Zijin Mining’s billion-dollar takeover deal for Allied Gold, worth CAD 5.5 billion, is accelerating the wave of consolidation in the African gold sector. Driven by record prices for precious metals, high margins for mining operations, and the strategic desire for long-lasting African assets in viable jurisdictions, investors’ eyes are turning to lucrative properties. Wars, inflation, and exploding national debts make precious metals the ultimate protection. Gold has gained 30% since the beginning of the year, while its little brother, silver, is riding a wave of stockpiling. Most analysts argue that short-term speculation is now giving way to medium-term value stability. Giants such as Barrick Mining with Loulo-Gounkoto, B2Gold with Fekola, and now Zijin via Allied’s Sadiola mine are strategically positioning themselves in the Senegal-Mali Shear Zone (SMSZ), yet Mali’s gold production fell by 23% in 2025. Canadian company Desert Gold Ventures controls the “reserve bank” between these Tier 1 mines with a 440 km² land package in the immediate vicinity, supplemented by scalable resources of currently over 1 million ounces. Today, it is clear that producers are no longer chasing visions, but rather expandable positions along proven zones. This is where Desert Gold’s strength lies, either as a seamless add-on or as a small mine with an NPV of over USD 100 million at current gold prices. What Allied, Barrick, and B2Gold are demonstrating, Desert Gold can quickly replicate on a smaller scale. And if in doubt, the successful explorer will become the logical next takeover candidate in this elite league. The excitement is mounting, and so is the valuation!

This article is disseminated in partnership with Apaton Finance GmbH. It is intended to inform investors and should not be taken as a recommendation or financial advice.

Best informed: Receive reports and updates via e-mail newsletter. Subscribe now for free

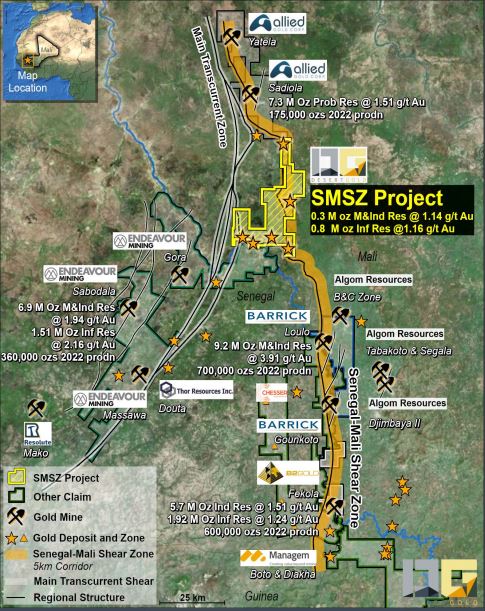

Heartbeat of the Gold Boom: Situated in West Africa’s Most Productive Gold Corridor

The news for Canadian explorer Desert Gold (WKN: A14X09 | ISIN: CA25039N4084 | Ticker symbol: QXR2 | TSX-V: DAU) could not be better at the moment. The successful explorer operates in one of the few regions in the world where geology, history, and infrastructure form an almost ideal intersection: the Senegal-Mali Shear Zone (SMSZ). Over the past decades, this structural corridor has produced deposits containing several million ounces and has attracted well-known mining giants such as Barrick Mining, B2Gold, and Allied Gold. The small Desert Gold controls around 440 km² of contiguous land here today, a strategic asset between active large-scale mines. Crucial from an analytical perspective: the gold-bearing structures are continuous throughout the region. The probability that mineralized trends will continue beyond the license boundaries is high and impressively demonstrated by neighboring mines.

From Explorer to Developer: 2026 Marks an Operational Turning Point

2026 is not a year of announcements, but of implementation. While many junior companies are still modeling resources, Desert Gold is already investing in physical infrastructure. Roads, foundations, water wells, ROM pads, and environmental structures are being prepared at the fully approved Barani East project. At the same time, a modular processing plant is being built, which should be operational by the middle of the year. From an analytical perspective, this approach significantly reduces project risk. Upfront investments shorten construction time, reduce CAPEX peaks, and increase the predictability of the transition to production.

Drilling Results from Mali: Resource Size, Geology, and Upside Inspire

The SMSZ project currently has a resource of approximately 1.1 million ounces of gold with average grades of approximately 1.1–1.2 g/t. However, it is not only the absolute size that is remarkable, but also the composition: these are predominantly near-surface oxide resources with favorable geology. Of the more than 30 gold zones identified, only five have been included in the resource estimate to date. In purely statistical terms, this means there is considerable potential for expansion. Each additional zone that is newly developed and has similar parameters can significantly increase the resource without causing a proportional increase in infrastructure costs – a classic lever on the project value. Based on these assumptions, the pre-feasibility study prepared in 2025 contains significant upside potential.

