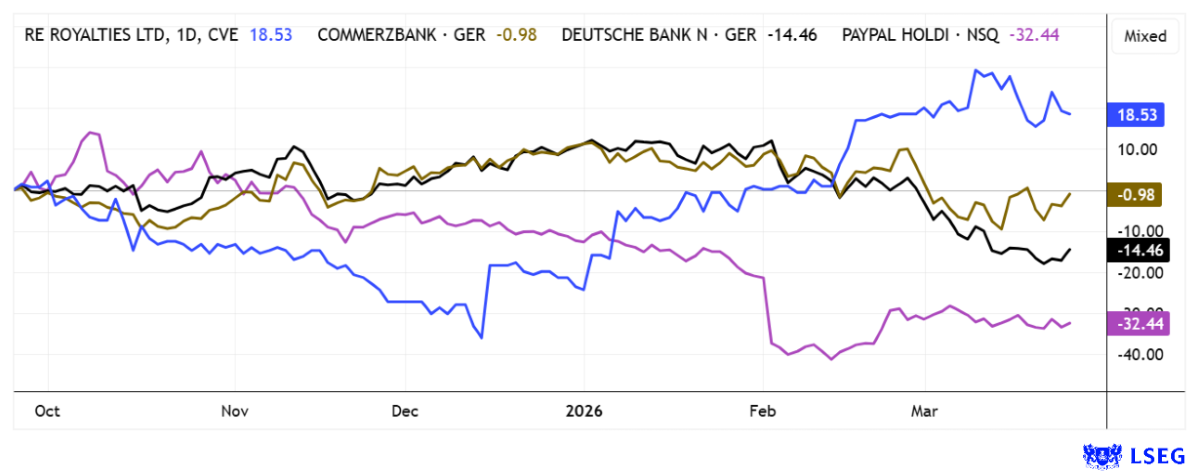

RE Royalties – Double-digit dividend yield meets structural demand boom

RE Royalties’ stock has had a strong year so far. This is no coincidence, as the innovative financial firm pursues a relatively rare financing approach in the energy sector, whereby the company does not act as an operator itself but instead acquires revenue-based royalty interests in renewable energy projects. This royalty principle, familiar from the commodities industry, has been consistently applied to solar, wind, hydro, and storage projects, enabling project developers to secure non-dilutive capital while RE Royalties, in return, receives contractually guaranteed shares of gross revenue for decades. Since the remuneration is based on revenue rather than profits, the business model remains largely protected from increases in operating costs, which significantly enhances cash flow predictability. Typically, loans provided are amortized within a few years, while the subsequent royalty payments often continue for terms of 20 to 25 years or longer.

The portfolio now comprises more than 100 individual investments in North America, South America, and Asia, achieving broad diversification across regions and technologies. The US market is currently developing particularly dynamically, where rising electricity demand driven by digitalization, electromobility, and AI data centers is leading to a structural demand boom. As part of this expansion, the company has, among other things, expanded a financing partnership with a US solar developer, with its investment in an initial project portfolio totaling approximately USD 4.8 million and expected to grow to about USD 9 million in the future. Overall, the company is thus specifically targeting the multi-billion-dollar market for decentralized energy supply in the commercial and industrial segments.

At the same time, RE Royalties has optimized its capital structure and largely repaid previous financing instruments, which improves balance sheet quality and increases financial flexibility. The active management of the portfolio is also evident in the fact that existing investments are regularly adjusted and expanded to include additional royalty components, thereby continuously strengthening the earnings base. With a current market capitalization of approximately CAD 17 million and an expected annual dividend of about CAD 0.04 per share, this results in a double-digit yield in the range of around 10%. The model fills an attractive niche between infrastructure financing and a sustainable income strategy—currently a likely one-of-a-kind structure for long-term yield seekers!

In an interview with IIF host Lyndsay Malchuk, CEO Bernard Tan describes his medium-term business strategy.

