The global transition from fossil fuels to renewable energy, essential to prevent climate change, improve public health and preserve the environment for future generations, is often the subject of romanticized portrayals that ignore the underlying drivers of the shift away from carbon emissions, and with them the value-creation opportunities they present to the marketplace.

This article is disseminated in partnership with Nuclear Vision Ltd. It is intended to inform investors and should not be taken as a recommendation or financial advice.

Chief among these drivers is the resource industry, where the abundance of fossil fuels, which benefit from widespread infrastructure, stands in stark contrast to the increasing scarcity of minerals critical to renewable energy, which will be required in exponential quantities over the coming decades to reach net-zero emissions. According to the International Energy Agency, global critical minerals demand could quadruple by 2040.

Given the dangers of shouldering a critical minerals shortage, from environmental degradation to technological obsolescence, it’s no surprise that governments across the world are scrambling to secure high-quality supplies in safe jurisdictions. Key catalysts compounding this trend include:

- The fact that critical minerals production is concentrated in a small number of countries, many of which, including China and Russia, have proven reluctant to adhere to free market principles.

- A wave of protectionism spurred on by the COVID-19 pandemic, the US-China trade war, US President Trump’s global tariffs, as well as major armed conflicts ongoing in resource hubs such as Ukraine, Russia and the Middle East. And while Europe’s manganese supply doesn’t physically route through the Strait of Hormuz — with dominant suppliers like South Africa, Gabon, and Australia shipping via the Cape of Good Hope and Atlantic lanes — the simultaneous closure of Hormuz and resumed Houthi attacks on the Red Sea, now operating at 49 per cent of pre-crisis capacity, have eliminated both of the Middle East’s major maritime corridors at once. War risk premiums don’t respect clean geographic boundaries, and with Brent already up by more than 10 per cent since the strikes on Iran and natural gas prices in Europe rising even more sharply, bulk carrier capacity is tightening globally as tonnage diverts and insurers reprice entire ocean corridors — not just the strait itself. The net effect is higher CIF costs for manganese ore arriving at European steel mills, squeeze on spot-traded cargoes and upward pressure on ferroalloy pricing, which materially strengthens the offtake case for European domestic manganese supply with zero maritime exposure.

- New legislation, including a US executive order and the EU’s Critical Raw Materials Act, setting the tone for countries to keep their allies close and their enemies at an economically feasible distance.

This macroeconomic backdrop is, in turn, incentivizing investors to favor companies advancing critical minerals projects on clear development paths, under established rule of law, ideally positioned to contribute to and capitalize on the shift towards renewable energy production.

Introducing Nuclear Vision

A high-conviction candidate for investors to consider is Nuclear Vision (CSE:NUKV), market capitalization C$21 million, a junior mining company advancing three fundamentally sound, infrastructure-ready projects in Slovakia and Botswana prospective for some of the most important critical minerals underpinning the green energy transition.

Laying the groundwork for Europe’s manganese renaissance

The European Union, plagued by underinvestment in its mining sector, imports virtually all of its raw manganese from Gabon and South Africa, with most of its high-purity manganese stemming from China, whose stronghold on global processing capacity stands at more than 90 per cent.

With more than 113,000 tons purchased in 2023, this dynamic places the bloc in a precarious position within the mineral’s more than US$30 billion market, which is expected to grow steadily into the 2030s, driven by its critical roles across the modern industrial complex. Here’s a breakdown:

- Low-grade, oxide-based manganese reinforces steel’s hardness and corrosion resistance, making it an essential input for the production of everything from ships to military armor to city infrastructure.

- High-purity, carbonate-based manganese enhances stability, range and cost-effectiveness in lithium-ion and sodium-ion batteries, making it crucial to the growth of the energy storage and electric vehicle industries. The sub-type is also leading the charge towards more efficient technologies, such as lithium-manganese-ferro-phosphate batteries, a cheaper and more energy-dense alternative to conventional lithium batteries. Additionally, carbonate ore can be processed using sulfuric acid at greater efficiency than its oxide counterpart, which requires energy-intensive and high-emissions roasting, providing it with a downstream advantage. Given this outsized promise, Benchmark Mineral Intelligence is forecasting 8x growth in battery demand for manganese within this decade.

