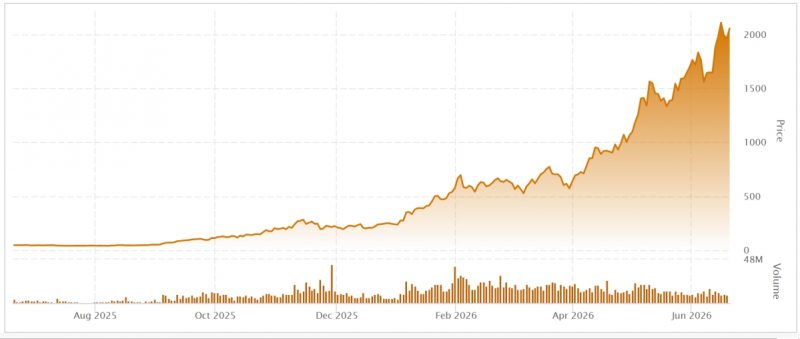

- SanDisk (NASDAQ:SNDK) stock has surged about 700 per cent in 2026 to over US$2,100 as an AI-driven NAND memory shortage flipped the company into massive profitability and made it the market’s most extreme momentum trade

- With unusually high volatility and a beta above 3, the shares are highly sensitive to the Fed decision today, where hawkish signals could trigger a pullback while dovish guidance could extend the rally

- The same memory shortage is showing up in products, with SanDisk launching a PS5-compatible 8TB SSD priced near US$3,000 and even lower-capacity drives costing as much as, or more than the console itself

- SanDisk stock (NASDAQ:SNDK) opened trading at US$2,044.75

SanDisk (NASDAQ:SNDK) has become the defining momentum trade of 2026, with shares changing hands near US$2,105 after a 6.34 per cent gain in the prior session and sitting just below the US$2,167 all-time high set on June 16. The move is historic in both speed and scale: the stock has surged roughly 700 per cent year to date, transforming from a US$40 spin-off into a roughly US$300 billion-plus market heavyweight in a little over a year.

The advance has taken on a parabolic character. With a beta of 3.45 and daily volatility running above 9 per cent, the name is now widely described by market participants as “the most overbought stock in history.” That combination of extreme momentum, leverage to macro conditions, and concentrated exposure to a single commodity cycle makes SanDisk uniquely sensitive to Thursday’s Federal Reserve decision.

This article is a journalistic opinion piece that has been written based on independent research. It is intended to inform investors and should not be taken as a recommendation or financial advice.

The Fed as a near-term catalyst

The Fed’s June decision represents the immediate wildcard. While the policy rate was kept unchanged in the 3.50 per cent–3.75 per cent range, the focus for investors is squarely on the updated dot plot and forward guidance.

For a high-duration, high-beta growth stock like SanDisk, the implications are magnified. With a beta of 3.45, SNDK historically amplifies broader market moves by more than threefold. A hawkish signal that reinforces a higher-for-longer rate path could compress valuations and trigger volatility in the most extended names. Conversely, even a modest dovish tilt could act as fuel for an already parabolic rally.

In practical terms, there may be no equity more levered—both fundamentally and mechanically—to the outcome of the Fed print.

The catalyst: An AI-driven NAND super-cycle

The fundamental driver of SanDisk’s vertical move is the ongoing NAND flash memory super-cycle, a supply-demand imbalance tied directly to the rapid buildout of artificial intelligence infrastructure.

The company, spun off from Western Digital in early 2025, now operates as a pure-play NAND flash supplier. That positioning has proved pivotal. Unlike diversified peers, SanDisk is almost entirely exposed to flash memory pricing, allowing investors to use it as a concentrated expression of the AI storage boom.

Demand has surged as hyperscale data centres expand to support AI workloads. NAND flash—used extensively in solid-state drives for storing and accessing massive datasets—has become a bottleneck resource, pushing prices sharply higher.

At the same time, supply has struggled to keep pace. Industry capacity remains constrained, with manufacturers prioritizing higher-margin products and limiting output growth.

The result is a textbook commodity upswing with extreme operating leverage. SanDisk’s cost base is relatively fixed, so rising NAND prices flow almost directly to margins and earnings. The company has swung from a US$1.6 billion loss in fiscal 2025 to billions in profit, as pricing power and volume growth combined to drive explosive financial performance.

Revenue growth has mirrored the shift. In its most recent results, quarterly revenue reached roughly US$5.95 billion, up approximately 250 per cent year over year, with margin expansion approaching software-like levels.

In short, the rally reflects the market capitalizing a super-cycle.

