductors. Revenue for the full year 2026 climbed to a record USD 8.195 billion, driven by robust order intake of electro-optical network interfaces. However, the detailed income statement for the first quarter of fiscal year 2027 shows just how vulnerable the chip designer is to headwinds. Net income fell significantly to just USD 34.5 million, while the net profit margin collapsed from 9.4% to 1.4%. A one-time M&A expense caused this slump. Shareholders are also increasingly critical of high research and development expenditures. Whether these expenditures will materialize after years of AI hype remains questionable for many observers. It is precisely this uncertainty that is driving capital into real tangible assets—above all, gold.

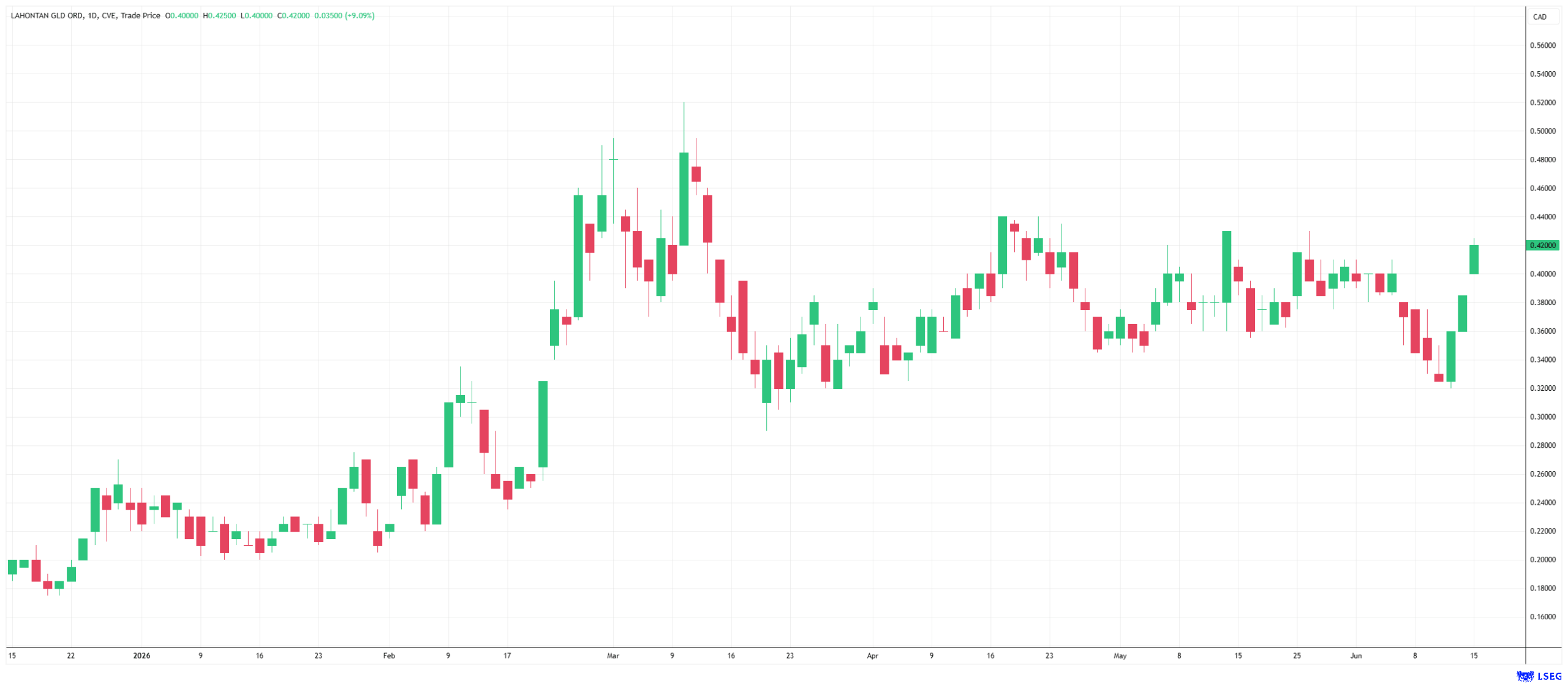

Lahontan Gold: Million-Ounce Deposit in a Crucial Phase

The Canadian mining company Lahontan Gold is developing, through its US subsidiaries, the historic Santa Fe gold mine in the Walker Lane Trend in the US state of Nevada. The resource estimate indicates indicated resources of 1,539,000 ounces of gold equivalent (AuEq) grading 0.99 g/t for the project. The inferred resources comprise an additional 411,000 ounces of AuEq with an average grade of 0.76 g/t.

The drilling campaign, which commenced in the first half of the year, supports the economic viability of the planned heap leaching process with high-grade results. Drill hole CAL26-02C returned a grade of 0.44 g/t AuEq over 90.8 m, including a core zone of 1.22 g/t AuEq over 12.3 m. At the West Santa Fe satellite project, drill hole WSF25-03R confirmed a near-surface, ultra-thick intercept of 41.2 m grading 1.94 g/t AuEq. These are promising results for the planned heap leaching process and make a rapid start to production more likely.

Lahontan Gets Serious: Cost Efficiency, Net Debt-Free Status, and Strategic Management Restructuring

The preliminary economic assessment (PEA) envisions a conventional open-pit operation with a processing capacity of 12,500 tonnes of ore per day. The engineering firm Kappes, Cassiday & Associates assessed the project’s economic viability and determined an after-tax project value (NPV5) of USD 200 million at an internal rate of return of 34.2%—calculated based on gold prices at that time. Given the significant rise in the gold price since then, this project value is likely to improve considerably in an updated PEA. In preparation for the planned mine construction, the company, which has approximately CAD 13 million in cash, carried out a targeted management realignment. The board recruited renowned mining specialists Shane Williams and Evan Pelletier, who bring extensive operational experience in the rapid commissioning of heap leach mines.

Conclusion: Strong Case for a Countercyclical Entry – From Tech to Gold Now?

The dwindling reserves of major gold producers have triggered a wave of consolidation in the sector, with buyers paying, on average, double-digit acquisition premiums relative to recent market valuations. Transactions such as Coeur Mining’s USD 1.7 billion acquisition of SilverCrest Metals or Minera Alamos’ purchase of the Pan Gold Mine in Nevada serve as blueprints. While tech stocks like Marvell are often highly risky with triple-digit P/E ratios, Lahontan Gold is valued at just around CAD 134 million. If the gold price gains momentum again, Lahontan Gold’s stock is likely to come into focus quickly—US assets are likely to be the first choice as investors shift from tech to gold to position themselves more defensively amid ongoing uncertainty. Investments in Nevada’s gold region are attractive given the existing infrastructure and excellent conditions.

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as “Relevant Persons”) may hold shares or other financial instruments of the aforementioned companies in the future or may bet on rising or falling prices and thus a conflict of interest may arise in the future. The Relevant Persons reserve the right to buy or sell shares or other financial instruments of the Company at any time (hereinafter each a “Transaction”). Transactions may, under certain circumstances, influence the respective price of the shares or other financial instruments of the Company.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.

Stockhouse does not provide investment advice or recommendations. All investment decisions should be made based on your own research and consultation with a registered investment professional. The issuer is solely responsible for the accuracy of the information contained herein. For full disclaimer information, please click here.