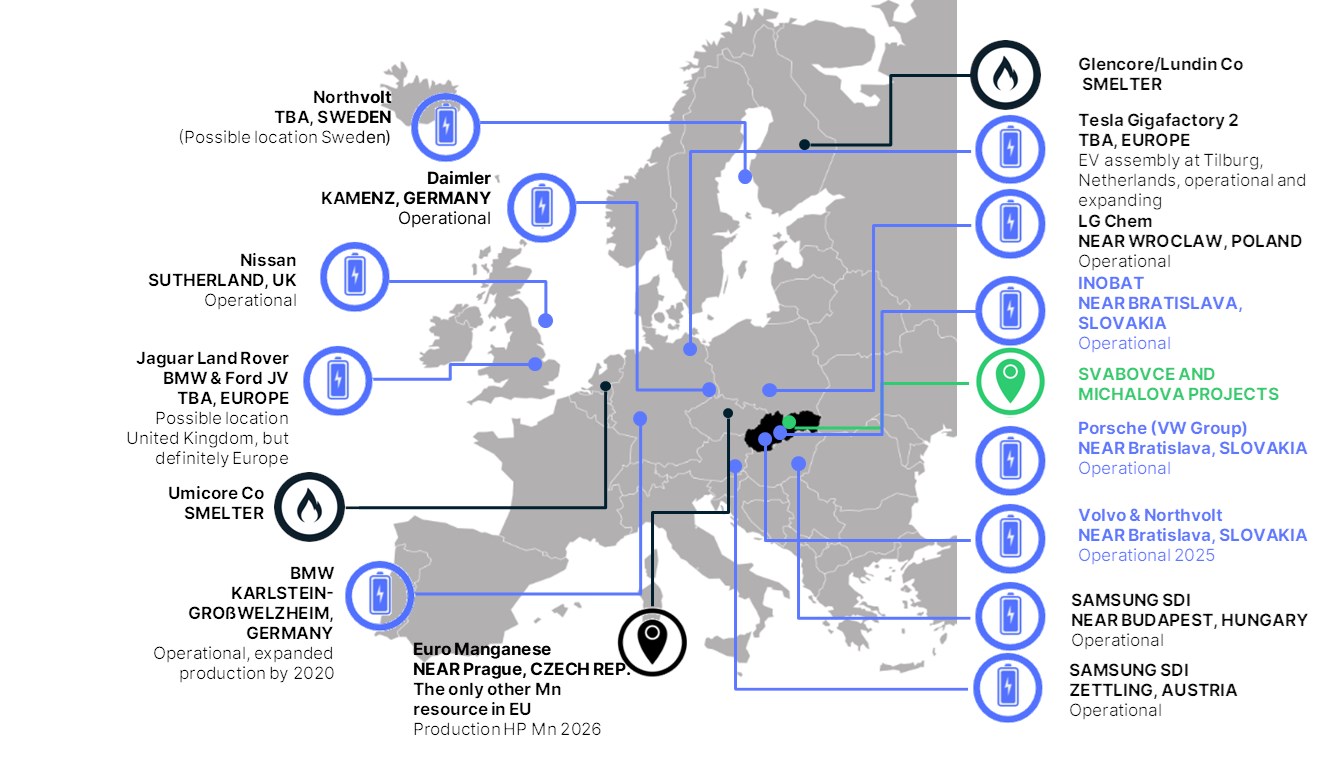

The symbiosis between manganese and the renewable energy transition, hindered by Chinese processing dominance, highlights the potential of Nuclear Vision’s 100-per-cent interest in the Michalova and Svabovce projects in Slovakia, which host two of the largest manganese deposits in the EU and are of the carbonate variety, putting them on track to play a vital role in EU supply chain independence.

The Michalova project

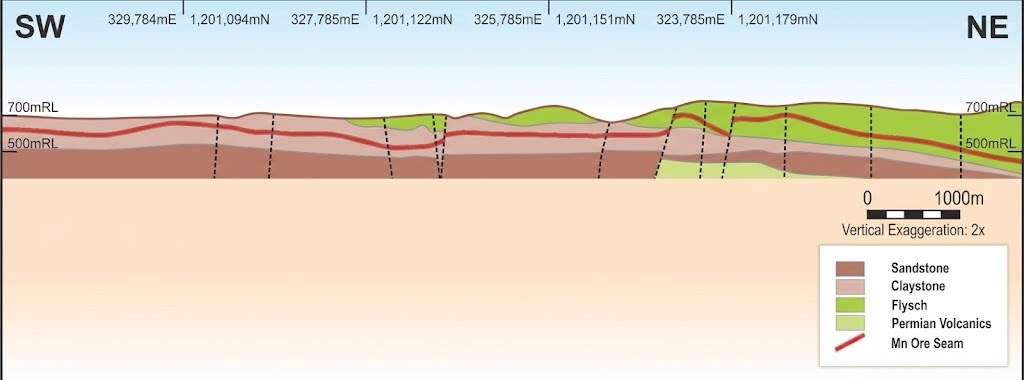

Michalova’s 14.34-square-kilometre tenement, located in the heart of Slovakia’s Battery Belt, hosts a historical resource estimated at 10.4 million tons grading 9.49 per cent manganese – constrained from surface to ~30 m depth – working out to 986,960 tons of the critical mineral. At a price of US$1,180 per ton in Q2 2025, according to data from imarc, this represents more than US$1 billion in commodities in the ground.

Like Svabovce profiled below, Michalova benefits from nearby rail, power and road networks, while residing less than 300 km from major automotive and battery manufacturing hubs – including the Gotion-InoBat gigafactory in Šurany and Volvo’s upcoming EV facility in Košice – significantly de-risking its development timeline and setting a strong foundation for potential offtake agreements.

Nuclear Vision also has a considerable amount of historical data in hand suggesting that Michalova’s substantial resource remains untapped, including initial metallurgical testing, evidence of small-scale mine workings, as well as two drillholes from 1954 indicating the presence of numerous separate manganese carbonate beds, including from ~30 m to 70 m depth in MS-1 and from ~40 m to ~200 m depth in M-171.