Extreme price action meets extreme fundamentals

The mechanics of the move highlight the paradox. A 700 per cent rally and parabolic chart typically signal speculative excess—yet the underlying earnings expansion is real and dramatic.

SanDisk trades above the consensus analyst target range, a classic late-cycle indicator. At the same time, its earnings power complicates the “overvalued” narrative. With quarterly EPS above US$20 and rising, annualized earnings could approach US$90–US$100 if conditions hold—a level that implies a forward multiple in the low-to-mid 20s.

That valuation is not obviously excessive for a company delivering triple-digit growth and operating at the centre of AI infrastructure. But it is highly contingent on one assumption: that today’s pricing environment persists.

The cycle question: Structural shift or peak?

The core debate now centres on whether the NAND super-cycle is structural or cyclical.

Bullish arguments increasingly lean toward structural. Memory demand is being reshaped by AI, rather than traditional end markets like smartphones or PCs. Data centres have become the primary consumers of storage, and hyperscalers are locking in long-term agreements to secure supply.

Industry data supports the view of sustained tightness. TrendForce projects massive expansion in the global memory market, with revenue forecasts sharply revised higher due to AI-driven demand and limited supply growth.

At the same time, pricing trends remain aggressive. Enterprise SSD prices have already logged record increases, and suppliers maintain strong negotiating power as buyers compete for constrained capacity.

The bear case, however, is grounded in history. Memory remains a cyclical commodity business, and past cycles have ended with abrupt oversupply and price collapses. New capacity, particularly expected to ramp later in the decade, could eventually normalize pricing and compress margins.

In that scenario, current earnings would represent a peak rather than a baseline—and the stock’s valuation would look far less forgiving.

From data centres to living rooms: The US$3,000 SSD

The effects of the NAND shortage are not confined to enterprise markets. They are increasingly visible at the consumer level, thanks to SanDisk’s latest product launch.

This week, the company unveiled its officially licensed Optimus GX Pro 850P NVMe SSD lineup for the PlayStation 5 and PS5 Pro, with capacities ranging from 1TB to 8TB.

The headline number: the 8TB model is priced at approximately US$2,960—discounted from a listed price near US$3,700—making it more than three times the cost of a PS5 Pro console.

Even lower-capacity options are expensive by historical standards. The 2TB version sells for roughly US$760, exceeding the price of a standard PS5 with a disc drive.

Technically, the drive offers PCIe 4.0 performance with read/write speeds of roughly 7,300/6,300 MB/s and a heatsink designed for Sony’s (NYSE:SONY) consoles. But the specifications are broadly comparable to prior-generation drives that sold for a fraction of the price just a year ago.

The pricing highlights the severity of what some industry observers have dubbed the “RAMpocalypse.” AI-driven demand has tightened supply across the memory ecosystem, pushing costs higher for everything from hyperscale storage to consumer gaming hardware.

The ripple effects are visible across the industry. Console prices have risen, and hardware makers from Sony to Valve have adjusted pricing to reflect elevated component costs.

In that sense, SanDisk’s US$3,000 SSD is less an outlier than a signal: the memory shortage is now visible to end users.

Outlook: Opportunity and risk at extremes

SanDisk’s rally encapsulates both the opportunity and the risk inherent in the current market environment.

On one hand, the company sits at the centre of a powerful structural trend. AI infrastructure is driving unprecedented demand for memory, tightening supply, and delivering extraordinary margins for producers.

On the other, the stock’s trajectory reflects that optimism fully—and then some. A 700 per cent run driven by a commodity cycle leaves little room for error, particularly with macro variables like interest rates still in flux.

The near-term path may hinge on the Fed. The longer-term outcome depends on the cycle itself.

If the AI-driven shortage persists through the late decade, today’s earnings could prove durable—and the rally justified. If supply catches up and pricing normalizes, the current moment may mark a cyclical peak.

For investors, SanDisk has become the market’s clearest test case of a simple question: is this the beginning of a new memory paradigm—or the top of an old one repeating at unprecedented scale?

About SanDisk

SanDisk stock (NASDAQ:SNDK) closed Wednesday more than 4 per cent higher, then carried that momentum into Thursday, opening more than 6 per cent higher at US$2,044.75 and has also risen more than 4,000 per cent since this time last year.

SanDisk Corp. develops, manufactures, and sells data storage devices and solutions using NAND flash technology. The company offers solid state drives for desktop and notebook PCs, gaming consoles, and set top boxes.

Join the discussion: Find out what the Bullboards are saying about SanDisk and check out Stockhouse’s stock forums and message boards.