With gold hitting an all-time high of US$2,346 per ounce on April 26, while blazing a clear path to US$3,000 thanks to ballooning U.S. debt, global geopolitical tensions, falling global interest rates, rising circuitry demand for AI models, and robust central bank purchases as a reserve asset, the opportunity for investors to capture added leverage through gold stocks hasn’t been this enticing since 2007’s Global Financial Crisis.

This is especially true because of physical gold. Gold stocks have a history of outperforming after lagging periods – the last of which has been ongoing since 2021 because of diverted demand into crypto and gold ETFs – creating what Sprott Asset Management describes as the greatest disconnect it has seen in its 25 years of tracking gold.

If investors stay true to business fundamentals, favouring top jurisdictions, growth, profitability, and seasoned management to keep operations humming, they stand to reap multi-bagger returns in the gold stock space.

A decade-long track record on a path to mid-tier production

A compelling mining stock to consider under this gold-equity dislocation thesis is Mandalay Resources (TSX:MND), a Canadian-based producer operating its Björkdal Gold Mine in Sweden and Costerfield Gold-Antimony Mine in Australia, both generating encumbered cash flows and 100 per cent owned.

Mandalay has been in production for more than 10 years, including four consecutive years of profitability since 2020, with an established run-rate between 80,000-100,000 ounces of gold equivalent (AuEq) per year. Output is expected to reach 90,000-100,000 ounces AuEq in 2024, supported by value-accretive estimates in line with decade-long averages (slide 6), including:

- Average cash costs of US$1,050 – US$1,170 per ounce AuEq

- Average all-in sustaining costs of US$1,450 – US$1,580 per ounce AuEq

Despite Mandalay’s profitable production history, its share price remains relatively undervalued in the junior mining space, positioning shareholders to build an underpriced position before gold stocks revert to the mean. A shift seems to have already begun, based on a 12.5 per cent gain for the PHLX Gold and Silver Index, which tracks 30 gold and silver mining companies, versus a 6.3 per cent gain for the SPDR Gold ETF from February 20 to March 20, 2024.

With 25,000 ounces AuEq already produced in Q1 2024 and a consolidated exploration budget of US$12 million-US$15 million for the year – well beyond its average annual spend of approximately US$7.5 million since 2015 – Mandalay remains focused on numerous opportunities at Costerfield and Björkdal to extend known mineralization and make near-mine discoveries, in addition to a strong inorganic growth pipeline, with eyes on becoming a mid-tier critical metals producer over the next few years.

Let’s take a closer look at Mandalay’s two flagship assets to better understand the value shareholders stand to reap.

The Björkdal Gold Mine

The 12,949-hectare Björkdal land package resides in the Boliden mining district, 28 kilometres northwest of Skellefteå, Sweden, where it has been in operation since 1983 near numerous world-class volcanogenic massive sulphide (VMS) copper, zinc and lead deposits that have been developed for more than a century.

Mandalay acquired Björkdal in 2014, operating it as an open-pit and underground mine until 2019, when it transitioned to exclusively underground operations to eliminate high open-pit costs and process higher-margin ore from stockpiles and the Aurora zone. Production stems primarily from the underground zones (70 per cent), in addition to a meaningful contribution from a stockpile of low-grade material (30 per cent), with processing capacity expected to reach 1.45 million tonnes per year by Q2 2024.

The Björkdal gold deposit is found within quartz veins up to several decimeters in width that yield ore for four concentrates currently sold in Sweden and Germany. Interim Mineral Reserves and Mineral Resources as of December 31, 2023 and December 31, 2022, respectively, using a gold price of US$1,800 per ounce, read as follows:

- 490,000 ounces of proven and probable gold reserves (1.5 million tonnes at 1.32 g/t gold)

- 1.21 million ounces of measured and indicated (M&I) resources

- 265,000 ounces of inferred resources

Currently boasting a 9-year life-of-mine, Mandalay has consistently replaced reserves and increased M&I resources at Björkdal since 2015 at a competitive discovery cost of US$15 per ounce AuEq (2016 to 2023). A few highlights from last year’s drilling campaign include:

- Intercepts up to 783 g/t gold and 89.5 g/t gold from the Eastern Plunge Extension and Aurora Upper Extension, respectively, in February 2023

- Extended mineralized veins at the Eastern Extension Zone up to 116.8 g/t gold and greater evidence for mineralized continuity at the North Zone up to 207 g/t gold in July 2023

As a high-tonnage and low-grade gold mine, these results suggest that Björkdal can drive significant profit growth by favouring higher-grade areas, a strategy management is actively pursuing in 2024 to maximize profit margins.