The PEA in Figures: Profitability with a Buffer

The updated preliminary economic assessment (PEA) provides hard facts. Assuming a gold price of around USD 3,000 per ounce, the project has an internal rate of return (IRR) of approximately 57%. The net present value (NPV 10%) after taxes is over USD 61 million. By comparison, the current market capitalization is significantly lower at CAD 36 million. Sensitivity is particularly relevant: the gold price is currently trading at a further USD 1,500 to 2,000 above the calculation basis, which means that the NPV increases disproportionately, as a large part of the costs are fixed. With gold prices of approximately USD 5,000 and above, the project’s net present value is well over USD 100 million. Metallurgical test work confirms recovery rates of around 68% using pure gravity, and a subsequent CIL step could increase this to over 90%. This implies additional upside without adding new resources. All signs point toward a very promising surge!

Second Growth Axis: Tiegba as a Strategic Option in Côte d’Ivoire

The Tiegba project adds a second, analytically defined value driver. The concession area covers approximately 297 km², of which less than 20% has been systematically explored to date. Historical soil samples yielded values between 50 and over 200 ppb gold along a 4.2 km x 2.1 km anomalous trend. No drilling results are available yet – which makes this asset particularly attractive: high exploration potential with limited risk, as its intrinsic value is already supported by SMSZ.

The Tiegba project lies within the Paleoproterozoic Birimian Terrane, which manifests itself in a northeast-trending volcanic-sedimentary sequence with syn- to late-tectonic granitoids, typical of gold-bearing greenstone belts in West Africa. The local geology of the project bears strong similarities to the Bonikro-Agbaou gold district. Notably, calc-alkaline intrusive structures have been mapped along the eastern and western margins of the permit area. These intrusions are considered favorable host rocks for gold mineralization, particularly along their contacts with highly stressed structural corridors and at the intersection with quartz vein networks. These geological structures are top-priority targets for further exploration.

At the end of January, CEO Jared Scharf presented his strategy in Côte d’Ivoire in an interview with IIF host Lyndsay Malchuck. Click here to watch the video.

Financial Clout: February Financing Secures Next Steps

The CAD 7.18 million financing completed in February strengthens the balance sheet at a critical stage. The high demand and the increase in the round indicate strong institutional interest. Analytically important: the funds are sufficient to cover infrastructure, equipment, and next development steps without having to return to the capital market in the short term. This reduces the risk of dilution precisely at a time when important operational milestones are imminent.

On the sidelines of the recent Mining INDABA conference in Cape Town, CEO Jared Scharf said: “The coffers are now sufficiently full, let’s build a mine!” – and he really means it.

Asymmetric Opportunity: Revaluation Backed by Figures

If one compares the PEA NPV of over USD 60 million with the current stock market valuation, the result is a significant undervaluation – even without resource expansions or higher gold prices. Adding the upside from previously unconsidered zones and the exploration option in Côte d’Ivoire creates an asymmetric opportunity profile. Whether Desert Gold goes into production itself or serves as a takeover target is secondary from an investor’s perspective. In the gold sector, ounces “in the ground” are currently valued at only around USD 50 to 150 per ounce on average by explorers, depending on project status, geology, and location. This is precisely where the valuation discrepancy arises with Desert Gold Ventures, whose SMSZ project already has more than 1.1 million ounces of gold in all resource categories, of which only a fraction has been economically modeled to date. Even with a conservative approach at the lower end of the peer valuation, this implies a project value that is significantly above the current market capitalization. The current PEA significantly reduces the classic explorer risk, as it already demonstrates economic viability, metallurgy, and low capital costs, marking the transition from a pure resource holder to a development project. In an environment of rising gold prices and increasing acquisitions, producers are no longer paying for theory, but for scalable, validated ounces – precisely the category into which Desert Gold is increasingly growing.

Desert Gold (WKN: A14X09 | ISIN: CA25039N4084 | Ticker symbol: QXR2 | TSX-V: DAU)

- PEA for Barani and Gourbassi in Mali shows NPV values in excess of USD 100 million at gold prices of around USD 5,000

- Complementary value driver, Côte d’Ivoire presents itself as an emerging gold producer in West Africa

- Stable political situation and mining-friendly jurisdiction

- Fast approvals, good infrastructure, and dynamic country development

- Underexplored areas offer high exploration potential and strategic opportunities

- Significant interest from Tier 1 producers such as Barrick Mining, Endeavour Mining, Allied Gold, and Perseus Mining

