By Francois Kalos

In recent weeks, global markets have experienced significant volatility, with some indices correcting more than 10%, largely driven by growing concerns of a potential recession in the US. For long-term investors, these fluctuations often present opportunities to rebalance portfolios and invest in companies with solid long-term prospects, such as Silvercorp Metals (NYSE-A: SVM; TSX: SVM).

Silvercorp recently completed the acquisition of Adventus Mining, a copper-gold development company with a suite of projects in Ecuador. This acquisition strategically positions Silvercorp as a geographically diversified “green metals” company.

Why copper?

Copper’s significance in this day and age cannot be overstated. It is crucial for a wide range of applications, including construction, electronics, transportation and telecommunications. As a strong conductor and corrosion resistant green metal, it has become an essential component in electrical systems and wiring.

The “green revolution” and a push for renewable energy sources have further fueled the demand for copper as wind turbines, solar panels and electric vehicles require significant amounts of this essential metal in their production.

Additionally, with developing countries continually expanding their infrastructure, this will further increase the global demand for copper.

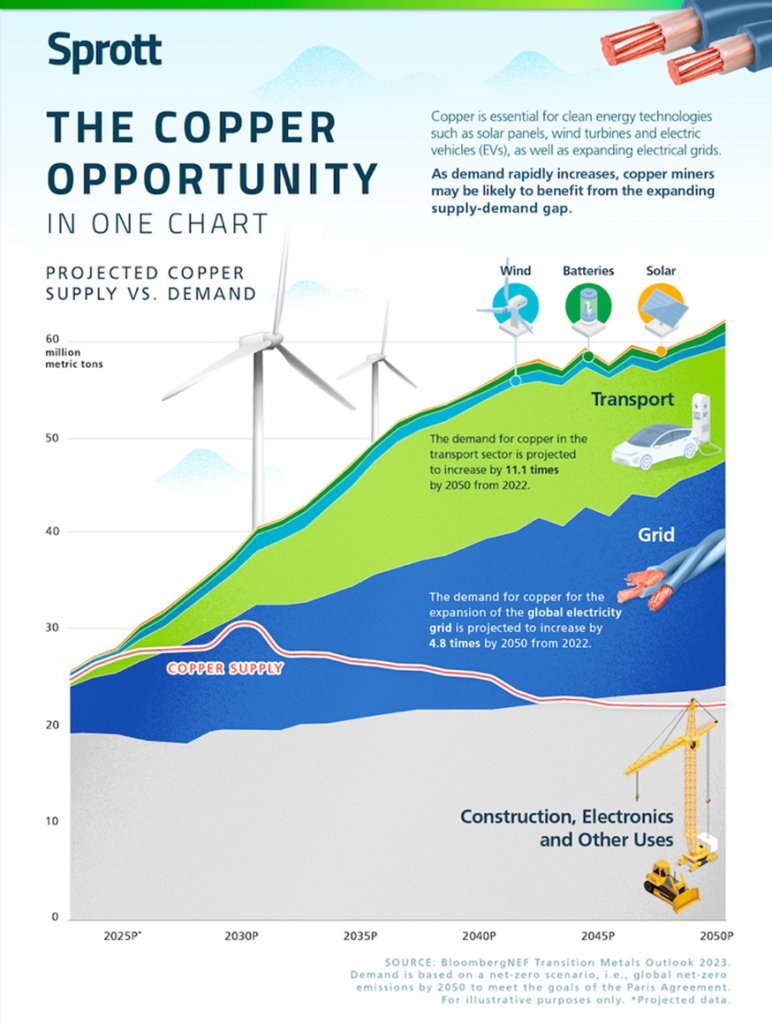

As outlined in the chart above and through extensive market research, copper is in the throes of an unprecedented supply/demand imbalance. While demand for the commodity continues to grow on a rapid trajectory, investment and production are still lacking amid political and financial challenges, due in part to the reluctance of major players to commit to new investment, as opposed to acquiring existing mines through mergers and acquisitions.

Investing in copper requires a long-term perspective. Global demand, supply disruptions and technological advances have a major impact on the price of copper, as well as market expectations about the global economic outlook.