Deutsche Bank – A Recession Could Weigh Heavier

Deutsche Bank’s stock has suffered a 30% plunge. Rumors suggest the bank is overweight in the private credit sector, while investment banking revenues are expected to decline. Interest rates are rising, and a surge in personal bankruptcies threatens loan repayments. This isn’t a problem yet, CEO Sewing said in recent comments. The executive does not understand why the stock price has fallen from EUR 34 to 25 in just four weeks. The expected decline in investment banking is a greater concern, as it cannot be offset by increased volumes in sustainable finance. It has since been developed into a clearly measurable core business area, as the Frankfurt-based institution is now one of the largest capital providers for the energy transition in Europe.

Between 2020 and 2024, sustainable financing and investments totaling around EUR 373 billion were realized, with a strategic target of approximately EUR 900 billion by 2030. This target figure illustrates that sustainable finance is no longer primarily reputation-driven, but rather functions as a long-term growth engine in the credit and capital markets business. At the same time, the bank is expanding its so-called transition finance business, which supports capital-intensive industries such as chemicals, steel, and energy in restructuring their production processes. A coming recession would naturally weigh on the loan book. Metzler Equities recently downgraded the Frankfurt-based bank to “Sell” with a price target of EUR 27.40; yesterday, the stock traded at EUR 25.50. The AGM is on May 28, followed by a dividend payout of EUR 1.00. The entry level is becoming increasingly attractive!

Commerzbank – Unicredit’s offer is largely tactical in the current environment

The latest offer from the major Italian bank Unicredit for Commerzbank has set the industry in motion and opened up new opportunities for competitors like Deutsche Bank. CEO Christian Sewing emphasized that his bank is ready to gain market share and capitalize on customer flows, regardless of the outcome of the takeover battle. While Commerzbank CEO Orlopp views the offer as an uncoordinated maneuver with a small premium, Deutsche Bank sees a scenario that could prompt many customers to switch accounts. Unicredit is banking on a twelve-week dialogue to resolve the current stalemate and acquire additional shares. Over 30% of the shares are already in Italian hands, which further heightens the excitement in the German banking market. Whether it is still worth waiting for further price increases is questionable, as the previously strong Commerzbank stock is unlikely to become an outperformer in the current environment. Unicredit shares have also already lost 30% from their peak!

PayPal shares are not far from their all-time low. The financial platform has recently come under significant pressure because revenue and profit growth fell short of investor expectations, and the operating guidance for the coming quarters was more cautious than forecast. Weak transaction volumes in the e-commerce segment, combined with higher investments in new products and compliance costs, have weighed on margins and put sustained downward pressure on the stock price. Additionally, macroeconomic headwinds from higher interest rates, consumer caution, and intensified competition in the payments sector have negatively impacted the valuation.

As a result, some analysts have lowered their price targets; the consensus on the LSEG platform stands at an average of USD 50.70 over a 12-month horizon. However, only 11 out of 44 institutions have a “Buy” rating. Rumors of a potential takeover by major technology conglomerates or financial services providers continue to circulate, but no concrete, binding offers have been made to date. The 2026 P/E ratio has, however, reached the low range of 8.4. With a market capitalization of EUR 36 billion, the 450-million-strong customer base is no longer expensive.

The demands for stability and sustainable business models in the financial sector are high. Today, risk and return must go hand in hand. The current problems at Deutsche Bank illustrate that this is not possible in all phases. RE Royalties, however, demonstrates how structured royalty financing can be combined with renewable energy, predictable returns, and sustainable impact. Commerzbank will likely soon be absorbed into UniCredit, and a buyer will eventually come knocking for PayPal as well.

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as “Relevant Persons”) currently hold or hold shares or other financial instruments of the aforementioned companies and speculate on their price developments. In this respect, they intend to sell or acquire shares or other financial instruments of the companies (hereinafter each referred to as a “Transaction”). Transactions may thereby influence the respective price of the shares or other financial instruments of the Company. In this respect, there is a concrete conflict of interest in the reporting on the companies.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships. For this reason, there is also a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.

Stockhouse does not provide investment advice or recommendations. All investment decisions should be made based on your own research and consultation with a registered investment professional. The issuer is solely responsible for the accuracy of the information contained herein. For full disclaimer information, please click here.