- Location near multi-million ounce deposits such as Agbaou (Allied Gold Corp), Bonikro/Hire (Allied Gold Corp), and Yaouré (Perseus Mining Ltd)

CONCLUSION: GBC sees CAD 0.81 – Dramatically Undervalued with 800% Potential

The gold market has entered a revaluation phase since the beginning of 2026. The recent consolidation in the range of USD 4,800 to 5,200 also came to a quick end. While large mining companies are able to realize dream margins in the current spot market compared to their costs, promising explorers are also attracting increased attention from savvy investors. This is because, with metal prices remaining high, Tier 1 producers can quickly invest their cash flow in strategic mine expansions. According to consensus analyses, major investment houses see gold trading predominantly in the range of USD 4,400 to USD 6,300 per ounce by the end of 2026, with the highest forecast targets from JPMorgan at around USD 6,300/ounce, followed by UBS at around USD 6,200 and Deutsche Bank and Société Générale at USD 6,000 each.

Desert Gold is now in the spotlight with two properties, the prospect of a significant resource expansion, and the start of small-scale production. With approximately 360 million shares after the latest financing, the coffers are full. In early February, Desert Gold reached a new three-year high at CAD 0.11. Over 10 million shares changed hands in some sessions. This also broke the multi-month resistance at CAD 0.08, which had proven quite stubborn since the last financings.

Nevertheless, the market capitalization has only risen to around CAD 36 million in recent days. With a fresh PEA behind it, which in the sensitivity analysis quickly points to a three-digit valuation beyond USD 100 million, the DAU share should continue its positive trend rapidly. The research firm GBC already estimated the fair price per share at CAD 0.81 back in October. Now the path seems clear to new highs, and purely from the perspective of high momentum, the stock could multiply very quickly.

CEO Jared Scharf will present live at 6:30 p.m. CET on February 25, 2026, as part of the 18th International Investment Forum. The update on the latest developments is likely to be exciting. Click here to register

This update follows our initial report 11/21.

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as “Relevant Persons”) currently hold or hold shares or other financial instruments of the aforementioned companies and speculate on their price developments. In this respect, they intend to sell or acquire shares or other financial instruments of the companies (hereinafter each referred to as a “Transaction”). Transactions may thereby influence the respective price of the shares or other financial instruments of the Company.

In this respect, there is a concrete conflict of interest in the reporting on the companies.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is also a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on researchanalyst.com. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.

Source: pixabay.com

Keyfacts

| ISIN: | CA25039N4084 |

| WKN | A14X09 |

| Last Price | 0.10 CAD |

| Number of shares | 360 Million |

| Marketcap. | 36 Million CAD |

| Sector | Gold, Exploration & Development |

| Geogr. focus | Westafrica |

| Flagship project | SMSZ (Mali) / Tiegba (Ivory Coast) |

| Catalysts | mine buildup, takeover speculation |

| Founding year | 2003 |

| CEO | Jared Scharf |

| Homepage | www.desertgold.ca |

Source: Desert Gold, TSX Venture

Media comments

- 23.02.2026 07:40

Beijing’s silver bomb is ticking: Silver Viper Minerals, Infineon, and JinkoSolar in the big winners check - 23.02.2026 07:35

IPO and takeover speculation at Steyr Motors, TeamViewer, and Pure One! Share price set to skyrocket?! - 23.02.2026 07:30

BYD drives demand, while Group Eleven Resources and Hecla Mining are the hidden stars of the commodity year - 23.02.2026 07:25

Gold for your portfolio: Why Barrick Mining, First Majestic Silver, and Kobo Resources are now in the spotlight for investors - 23.02.2026 07:20

New valuation level ahead? How Volatus Aerospace is rising to become a system supplier in the shadow of DroneShield and AgEagle Aerial Systems

Author

André Will-Laudien

Born in Munich, he first studied economics and graduated in business administration at the Ludwig-Maximilians-University in 1995. As he was involved with the stock market at a very early stage, he now has more than 30 years of experience in the capital markets.More about the author

Further analyses

- 23.02.2026

DESERT GOLD – A new gold producer in Africa takes off - 02.02.2026

NEO BATTERY MATERIALS – The Western response to China’s battery monopoly - 26.01.2026

POWER METALLIC MINES – Lion becomes a high-grade concentrate monster - 21.01.2026

Silver Viper Minerals – Leveraging new silver discoveries in Mexico’s core regions - 14.01.2026

ANTIMONY RESOURCES – From exploration project to strategic asset

Stockhouse does not provide investment advice or recommendations. All investment decisions should be made based on your own research and consultation with a registered investment professional. The issuer is solely responsible for the accuracy of the information contained herein.

For full disclaimer information, please click here.