Although current market conditions suggest short-term weakness in the copper market, the aforementioned fundamentals point to increased long-term consumption, with some analysts forecasting copper to exceed US$15,000 per metric ton in the next few years (up from the current US$8,200 per metric ton).

Exploring the benefits of the Adventus acquisition

Fully permitted de-risked copper-gold deposit

Silvercorp now owns a 75% interest in the fully permitted El Domo open pit copper-gold deposit with proven and probable mineral reserves of 6.5 million tonnes at 1.93% Cu, 2.52 g/t Au, 2.49% Zn, 45.7 g/t Ag and 0.25% Pb, which recently received government approval to commence mine construction and subsequent operation.

Low-cost production

The feasibility study for El Domo outlined a 10-year mine life with an average annual production of 10,463 tonnes of copper and 21,390 tonnes of copper equivalent over the life of the mine at production C1 cash costs of US$1.14/lb and an all-in sustaining cost (AISC) of US$1.26/lb copper equivalent.

Secured financing

Per the feasibility study, the initial capital cost (including refundable VAT) to build the El Domo mine is US $248 million, of which US$175.5 million will be funded by the existing Wheaton Precious Metals stream, with the remainder coming from Silvercorp – which has current cash and cash equivalents of approximately US$215 million on its balance sheet.

Strong economic projections

The El Domo feasibility study highlighted the project’s strong economics – projected payback period of 2.6 years, an after-tax IRR of 32% and a NPV8% of US$259 million using US$3.50/lb Cu, US$1,700/oz Au, US$1.20/lb Zn, US$23.00/oz Ag and US$0.95/lb Pb.

Blue sky potential

Silvercorp’s other newly acquired advanced project, the PEA-stage Condor gold deposit, has a projected 12-year mine life and average annual payable production of 187,000 ounces of gold and 758,000 ounces of silver at a by-product AISC of US$839/oz over the life of the mine.