Björkdal achieved production of 11,558 ounces in Q4 2023, including revenue of US$22.1 million, a 42 per cent increase year-over-year and its strongest quarter since Q1 2022, thanks to elevated gold grades, particularly from the Eastern Extension zone.

Full-year 2023 production reached 42,148 ounces, at AISC of US$1,751 per ounce and cash costs of US$1,354 per ounce, and is expected to grow to 43,000-47,000 ounces in 2024, at AISC of US$1,690-US$1,850 and cash costs of US$1,270-US$1,390. Production is well on its way to meeting 2024 guidance, with a Q1 2024 yield of 10,370 gold ounces, a 16 per cent increase year-over-year, with US$3 million-US$4 million earmarked for exploration throughout the year.

Key focuses for high-grade resource growth in 2024 (slide 17) include the Eastern Extension, which is open at depth, and new domains near the North Zone and Boreal Zone, while bulk mining growth will be sought by extending the Aurora Zone.

In terms of regional exploration in 2024 (slide 18), Mandalay will concentrate its efforts on Björkdal-style gold identified through mapping, base-of till-drilling and historic diamond drilling to the east of the mine, and Boliden-style VMS copper-gold to the southwest of the mine, while practicing its ongoing target-generation process based on base-of-till drilling, ground magnetics and induced polarization surveys.

The company is updating a long-term block model, which will include drilling up to September 2024, for the filing of a new mineral resource estimate and NI 43-101 technical report slated for March 2025.

The Costerfield Gold-Antimony Mine

Purchased in 2009, the 1,293-hectare Costerfield project is in the mining mecca of Australia, specifically in the Victorian Gold Belt, which has yielded more than 55 million ounces in historical production.

The project, only 30 km from Agnico Eagle’s high-grade Fosterville Gold Mine, boasts reserves and resources as of Dec. 31, 2023, that read as follows:

- 188,000 ounces of gold and 10,600 tonnes of antimony (559,000 tonnes at 10.5 g/t gold and 1.9 per cent antimony) of proven and probable reserves, supposing US$1,800 per ounce of gold and US$11,500 per tonne of antimony

- 330,000 ounces of gold and 28,800 tonnes of antimony (965,000 tonnes at 10.6 g/t gold and 3 per cent antimony) of measured and indicated resources, and 64,000 ounces of gold and 5,100 tonnes antimony of inferred resources, supposing US$1,900 per ounce of gold and US$12,000 per tonne of antimony

Mandalay has consistently maintained a 2- to 5-year reserve life at Costerfield since 2012 (slide 14), including a 3.5-year estimate as of 2023, averaging more than 500,000 ounces AuEq over the period at an average discovery cost of only US$45 per ounce of measured and indicated resources (2010-2023).

The company has depleted about 60,000 ounces AuEq per year for a total of 940,000 ounces since 2010, while defining a resource of more than 1.3 million ounces to date, with a gold concentrate sold locally to a refinery in Melbourne, and a gold-antimony concentrate shipped from Melbourne to smelters in China and Oman.

Mandalay is Australia’s sole producer of antimony, generating up to 5 per cent of global supply per year. The material commands a high price and has posted a strong performance from about US$7,000 per tonne in 2021 to US$13,500 per tonne as of April 2024, thanks to high demand, a dwindling global supply, and its varied uses as a fire retardant, hardener for solar panel glass, and in lead-antimony alloys to improve batteries’ electrical conductivity, including those of electric vehicles.

