Vonovia – It Sounds Like Market Logic

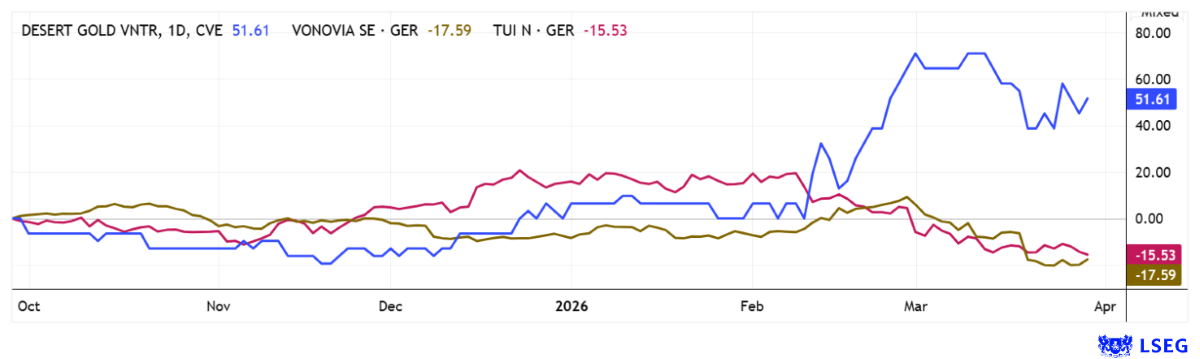

For those wondering why Vonovia’s stock has plummeted 25% in recent trading days, here is a logical explanation: Real estate stocks are, at their core, bets on interest rates. When interest rates fall, the boom begins for appreciation and fresh financing due to rising demand. However, if the government steps too hard on the debt pedal, as is currently the case, bond yields rise, which also leads to higher construction loan rates. It is also obsolete for the Federal Ministry of Construction to complain about insufficient investment in housing construction, because it is precisely the government’s overreach in other sectors that is catapulting long-term interest rates upward, to well over 3%. As a result, 10-year mortgages are broadly reaching the magic 4% mark, even if rates are still lower in some cases.

When Vonovia recently presented its figures for 2025, analysts reacted positively, as the results were not that bad. EBITDA rose by 6% to EUR 2.8 billion, and the average rent per square meter also increased by 4.6%. After two difficult years, portfolio values rose by 1.8% on a comparable basis, while the total value of the portfolio increased by 3% to EUR 84.4 billion. The dividend is also set to rise to EUR 1.25. The fly in the ointment is likely still the high loan portfolio and the resulting debt ratio of 45.4%. CEO Luka Mucic aims to raise around EUR 5 billion through portfolio sales to reduce debt. One can only hope that market conditions will allow for this plan. Investors are likely anticipating much tougher times and have been selling the stock in large numbers. The share price fell from EUR 29.50 to EUR 20.50 in just 5 trading days. On the LSEG platform, 15 out of 24 analysts remain bullish and expect prices around EUR 32. It will be interesting to see what happens with the stock in the coming weeks, leading up to the AGM on May 21.

Desert Gold – A Breather

In January, gold stocks experienced an early spring. High spot prices, cheap fuel, and low interest rates boosted the economic analyses of many deposits. Prices exceeding the USD 5,000 mark fundamentally changed the calculations for many projects: Properties that offered only marginal prospects just a few years ago now achieved significantly more attractive return metrics. With the Iran conflict, the parameters changed dramatically. Now, precious metal prices have consolidated significantly, interest rates have reached new highs, and fuel is suddenly 60% more expensive than it was at the start of the year. No wonder that the share price of a small explorer like Desert Gold fell by a full 30% within three weeks.

However, there is no rationality behind this movement, as the development of the Barani East project in western Mali follows a strict, capital-disciplined approach. Strategically, it is located in close proximity to established producers such as Barrick Gold and B2Gold along the Senegal-Mali Shear Zone, one of Africa’s most productive gold structures with a cumulative annual output of several million ounces. Currently, work is focused on building logistical infrastructure, while a modular processing plant is being constructed in parallel. Even in the first phase of expansion, it is expected to process approximately 10 tons of ore per hour, and an option to increase capacity fivefold is already in place. The project development is based on a feasibility study updated in 2026, which, using a conservative gold price of around USD 2,850 per ounce, demonstrates a robust net present value and a double-digit internal rate of return. If, on the other hand, the gold price rises by a further 10–15%, the project value increases disproportionately, as fixed costs remain largely constant and every additional dollar in the selling price directly impacts the margin.

From an analytical perspective, management aims to generate positive operating cash flow as early as possible and then gradually scale up production. Major producers in the area might take notice at this point, as they need to replace their reserves given that the average lifespan of many mines has fallen sharply. This increases the likelihood of acquisitions of smaller projects as soon as they appear economically viable. The crux lies in the size of the license area, totaling 440 sq km. After all, only 10% of the land area has been explored so far, which leaves plenty of room for imagination. The fact that Desert Gold is trading at CAD 0.12 with a market capitalization of just CAD 45 million is a fortunate circumstance that investors should take advantage of right now. The research firm GBC expects a 650% increase in value within the next 12 months!

IIF host Lyndsay Malchuk in conversation with CEO Jared Scharf about the outlook for current projects in West Africa.

TUI – What do the Analysts Say?

Since the start of the Gulf crisis in early March, TUI shares have lost over 30% to around EUR 6.50. This is due to free rebookings, high cancellation costs, and rising fuel prices, which were not yet factored into trips booked earlier. In general, many analysts also fear that the surge in inflation will significantly dampen EU citizens’ desire to travel. The still-positive annual figures for 2025, with an operating profit of EUR 1.2 billion, could therefore quickly turn sour if the pressures persist throughout the year. The fortunes of the TUI stock thus appear to be directly linked to the resolution of the Iran conflict, as the sooner normality returns, the faster the operational turnaround can be achieved. Despite all the difficulties, however, optimism still prevails among analysts. 12 out of 16 experts are giving it a thumbs-up and expect an average 12-month target price of no less than EUR 11.24, a full 75% above the current price. “Buy when the cannons roar” is a stock market adage that could very well apply here!

Difficult times have often been the best entry points in the stock market in the past. Whether this will pay off for Vonovia or TUI in the short term remains to be seen, as this would likely require interest rates to fall again and the Iran conflict to be resolved. However, if Desert Gold commissions its processing plant and can sell the first ounces at current prices, then investors should sharpen their pencils and take another closer look at the latest sensitivity analysis.

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as “Relevant Persons”) currently hold or hold shares or other financial instruments of the aforementioned companies and speculate on their price developments. In this respect, they intend to sell or acquire shares or other financial instruments of the companies (hereinafter each referred to as a “Transaction”). Transactions may thereby influence the respective price of the shares or other financial instruments of the Company.

In this respect, there is a concrete conflict of interest in the reporting on the companies.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is also a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.

Stockhouse does not provide investment advice or recommendations. All investment decisions should be made based on your own research and consultation with a registered investment professional. The issuer is solely responsible for the accuracy of the information contained herein. For full disclaimer information, please click here.