Leadership is planning further drilling to test the extent of these beds, with eyes on thoroughly assessing Michalova’s mineral potential and producing an NI 43-101 compliant resource estimate, should results warrant it, further aligning the project with European demand for high-purity manganese and the expediting of the renewable energy transition.

The Svabovce project

Nuclear Vision’s nearby Svabovce project boasts a hefty historical resource of its own, estimated at 13.9 million tons grading 14.47 per cent manganese, or 2,011,330 tons of manganese, representing more than US$2.3 billion in the ground, exponentially increasing the gap between the company’s market cap and the value of its assets.

The high-grade project, covering a 47.24-square-km exploration license with a four-year term, was open-cut mined from the 1850s to 1907, and mined underground until 1971, leaving approximately 35 km of underground workings fit for future mining.

Previous explorers also left an abundance of historical drilling data charting sediment-hosted manganese to up to 250 m depth, offering Nuclear Vision a prospective runway to pursue future exploration and a potential NI 43-101 resource estimate.

The company plans to explore Michalova and Svabovce drawing on a recently closed C$6 million capital raise, including a C$2 million investment from mining luminary, Eric Sprott, granting him a 12.8 per cent stake on a non-diluted basis and an 18 per cent stake on a fully diluted basis.

Sprott’s more than 50-year track record of identifying undervalued junior miners, both as an individual investor and through Sprott Asset Management, has created billions in market value, meaningfully de-risking Nuclear Vision’s growth plans.

A uranium project with potentially global relevance

Nuclear Vision will allocate a portion of the capital raise to exploring its UA92 project in Botswana, which makes a strong case for shoring up an oncoming uranium deficit expected to reach about 200 million pounds by 2040, as rising demand for AI technology, data center capacity and sustainable energy favors the radioactive metal’s high energy density and zero-emissions profile.

The project resides in a mining-friendly jurisdiction, located 350 km north of Gaborone and 75 km west of Francistown, with readily accessible power, road and transportation infrastructure, typifying Botswana’s long-standing reputation as a top mining jurisdiction. Perhaps most well-known for its diamond output, the Southern African nation is actively diversifying its exposure to the gemstone, with UA92 presenting itself as a key lever to unlocking vast untapped uranium reserves.

UA92’s 2,400-square-km land package is the largest in the Karoo Basin, where uranium mineralization is analogous to the Chu Sarysu Basin in Kazakhstan, responsible for producing ~21 per cent of the world’s uranium in 2025, drawing on more than 5 billion pounds in reserves, resources and production, including operations by Cameco. The project also neighbors Lotus Resources’ Letlhakane uranium project, hosting one of Southern Africa’s largest sandstone-hosted uranium deposits at more than 114 million pounds.

UA92 further enhances its value proposition with targets less than 400 m from surface, potentially enabling low-cost in-situ recovery, setting a positive tone for an ongoing high-resolution geophysical survey, based on historical drilling by Anglo American prospective for uranium mineralization, that will span 6,630 line-km across UA92’s three licenses.

With the survey kicking off in February as part of a comprehensive exploration program, including reconnaissance drilling planned for later in the year, Nuclear Vision is well-positioned to turn targets into positive news flow, guided by a leadership team with diversified commodity backgrounds and numerous discoveries to its name, including in the adjacent Aranos Basin, which shares Karoo’s geology and structural setting.

Nuclear Vision’s asymmetric growth runway

Having acquired Svabovce and Michalova for only €100,000 cash and 10 million common shares – valued at C$3.1 million as of March 10, 2026 – Nuclear Vision has left itself the vast majority of these projects’ multi-billion-dollar-potential to grow into, with a rich historic dataset to foster shareholder value by better delineating mineralization, harvesting exploration upside and validating a path to production.

If the company’s manganese projects alone, highly aligned with Germany’s new €3 billion EV stimulus package, point to its valuation rising multiples beyond its current market cap, the potentially transformational UA92 only extends this price-value dislocation further, with ongoing exploration across the project’s prospective geology likely to push the critical minerals stock higher.

Shares, however, down by 6 per cent since adopting the Nuclear Vision name in May 2025, have yet to reflect the underlying company’s solid fundamentals, discounting the combination of mineral-rich projects, long-term commodity tailwinds and a seasoned leadership team for exogenous reasons, including broader, risk-off sentiment stemming from Trump’s chaotic reorganization of global trade.

This dynamic clears the stage for investors who can recognize Nuclear Vision’s high-conviction value proposition and the inevitability of the renewable energy transition to put dry powder to work.

Join the discussion: Find out what investors are saying about this critical minerals stock on the Nuclear Vision Ltd. Bullboard and make sure to explore the rest of Stockhouse’s stock forums and message boards.

Stockhouse does not provide investment advice or recommendations. All investment decisions should be made based on your own research and consultation with a registered investment professional. The issuer is solely responsible for the accuracy of the information contained herein.

For full disclaimer information, please click here.