Buy SpaceX?

In episode 565 of the “Doppelgänger“ podcast, Philipp Klöckner analyzed SpaceX’s IPO in detail. One of Germany’s best-known AI experts and tech analysts views the largest IPO of all time rather critically—at least from a fundamental valuation perspective. In the short term, however, he still considers the IPO very likely to be successful. Even professional investors, who actually consider a valuation close to 100 times annual revenue absurd, are likely to subscribe to the stock. The reason is less a conviction in the business model than the expectation that Elon Musk’s fan base will buy the stock almost regardless of the price. In addition, large ETFs and index funds would have to acquire shares following an IPO, which could further drive buying pressure. Klöckner therefore even considers an initial valuation of USD 3 trillion or more to be possible. In the medium term, however, he sees significant risks. SpaceX’s growth is already slowing, while the potential of Starlink is limited in his view.

Future visions, such as data centers in space, are realistic in five years at the earliest and are therefore currently hardly relevant for valuation. He is also particularly critical of the AI division xAI. Although this area is apparently presented in the prospectus as the largest future market, Klöckner believes that Musk has practically already lost the AI race against competitors like OpenAI or Anthropic. As a result, a large part of the valuation is based more on hope and Musk’s storytelling than on solid operating metrics.

Space Stocks in Demand

The anticipated SpaceX IPO is currently shaking up the entire space sector and sending stock prices soaring. Investors are betting that a successful IPO could channel billions of dollars into the industry. Rocket Lab has been particularly in demand recently, with its stock rising by nearly 70% at times within just a few trading days, as has Intuitive Machines, which gained around 46% over the course of the month. Planet Labs also benefited from the new euphoria surrounding space stocks. The space hype has also reached Germany, with OHB’s stock doubling in May.

Space, Defence, AI, and More in One Stock

Almonty Industries shares offer an alternative way to profit from the space boom. The tungsten producer is currently ramping up production at its Sangdong mega-mine in South Korea, positioning itself to become the largest Western supplier of this critical raw material. Tungsten is also virtually indispensable in the aerospace and satellite industries. This is because tungsten has the highest melting point of all metals, is extremely heat-resistant, and is very dense. That is why it is used in rocket nozzles, engine components, heat shields, high-performance electronics, and radiation shielding systems, among other applications. Material requirements are rising massively, particularly for reusable rockets and hypersonic technologies. Added to this is the expansion of satellite networks such as SpaceX’s Starlink. Thousands of satellites require robust electronics, special alloys, and high-precision manufacturing components, in which tungsten often plays a central role.

And that is not the only thing pointing to a golden future for tungsten. It also plays a central role in other key industries. In the AI industry, the metal is needed, among other things, for the manufacture of high-performance semiconductors, chips and data center hardware, as tungsten is extremely heat- and current-resistant. At the same time, its importance in the defence sector is growing. Armour-piercing ammunition, hypersonic weapons, turbine technology, and military electronics all require tungsten.

At the same time, China has dominated global tungsten production until now. But that will likely come to an end in 2026. As mentioned, Almonty is not only ramping up the Sangdong mine but also expanding its mine in Portugal and plans to begin production in the US this year. It sounds unbelievable, but the Almonty mine will likely be the first producing US tungsten mine in a decade. Since 2015, the country has been completely dependent on imports. Incidentally, a new law will take effect in 2027, prohibiting the import of tungsten from China.

Tungsten Price Unbelievable

Anyone who thinks that gold and silver prices have risen sharply in recent years should take a look at tungsten. Currently, on the Rotterdam exchange, over USD 3,000 is being paid for 1 metric ton unit (MTU) of ammonium paratungstate, equivalent to 10 kg. At the beginning of the year, the price was USD 900, and just a few years ago, it was less than USD 300. Despite this unbelievable price surge, tungsten, unlike gold or silver, has not corrected in recent months.