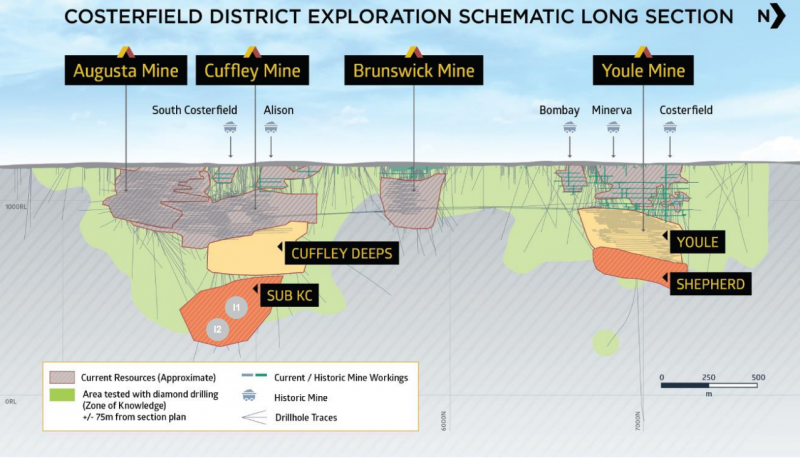

Production is focused on high-grade material from the Youle and Shepherd deposits, as well as the Augusta mine, to expand mineral reserves and optimize Costerfield’s 150,000 tonnes per year processing capacity at its Brunswick plant.

Production in 2023 reached 47,661 ounces AuEq (36,057 ounces of gold and 1,860 tonnes of antimony), at AISC of US$1,113 per ounce and cash costs of US$876 per ounce, with a highlight of 15,383 ounces AuEq in Q4 2023, including Mandalay’s highest quarterly gold production since Q4 2021 at 13,016 ounces. Output at Costerfield in Q1 2024 came to 14,566 ounces AuEq, about 32 per cent higher year-over-year.

Full year 2024 production, estimated at 47,000-53,000 ounces AuEq, with AISC of US$1,080-US$1,260 and cash costs of US$850-US$970, positions Mandalay stock for a positive re-rating, driven by increased profits and potential resource expansion, should gold hold at its generationally high price.

Targets for life-of-mine extension in 2024 (slide 12), backed by US$9 million-US$11 million in exploration expenditures, include prospects near multiple Shepherd veins grading as high as 797 g/t gold, indications of Shepherd and Youle-style veins at depth and to the north of Brunswick as high as 25.5 g/t gold, and testing of the northern extension of the Cuffley Deeps and Sub KC, the latter of which intercepted 1,361 g/t gold over 0.09 m and 259 g/t gold over 0.19 m.

When it comes to regional exploration targets in 2024 (slide 13), Mandalay has its sights set on True Blue, a new production corridor over 1.5 km in strike length near the Youle workings grading up to 20.2 g/t gold and 20.3 per cent antimony, northern and southern extensions of the Brunswick Line, and a new potential domain at the Costerfield Plunge, continuing the company’s monumental 82.9 km of exploration diamond core across 2022 and 2023 combined.

The rarified air of profitable microcap mining stocks

With less than 1 in 10,000 mineral exploration projects going on to become a mine, only a handful of mining stocks can rely on profits and revenue as a means of investor evaluation, many of which are billions of dollars larger than Mandalay in terms of market capitalization.

Coming in at C$221.16 million as of April 26, the gold producer offers exposure to a solid track record of profitability, including US$95.56 million in net income and more than US$60 million in free cash flow (2021-2023) generated from US$773.41 million in revenue since 2020.

As of Q1 2024, Mandalay held a cash balance of US$47 million – a 133 per cent increase from US$20.2 million at year-end 2023 – while turning positive on a net debt-to-cash basis in the quarter (slide 7), fortifying the company with a strong balance sheet to execute on imminent drilling, delineate more resources and reserves, and strengthen its case for undervaluation at the current share price.

Leadership thriving through the test of time

Mandalay Resources’ stellar track record could, of course, not be achieved without a management team well-versed in mining operations, project development, financing and M&A at large and small companies.

