By: Peter Epstein, MBA

How many times have readers heard this story? A very exciting junior miner, with positive cash flow starting soon, cash flow to fund BIG exploration plans…

Then reality sets in, and getting into production is REALLY HARD. A common problem is permitting, which can be delayed or never come through.

Nicola Mining (TSXV: NIM)/(OTCQX: HUSIF) has been in the junior mining game for a long time. It’s managed by an experienced, patient team led by Peter Espig, who became CEO a decade ago.

Mr. Espig has expertise in deal sourcing, financial structuring & corporate turnarounds. He served as VP of the Principal Finance & Securitization & Asia Special Situations Groups for Goldman Sachs Japan. Peter received a B.A. from the Univ. of B.C. and an MBA from Columbia Business School.

The Company is restarting its gold mill near Merritt, B.C., next month. Roughly 15,000 tonnes of gold-bearing ore have arrived from Osisko Development Corp.’s Cariboo gold project. Additional tonnage could follow, but Osisko is not seen as a long-term customer.

The fully-permitted Merritt mill + lined tailings storage facility is unique as it sits on 900 acres of freehold-held land. The mill has highway access and is connected to the grid. B.C.’s hydroelectric power offers some of the greenest, lowest-cost power on the planet.

The site is industrial-zoned and is the only facility in B.C. permitted to accept gold & silver feed from anywhere in the province. When Osisko looked for a home to process its ore, Nicola was the only choice!

Management believes the replacement value of the Mill is up to $100M. It would take many years to design, conduct studies, apply for permits, consult locals, fund, construct/commission, provide site bonding for a tailings facility, and implement a reclamation plan.

These milling partnerships with Osisko and others are not generic toll-milling agreements. Since the mill is literally the only game in town, Nicola enjoys strong negotiating power. It’s reasonable to assume that income from milling partnerships could increase (over time) to a meaningful amount.

Gold/silver concentrate is sold to Ocean Partners UK Limited, a strong partner & shareholder in Nicola. Ocean Partners can help fund acquisitions of stranded deposits and other opportunities in B.C.

It’s also important to recognize the income Nicola’s assets are already generating. The following image shows where this non-milling income is coming from. In total, these sources could generate C$6M+ in cash flow this year.

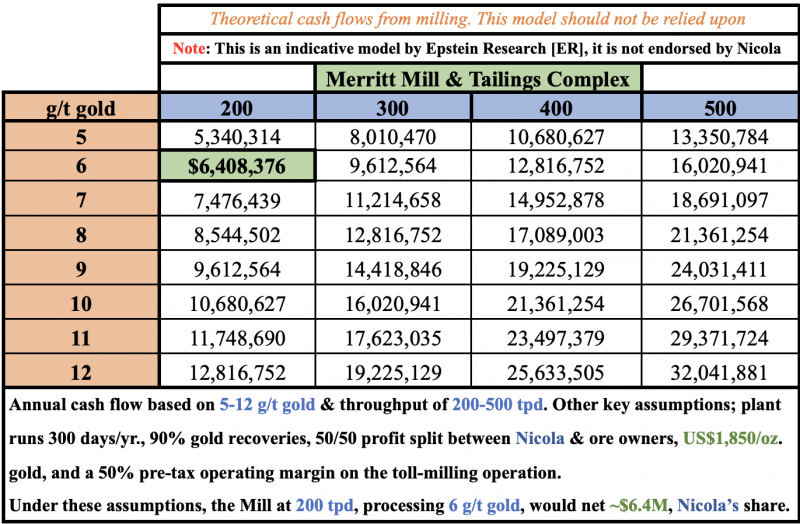

Below is a chart showing a range of milling scenarios; 90% gold recoveries, 300 days/yr. of operation, and a 50/50 split of profits between Nicola & milling partners. Note: {In many instances, Nicola captures > 50% economics}.

Nicola owns 50% [a 75% economic interest] in the Dominion Creek project, which reported grab samples in July 2020 averaging 61.3 g/t Au + 174 g/t Ag.

Dominion has submitted a mine plan for a permit to collect a 10,000-tonne bulk sample, Nicola is optimistic that Dominion will receive the permit this year. Based on surface work, the bulk sample grade is expected to be strong.

The mill operates at 200 tonnes per day (“tpd“), but with modest upgrades and < $2M in capital, it could be expanded to 400-500 tpd in a matter of months.

At 200 tpd, processing mill feed of 6 g/t gold, the annual net cash flow to Nicola (before tax) would be ~C$6.4M. That assumes a 50% operating margin on toll-milling and US$1,850/oz. gold.

CEO Espig is in discussions with multiple entities that could provide high-grade feed for the mill. Depending on grade, ore can be trucked 100s of km. There are a hundred or more stranded deposits within range, but they need mining permits.

Nicola has three main uses for its growing pile of cash, 1) exploring its properties, 2)paying down [~$6M] debt, and 3) buying back shares. I imagine acquisitions are possible as well.