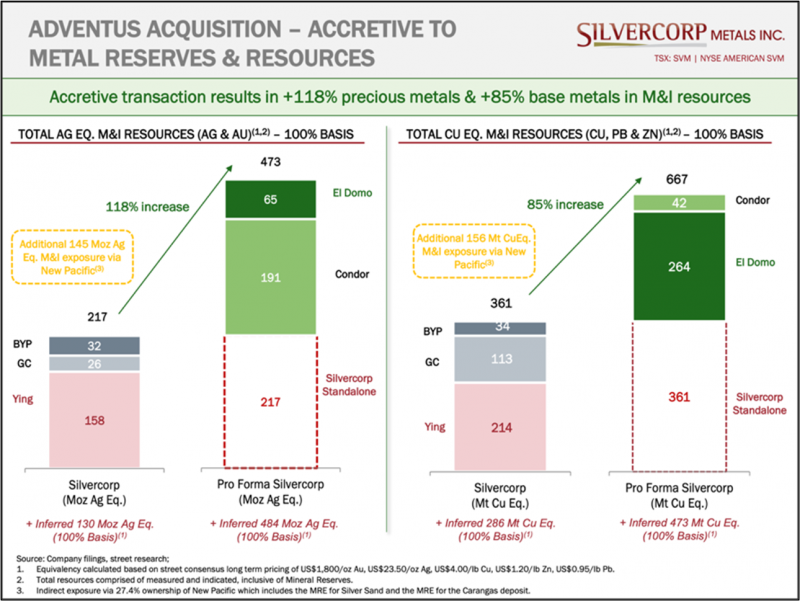

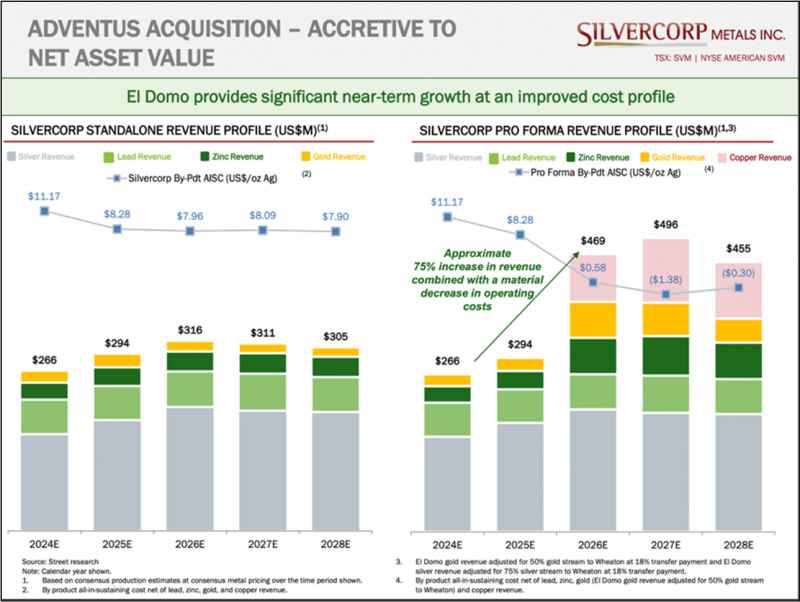

The acquisition of Adventus represents a pivotal and exciting milestone for Silvercorp and its shareholders, as the El Domo project provides immediate asset, geographic and metal diversification, with increased exposure to metals that are key to a low carbon future. It is accretive on both a net asset value/share and a mineral reserve/resource basis, with pro forma estimates showing over 118% growth in precious metal M&I resources and over 85% in base metal M&I resources.

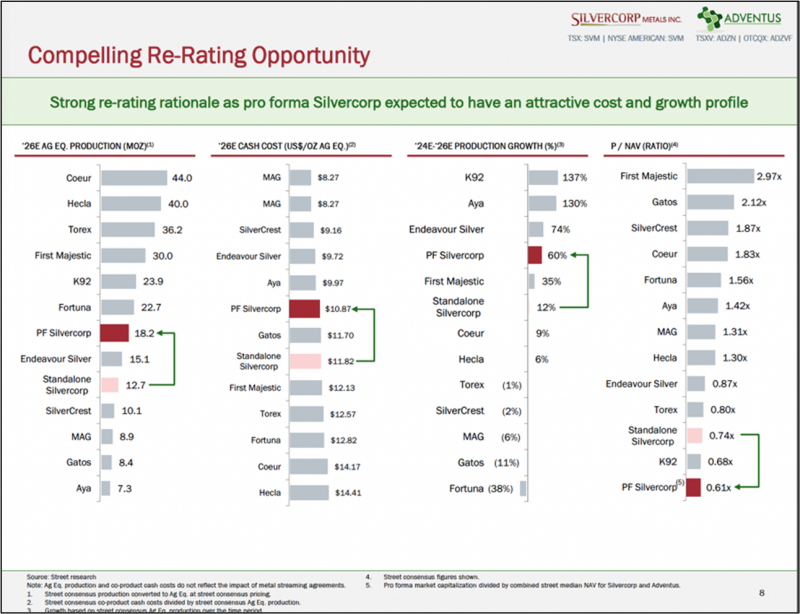

There is also a compelling re-rating opportunity relative to peers as Silvercorp’s pro forma is expected to present a more attractive cost and growth profile, as illustrated in the following chart.

Looking ahead

Silvercorp’s recent achievements underscore its strategic direction and growth potential. With record first-quarter revenues of US$72 million, a 20% increase year-over-year, the successful completion of the Adventus acquisition and the receipt of regulatory approval to commence construction of the El Domo mine, Silvercorp is well positioned for continued success as a growth-oriented, geographically diversified “green metals” company in the evolving mining landscape.

For more information about Silvercorp, please visit silvercorpmetals.com/welcome.

This is third-party content provided by Silvercorp Metals Inc. (NYSE-A:SVM; TSX:SVM). Please see full disclaimer here.

Join the discussion: Find out what everybody’s saying about this company on the Silvercorp Metals Inc. Bullboard investor discussion forum, and check out the rest of Stockhouse’s stock forums and message boards.

(Top photo of Adventus Mining team member in Ecuador: Adventus Mining)