Notable Shifts in the Central Bank Sector

Approximately 1% of global wealth is invested in gold; in numerical terms, this currently amounts to roughly USD 28 trillion. That is not even close to the total amount the US Federal Reserve (FED) owes its bondholders. For over a decade, a new trend has been dominating, with China, India, Poland, and Turkey—as well as numerous other emerging markets—massively expanding their gold reserves while simultaneously reducing their US dollar holdings. Annual purchases by central banks worldwide have remained at record levels of over 1,000 metric tons for several years, underscoring gold’s growing strategic importance in the international monetary system. The major gold holders—the US (8,133 metric tons), Germany (3,352 metric tons), Italy (2,452 metric tons), France (2,437 metric tons), and Switzerland (1,040 metric tons)—have kept their holdings virtually unchanged for many years. China (2,313 metric tons), Russia (2,300 metric tons), India (880 metric tons), Japan (846 metric tons), and Turkey (535 metric tons) have caught up significantly. By far the largest single buyer, with an increase of 102 metric tons, is Poland, where reserves had already reached 580 metric tons by 2025. However, only about 20% of the world’s gold is held by central banks; about 40 to 50% is processed into jewelry, and just under 10% is used in industry. This leaves 15-20% for the investment community—but in this segment, ETFs and derivatives dominate. According to the Bank for International Settlements (BIS), the latter represents a value of USD 1.14 trillion, approximately 2.7 times the world’s annual production. An old saying of unknown origin goes: “Gold is the king of metals and the metal of kings!”

Lahontan Gold: Reactivation of the Santa Fe Mine as a Production Platform

We are focusing on the US “Gold State” of Nevada and on one of its developers, Lahontan Gold. At the heart of the investment thesis is the redevelopment of the historic Santa Fe Mine, located in the middle of the famous Walker Lane Trend. The project is based on a mine that was previously in production, where a total of approximately 359,000 ounces of gold and over 700,000 ounces of silver were extracted via open-pit mining and heap leaching between the late 1980s and the 1990s—at a time when the gold price was below USD 400 per ounce. The current situation is fundamentally different, as both the gold price and the metallurgical and geotechnical capabilities allow for significantly higher economic yields, while estimated production costs stand at approximately USD 1,200 per ounce. This results in a structurally much greater margin leverage, which makes the economic reactivation of a previously operated asset significantly more attractive.

2 Million Ounces Enable an Exploration Program for Many Years

The current resource base comprises approximately 1.95 million ounces of gold equivalent (AuEq) in accordance with NI 43-101, with a significant portion classified in the higher-value “Indicated” category. However, what is crucial is not only the existing resource base but also the strategic ambition to expand it to over three million ounces, thereby enabling the scaling up toward a self-sustaining production operation. This development is supported by existing infrastructure such as water access, power connections, and the use of a historic open-pit mining concept, which reduces both capital requirements and development time. Management, led by CEO Kimberly Ann, plans to submit the mining application in the first quarter of 2027. This is expected to be followed by a very short construction phase of just four to six months, implying a potential start of production as early as the fourth quarter of 2027. This compressed timeline is exceptional compared to typical gold development projects.

IIF host Lyndsay Malchuk delves into the facts in Nevada and interviews CEO and founder Kimberly Ann.

Systematic Upgrading of the Deposit Model

The current exploration phase is important for operators and investors, as it significantly expands the geological model of Santa Fe. Of particular relevance are the drill results from the Calvada area, where a thick oxide mineralization was intersected over 90.8 m grading 0.44 g/t AuEq, including higher-grade intervals of 12.3 m at 1.22 g/t AuEq. These results are significant in that they confirm mineralized continuity below the previous resource boundaries, indicating a deeper and potentially more extensive system than previously modeled. The exploratory momentum is further strengthened by the discovery of the “Slab West” zone, which lies outside the previous resource areas and exhibits significant mineralization signatures in several drill holes, including 35 m at 0.34 g/t and 61 m at 0.26 g/t gold equivalent. This shifts the geological understanding from a clearly defined resource to a potentially larger system that has not yet been fully delineated. The resource base is supplemented by historic heap-leach tailings, with an estimated material volume of approximately 16 million metric tonnes, which could contain up to 200,000 ounces of residual gold. From an economic perspective, these tailings represent an important short-term production and cash flow lever that can be used for major capital expenditures at the mine.