Management deserves a lot of credit for building up this income. Years of hard work, planning, negotiations, ingenuity & attention to detail were required.

After a 2-yr. year process, in November, Nicola received a permit allowing for substantial drilling (up 190 holes) & trenching (up 12 km) over the next five years.

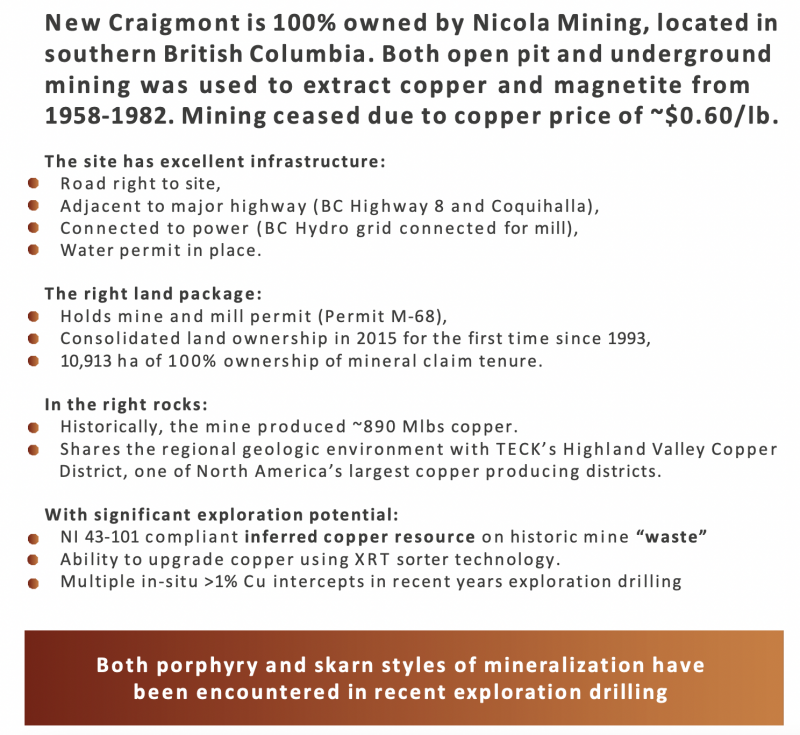

This is critically important as it opens up Nicola’s 100%-owned New Craigmont Project (“NCP“) — much of it for the first time — to extensive, modern exploration & drilling with tremendous operating flexibility.

As exciting as positive cash flow is, potentially growing into the $10’s of millions, management is even more bullish on the blue-sky potential of the NCP.

What’s so great about the NCP? It hosts the past-producing Craigmont Copper mine (1961-1982), the highest grade, primary copper (“Cu“) mine in N. America. In its time, ~1B pound of Cu was produced at an avg. grade of 1.28% Cu.

Exploration over the years has proven that the NCP is a porphyry / high-grade skarn Cu system. The NCP is adjacent to Canada’s largest Cu operation, Teck Resources’ Highland Valley.

For over four decades until 2016, virtually no exploration was done. Seven owners, diverging interests and long periods of low Cu prices resulted in the NCP remaining idle.

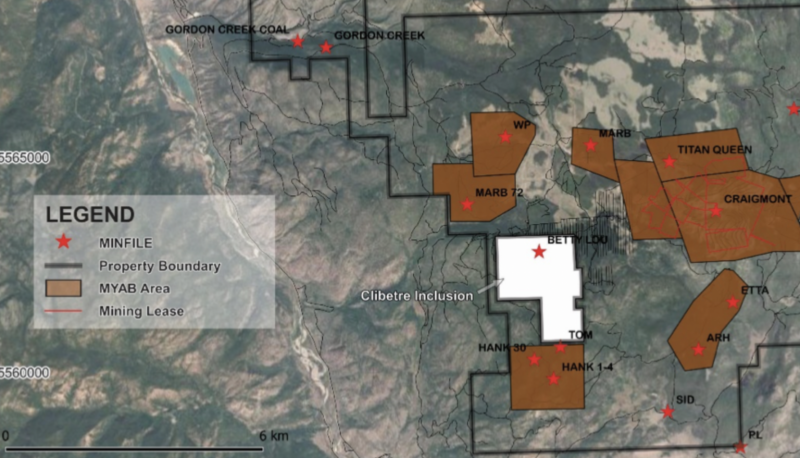

In November 2015, Espig consolidated ownership of the mineral claims & mining leases, which now comprise the NCP. Nicola now owns 10,913 hectares, a significantly larger land package than held by the historic Craigmont Mine.

