Are you wondering what the Halloween Effect is and if it’s more than an old tale from centuries ago? Perhaps it’s a coincidence, or is it rooted in truth and facts?

What is the Halloween Effect?

The Halloween Effect is an investing theory suggesting that stocks perform better from Oct. 31 to May 1 than during the rest of the year. On the flip side of the Halloween Indicator is the “sell in May and go away” theory, advising investors to stay in the market during the winter months and exit during the summer.

Research papers and articles have dived into the theory for years. Despite a consensus on winter months as the time to be in the markets, the explanations are inconclusive, making it an unsolved mystery perfect for the Halloween season.

To gain some clarity, we look at the theory’s history and reference some statistics in the video above and the story below. Thus, giving clues to decide if this is a spooky spirits thing, a coincidence, or explained by some well-plotted research.

Halloween Effect history

Its origins date back more than a century, particularly in the United Kingdom, noticeable since 1684.

Wealthy investors would leave cities for their country estates during summer, leading to lower market activity. When they returned in the fall, the influx of capital often increased market liquidity. This seasonal behaviour was noted as early as the 1930s in publications such as The Scotsman. Following which, the phrase gained popularity in post-war newspapers.

“Many recall the old adage of the stock exchange ‘sell in May and go away,’ but there is something more than a normal summer holiday feeling in markets now.”

Unnamed “Special Correspondent” for The Scotsman newspaper in Edinburgh, May 1938

Again in The Scotsman, April 1943: “Experience in the last two years indicates that stock exchange business has diminished during the summer months although the holiday problem is far less acute than in days before the war.”

On May 30, 1964, page two of The Financial Times noted, “The stock exchange world is in a sort of twilight state at the moment. The potential buyers seem to have “sold in May and gone away.”

By the late 1980s, this practice became known worldwide, and in 1990, the term “Halloween Effect” was coined in the book “Beating the Dow” by Michael O’Higgins. In Japan, “Setsubun tenjo, higan zoko” is the Japanese equivalent of “sell in May and go away. ” Reported by financial journalist Christopher Fildes in June 1989 in the British weekly, The Spectator.

Halloween Effect Research

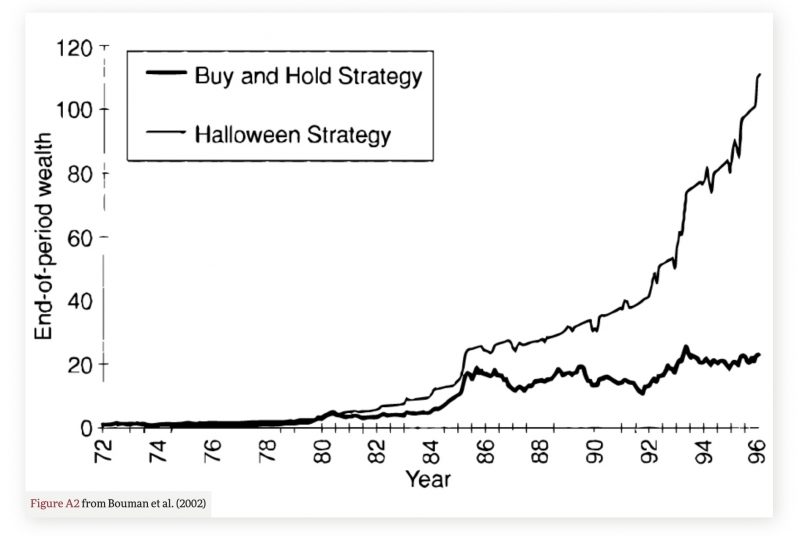

Research supports the Halloween Effect, notably a 2002 study by Sven Bouman and Ben Jacobsen published in The American Economic Review. Their findings indicate that selling in May can beat the market more than 80 per cent of the time over five years and more than 90 per cent over 10 years. They also found that stock market returns were significantly higher from November to April compared with May to October across 36 out of 37 markets studied.

Another example, the Dow Jones Industrial Average rose by 14 per cent from January through April but only 1.2 per cent from May to September. Similarly, the S&P 500 saw a 17.5 per cent increase from January to April. This compared with just 1 per cent in the summer months.

Investors who subscribe to this theory typically choose defensive stocks (stocks that provide consistent dividends and stable earnings regardless of the overall state of the stock market) during the summer hiatus. This is contrary to the buy and hold strategy – where the stocks are not sold in the summer months, rather the investor might ride out down months and invest for the longer term.

In some cases, the difference in performance can be significant. For example, between 1972 and 1996, investors using the Halloween strategy would have seen returns of nearly 120 per cent compared with roughly 20 per cent for investors who chose to buy and hold throughout that period.

Why it might work

Several explanations have been proposed on why the Halloween Effect might work.

1. Investor Behaviour: Many investors take vacations in the summer, leading to lower trading volumes and potentially poorer performance.

2. Seasonal Economic Factors: Changes in consumer behaviour and agricultural cycles during summer months might also play a role.

3. Historical Patterns: Historical data shows that stocks rose 65 per cent of the time from late October to early May. This compared with 58 per cent from May to October between 1920 and 1970.

In the Journal of International Money and Finance, The Halloween indicator, “Sell in May and Go Away”: Everywhere and all the time, Cherry Zhang and Ben Jacobsen revisit the original research publication. They re-examine the Halloween Effect puzzle using all historical data available from all countries worldwide. This in response to one of the big critiques that the sample size that was U.K.-focused.

The results highlight that developed markets exhibit a stronger Halloween Effect. Also, that the data for these markets is often more robust compared with emerging or less studied markets. The analysis across 37,167 monthly returns confirms that returns generated from November-April contribute positively to the market risk premium. While summer returns are not only lower but negative compared with risk-free rates. This, supporting the efficacy of seasonal strategies such as the Halloween indicator.

Halloween Effect critiques

Despite the evidence, some researchers argue the Halloween effect might not be as reliable as it seems. Events such as the 1987 Black Monday crash could skew results. Additionally, as more investors become aware of the strategy, its effectiveness may diminish because of the efficient market hypothesis. Thus suggesting that known patterns are quickly priced into the market.

A most curious tale

The Halloween Effect presents an intriguing market anomaly and a most curious tale. While historical data suggests it offers stronger capital gains during certain months, investors should exercise caution and conduct thorough research.

Join the discussion: Find out what everybody’s saying about public companies and hot topics about stocks at Stockhouse’s stock forums and message boards.

The material provided in this article is for information only and should not be treated as investment advice. For full disclaimer information, please click here.