Almonty built the Sangdong mine based on the prices at that time. As a result, the cost of tungsten production in South Korea stands at USD 126.8 per MTU. It is therefore no surprise that analysts expect Almonty’s revenue and profits to skyrocket in the coming years.

https://youtu.be/D39rKLK2MN0?si=7eQRjVzDKIGR8990

Analysts Expect Profits to Skyrocket

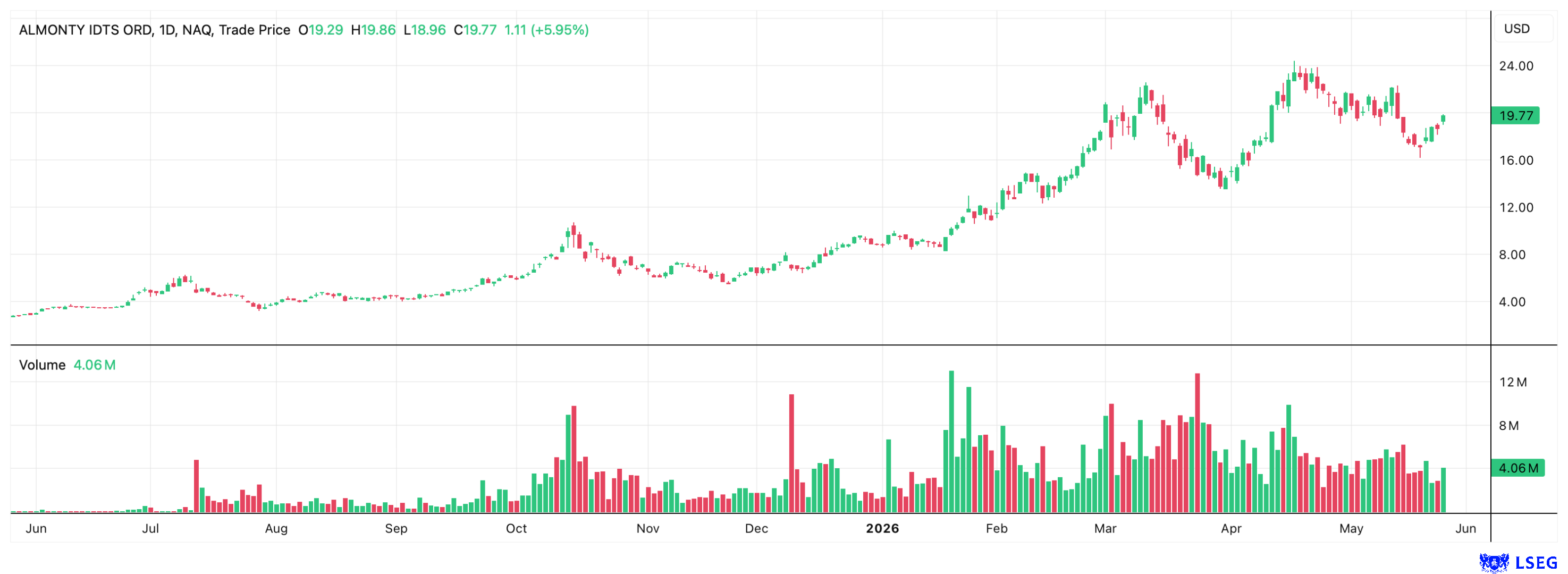

Most recently, analysts at Sphene Capital published an update on Almonty. The experts continue to see significant upside potential and reaffirm their “Buy” recommendation. Due to persistently strong tungsten prices, revenue and profit expectations have been raised, and consequently, the price target has been significantly increased from CAD 20.10 to CAD 37.40. Almonty shares are currently trading at around CAD 27.

Analysts expect Almonty to generate CAD 1 billion in revenue as early as next year. EBITDA is then expected to reach CAD 630 million, with net income at CAD 494 million. Revenue is projected to double again by 2028. EBITDA is expected to climb to CAD 1.39 billion in 2028, and net income to CAD 1.1 billion.

Conclusion: Stock Appears Undervalued

Almonty is currently operating in an ideal environment. With tungsten, the company produces a critical metal for numerous key industries, is practically the only serious producer in the West, and is significantly ramping up production. Against this backdrop, Almonty shares continue to appear undervalued. For 2027, Sphene analysts expect earnings per share of CAD 1.75, and for 2028, CAD 3.90. This implies a P/E ratio of 15.4 for 2027 and 6.9 for 2028.

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as “Relevant Persons”) may hold shares or other financial instruments of the aforementioned companies in the future or may bet on rising or falling prices and thus a conflict of interest may arise in the future. The Relevant Persons reserve the right to buy or sell shares or other financial instruments of the Company at any time (hereinafter each a “Transaction”). Transactions may, under certain circumstances, influence the respective price of the shares or other financial instruments of the Company.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.

Stockhouse does not provide investment advice or recommendations. All investment decisions should be made based on your own research and consultation with a registered investment professional. The issuer is solely responsible for the accuracy of the information contained herein. For full disclaimer information, please click here.