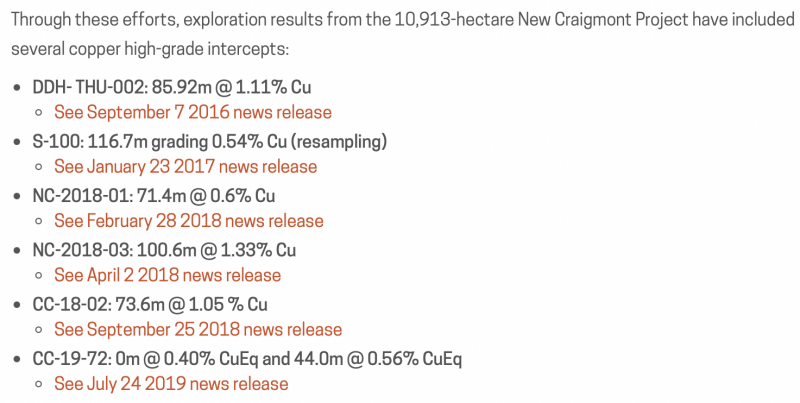

Since 2016 the Company has conducted 10,498 meters of diamond drilling + 1,869 meters of RC drilling. That’s in addition to extensive soil sampling, IP & ground magnetic surveys, property-scale mapping, upgrading Cu grades through the use of an X-Ray transmission sorter, and publishing a NI 43-101 report on historic mine waste terraces.

Below are the best intervals at the NCP; 86 m @ 1.11% Cu, and 101 m @ 1.33% Cu…. these are excellent hits, especially for Canada. Next door, Highland Valley has a remaining mine-life grade (Measured + Indicated + Inferred) of 0.27% Cu.

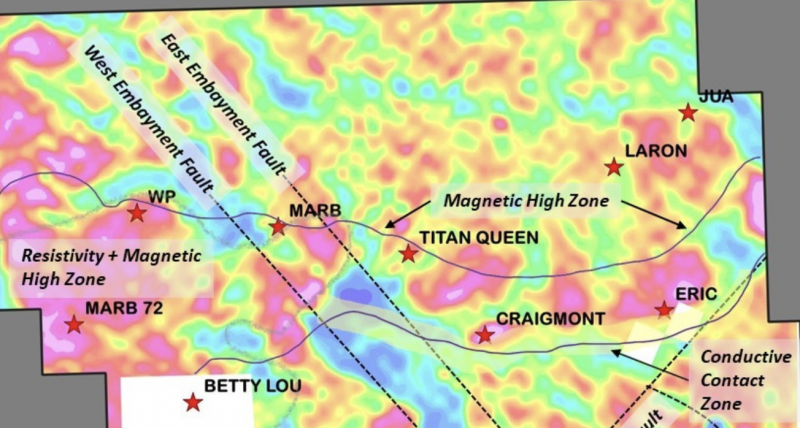

Looking at the property map above, virtually all recent exploration + past mining activities took place around the red star on the right side labelled Craigmont. However, the Company’s technical team has identified a very prospective (from surface & soil samples) target to the east.

The technical team is planning six holes of ~200-250 m length in this area. Then, drilling will move ~6 km west to the MARB 72 & WP targets. Management doesn’t know how many holes might go there but is excited as there are some well-mineralized outcrops.

I’m no geology expert, but this portion of a map {see colourful image below} from a recent ZTWM survey speaks for itself.

The highest grade (past-producing) Cu mine in N. America is near the bottom right (Craigmont). Notice the pink colouring—the more pink, the better, as it depicts higher resistivity & magnetic zones.

Where does one see the most pink? In the MARB 72 & WP zones. Notice the size of the pink blob in and around WP/MARB 72 is larger than that near Craigmont. By no means does this guarantee success, but it’s highly encouraging.

After drilling MARB 72 & WP, the drill rig is expected to move to Titan Queen. Notice the sizable pink zone between Titan Queen & Craigmont.

The beauty of this drill program is that there are essentially no budget or time constraints. With recurring cash flow, the team has the flexibility to step up drilling or slow it down to assess progress. They might settle into one area or keep exploring multiple areas.

The last time the historical Craigmont Mine was in production in 1982, the Cu price hit a low of US$0.544/lb. Today it’s at US$4.06/lb. Back then, average mined grades were twice as high, and water scarcity & climate change? Not really a thing.

The Merritt mill + the blue sky upside from the NCP represent the meat & potatoes of this story, both could be company makers. Imagine the value of the mill if it can demonstrate 90%+ recoveries at a continuous 400-500 tpd.

Another prospective asset is the 100%-owned, fully-permitted Treasure Mountain project. Treasure Mountain hosts high-grade silver in south-central B.C.

Soil samples from 2019 & 2020 returned strong values, including one of 813 g/t Ag + 0.52 g/t Au + 19% zinc & 4.66% Cu. A vein sample came back at 1,300 g/t Ag, 2.59 g/t Au, 1.16% Cu, 27.4% lead & 27.2% zinc.

Treasure Mountain is permitted to mine 60,000 tonnes/yr. and ship that material off the property for processing.

Written by Peter Epstein of Epstein Research [ER] on behalf of Nicola Mining Inc., a Stockhouse Publishing client.