Conclusion: A Significant Valuation Gap with Re-rating Potential

The project’s economic attractiveness is significantly enhanced by the current gold price environment, which is well above the historical assumptions used in earlier economic assessments. While the original PEA was based on a gold price of approximately USD 1,950 per ounce, current market prices are at times well above USD 4,000 per ounce, causing a fundamental shift in the underlying cash flow structures. Based on updated model calculations, the after-tax net present value is approximately USD 472 million with an internal rate of return of about 66.6%, which is exceptionally high for a development project of this scale.

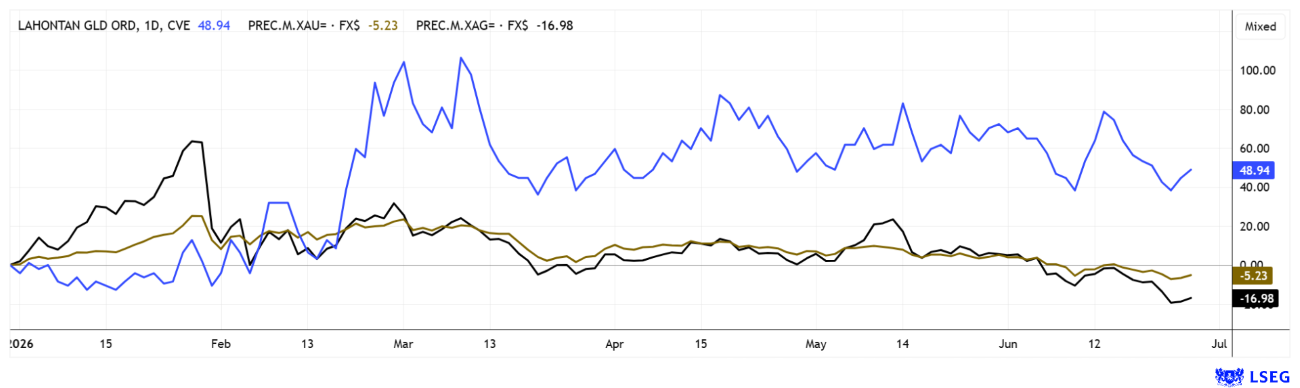

Lahontan Gold had already reached a valuation of over CAD 200 million in March. The project has now progressed further and would warrant a higher valuation, but the current consolidation in the precious metals sector is likely prompting some investors to take profits. However, in the comparison chart with gold and silver, we see a significant outperformance by Lahontan Gold stock.

Following the successful raising of more than CAD 13 million in April, the company now has significantly more firepower for its next phase of growth. The discovery of “Slab West” also shows that the geological potential is clearly far from exhausted. If the company succeeds in integrating the new zones into its next resource models and further boosting profitability, the valuation should quickly follow suit. With a market capitalization of only about CAD 145 million, there remains considerable upside potential here. Risk-conscious investors are taking advantage of the volatile environment with staggered buy limits ranging from CAD 0.32 to CAD 0.40. This could turn out to be a real home run!

Capital markets tend to overreact in all directions. As a result, high-tech and AI enthusiasts are now paying the price for a prolonged bull market, with the first sharp corrections taking hold. Valuations in the defence sector have completely collapsed. Significant profit-taking is also spreading in the precious metals sector after the segment reached historic price highs in January. The gold developer Lahontan Gold is in the eye of the storm, but can look forward to reporting its first production figures!

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as “Relevant Persons”) currently hold or hold shares or other financial instruments of the aforementioned companies and speculate on their price developments. In this respect, they intend to sell or acquire shares or other financial instruments of the companies (hereinafter each referred to as a “Transaction”). Transactions may thereby influence the respective price of the shares or other financial instruments of the Company.

In this respect, there is a concrete conflict of interest in the reporting on the companies.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is also a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.

Stockhouse does not provide investment advice or recommendations. All investment decisions should be made based on your own research and consultation with a registered investment professional. The issuer is solely responsible for the accuracy of the information contained herein. For full disclaimer information, please click here.