Bayer: Transformation and Validation in Europe

Since Bayer is already adapting this technology for the European market and Sumitomo is handling distribution in the Americas, MustGrow bridges the gap between ecological research and practical application in the fields. For investors, MustGrow’s business model offers significant opportunities, as the company delivers precisely the innovations that large corporations urgently need to meet regulatory requirements. As an agricultural innovator and a multi-billion-euro corporation, Bayer is driving the transformation toward regenerative agriculture. To increase its own efficiency, the company has introduced the so-called Dynamic Shared Ownership model, which is expected to enable cost savings of around EUR 2 billion by the end of 2026. At the heart of the strategic realignment of the Crop Science division is the expansion of the portfolio in the biologicals sector. To meet the strict regulatory requirements in the Europe, Middle East, and Africa (EMEA) region, Bayer signed an exclusive licensing agreement for MustGrow’s soil biocontrol technology. The German company is assuming all costs for field development, toxicology, and regulatory processes, which industry experts view as a strong vote of confidence in the technology’s effectiveness. The partnership also provides MustGrow with significant financial relief while opening access to one of the most strictly regulated agricultural markets in the world.Sumitomo Revs Up Its Sales Engine

On the sales side, the Japanese conglomerate Sumitomo is positioning itself and accelerating the agricultural transition. To consolidate growth in the biologics segment, the group recently officially launched the new Sumitomo Biorational Company, which is intended to serve as a global center of excellence for biological innovations and aims for revenue of up to USD 1 billion by 2030. Through an exclusive agreement, Sumitomo secured the distribution rights to MustGrow technology for North, Central, and South America, with a commercial focus on high-value crops such as potatoes and bananas. The Japanese giant’s key competitive advantage lies in its control of the last mile to the farmer through high-performance distribution networks such as Helena Agri-Enterprises in the US and Agro Amazonia in Brazil. This is intended to rapidly bring MustGrow’s innovative formulations into widespread agricultural use.MustGrow Biologics: Nature as a Highly Effective Technology

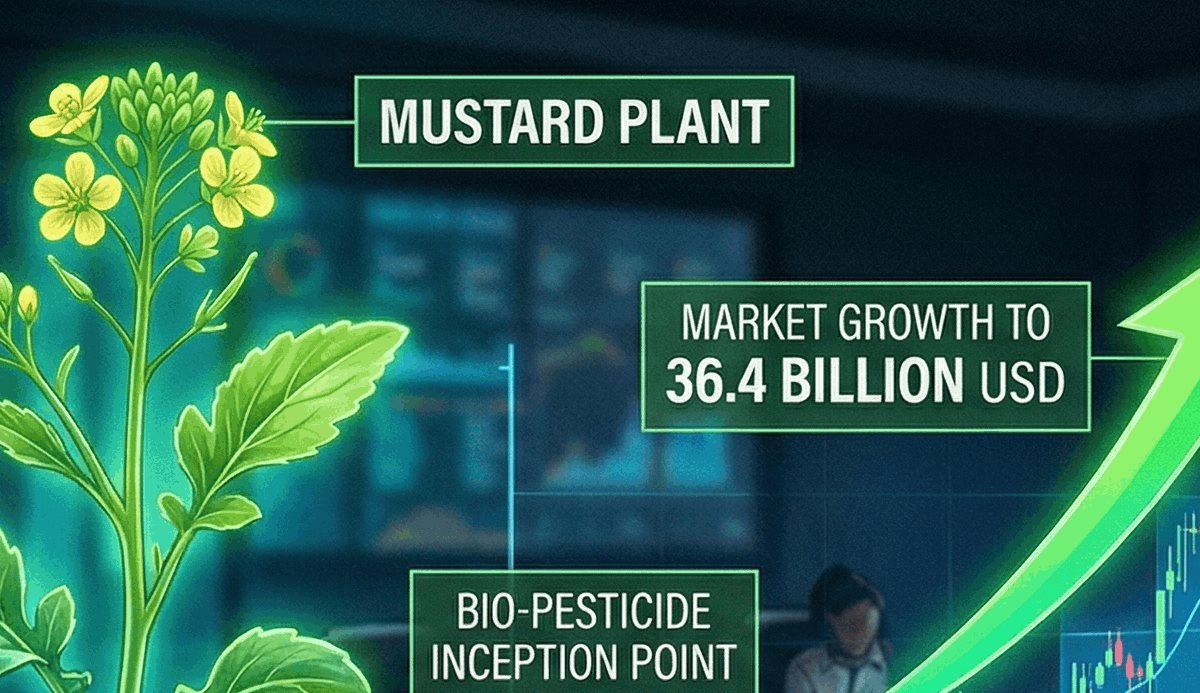

With its patented active ingredient platform, MustGrow Biologics is driving the shift in agriculture toward more sustainable practices. The technology harnesses the natural defense mechanism of the mustard plant and stabilizes the active ingredient in a liquid form that integrates seamlessly into existing irrigation systems. Unlike highly toxic and increasingly banned synthetic fumigants such as methyl bromide, MustGrow’s biological product acts selectively against harmful fungi and nematodes while sparing beneficial microorganisms in the soil. This is intended to control pests and preserve soil quality, which benefits yields in the long term. To accelerate commercial scaling, the company recently shut down its low-margin third-party distribution operations to channel all resources into the lucrative production of its own biofertilizer, TerraSante. Instead, strong partners such as Sumitomo will handle distribution. With key certifications for organic farming in US states like California and Florida, the product is meeting high demand. Although MustGrow is a small company, these partnerships, combined with its effective product, position the company as an agile technology provider that is also becoming increasingly attractive to investors.

Market Growth Offers Return Opportunities

Current market studies confirm the economic appeal of this business model. Market researchers at Precedence Research forecast that the global market volume for biopesticides will grow to over USD 36.4 billion by the middle of the next decade, representing annual growth of over 15%. Research by the consulting firms McKinsey and BCG also confirms that agricultural companies that switch to specialized biological products early on can generate significantly higher returns for their shareholders than traditional chemical suppliers. In this market environment, with a current market capitalization of approximately CAD 37 million, MustGrow offers risk-aware investors a rare opportunity: While industry giants like Sumitomo and Bayer already seem convinced, the market has so far been cautious regarding MustGrow stock. This could present an opportunity.Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as “Relevant Persons”) may hold shares or other financial instruments of the aforementioned companies in the future or may bet on rising or falling prices and thus a conflict of interest may arise in the future. The Relevant Persons reserve the right to buy or sell shares or other financial instruments of the Company at any time (hereinafter each a “Transaction”). Transactions may, under certain circumstances, influence the respective price of the shares or other financial instruments of the Company. In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships. For this reason, there is a concrete conflict of interest. The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such. The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user. The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.Stockhouse does not provide investment advice or recommendations. All investment decisions should be made based on your own research and consultation with a registered investment professional. The issuer is solely responsible for the accuracy of the information contained herein. For full disclaimer information, please click here.