Frazer Bourchier, Mandalay Resources’ president, director and chief executive officer, is a registered engineer with more than 33 years of global mining experience across operational field management and executive leadership. He previously served as:

- President, CEO and director of Harte Gold from 2020 to 2022

- Chief operating officer of Detour Gold from 2018 to 2019

- Chief operating officer at Nevsun Resources from 2012 to 2017

- An operational executive for two years at Wheaton Precious Metals (TSX:WPM)

- Mining manager and general manager at the Porgera open-pit gold mine in Papua New Guinea for Placer Dome (subsequently Barrick Gold (TSX:ABX))

Bourchier’s tailor-made expertise is supported by executives and directors keen on drawing a straight line between profitable production, operational cost controls, strategic exploration and long-term shareholder value creation. Meet them below:

- Bradford A. Mills, chairman, brings more than 40 years of experience in the resource industry, including as Mandalay’s CEO from 2009 to 2016, overseeing its transition to a producing gold company from 2010 onwards. From 2004-2009, Mills was CEO of Lonmin (GBX:LMI), the world’s No. 3 platinum and platinum group metals (PGM) producer. Before that, he served as president of the BHP Billiton copper group. Mills is currently a director of Rambler Metals & Mining (AIMM:RMM), a developer and explorer of base and precious metals in Newfoundland and Labrador, Circum Minerals, a private potash development company in Ethiopia, and CNM, a private nickel-copper-cobalt-PGM producing company in Zambia, as well as the founder and managing director of Plinian Capital, a private equity firm investing in natural resource projects and companies.

- Hashim Ahmed, chief financial officer, has more than 20 years of experience across management, accounting and corporate finance at Barrick Gold, Jaguar Mining (TSX:JAG) and Nova Royalties.

- Scott Trebilcock, executive vice president and chief development officer (CDO), has spent the past 25 years as a process engineer, management consultant and mining executive, including as CDO of Nevsun Resources, where he was responsible for strategy, corporate development and investor relations, as CEO of junior gold developer KORE Mining (TSXV:KORE), and as a founder and director of several other junior gold exploration companies.

- Ryan Austerberry, chief operating officer, boasts more than 18 years of experience in the resource industry across technical and managerial roles. He has worked for Mandalay since 2009, previously serving as corporate manager of technical services, as well as general manager of Björkdal and Costerfield.

- Chris Davis, vice president of operational geology & exploration, has spent more than 20 years in narrow-vein gold and polymetallic exploration, primarily in Europe and Eastern Australia.

- Åsa Corin, general manager at Björkdal, has accumulated 18 years of experience in the mining industry, including working as a geologist in Finland, Sweden and Western Australia.

- Adam Self, general manager at Costerfield, brings more than 25 years of resource industry experience, mostly in underground production, that has seen him progress from operator to supervisor to technical and mine management.

The company’s leadership team is rounded out by a board of directors made up of mining luminaries, including a second former Mandalay CEO, an advisor and asset manager for more than 20 years who cut her teeth at Morgan Stanley, a 40-year veteran across all facets of international resource exploration, development and production, a lawyer with more than 25 years of corporate legal experience in the mining industry, and a chartered accountant who has raised more than US$750 million and played key roles in several billion dollars’ worth of corporate transactions.

Guided by the focus on optimization that only a few centuries of specialized knowledge can bring, Mandalay has shown itself to be a reliable cash generator with plenty of room to grow, as it explores its more than 14,000-hectare land package and increases its upside to gold’s ongoing bull run.

A stock on the verge of wider market recognition

As should now be evident, though Mandalay stock remains undervalued, it offers an abundance of catalysts for a re-rating, including mines with proven production and expansion potential, profitable operations, and a management team that substantiates its experience on the income statement.

The stock is further de-risked by 76 per cent institutional ownership, spread across Plinian Capital’s CE Mining (25 per cent), GMT Capital (20 per cent), Ruffer LLP (19 per cent), and AzValor (12 per cent), in addition to a buy rating from Brian Quast, an analyst at BMO Capital Markets, and a share buyback program announced in February 2024, which proves management is well aware of the market’s unjustified reluctance to reward the company’s value-accretive results.

With MND shares having added only 138 per cent since 2019, tracking the past few years of profitability, investors are being gifted an opportunity to own a stake in a model miner, whose growth runway is only beginning to unfold.

Join the discussion: Find out what everybody’s saying about this microcap gold stock on the Mandalay Resources Bullboard, and check out Stockhouse’s stock forums and message boards.

This is sponsored content issued on behalf of Mandalay Resources, please see full disclaimer here.