DroneShield – NATO Contracts Drive a 100% Revival

The daily “horror” news reports extensively on drone warfare. An important point in this context: The US must spend millions to take Iran’s comparatively cheap Shahed drones out of the sky. The cost ratio of USD 20,000 per Shahed drone to up to USD 3 million per interceptor missile is often cited – crazy! This calls for defense alternatives; the Australian drone defense specialist DroneShield could be a solution! The company is establishing its first production line in the EU to expand its presence in Europe and significantly increase the global manufacturing capacity of its technologies. The catalyst is the rise in European defense spending under “ReArm Europe” and “Readiness 2030,” which is driving rapid growth in demand for sovereign, scalable defense systems. Production will be handled by an established European partner, with the first deliveries scheduled for mid-2026. At the same time, a European supply chain is emerging in a key defense segment. This benefits the West!

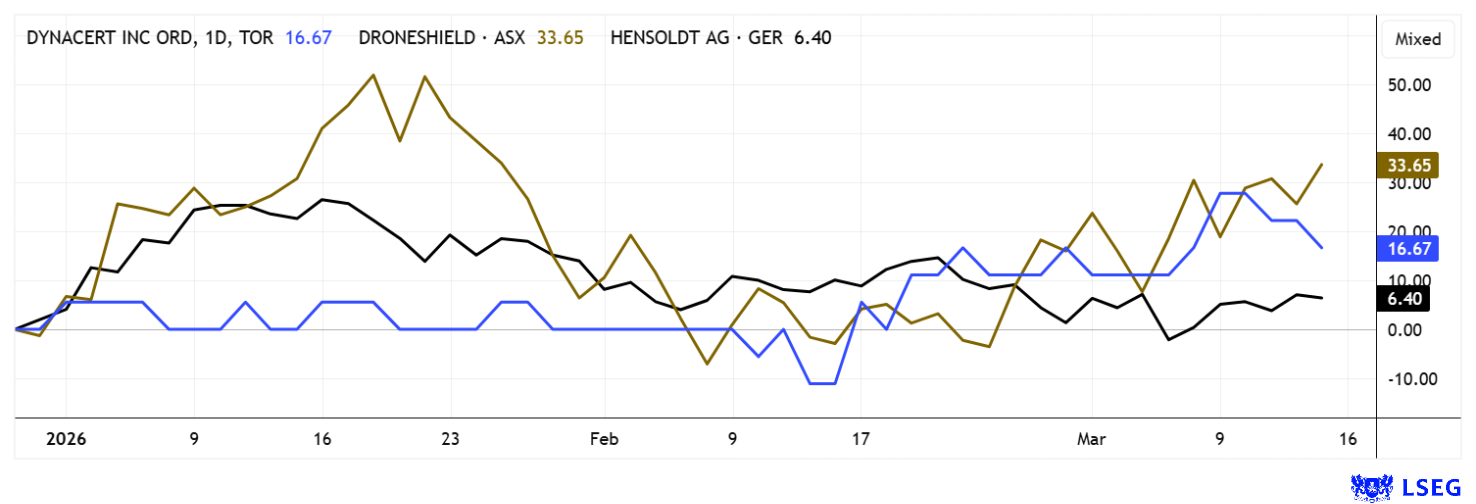

Strategically, the move strengthens the Australian company’s competitive position in European procurement programs and enables faster delivery times for larger quantities. CEO Oleg Vornik sees this as a key to strengthening European autonomy in drone defense. By the end of 2026, DroneShield aims to increase its annual capacity from EUR 430 million to EUR 2.1 billion. This significant scaling responds to the growing global demand from the military, security agencies, and critical infrastructure. Given a market capitalization of EUR 2.35 billion, a substantial increase in revenue would justify the 325% appreciation that has occurred over the past 12 months. With strong operational partners from Europe, this could even be achieved. After an 80% correction through November, the stock has now more than doubled again and is back in the spotlight!

dynaCERT – Diesel-saving technology is now in focus

Other technologies are also in greater demand than ever, because when oil prices skyrocket, fuel savings are needed in every respect! After years of intensive development work, the Canadian company dynaCERT is now at a point where its technological investments could increasingly translate into commercial opportunities. The company is strategically positioning itself as a solution provider for a transitional phase in the global energy sector, during which traditional diesel engines will continue to play a central role for many years to come. Rather than relying exclusively on a future hydrogen infrastructure, dynaCERT’s technology addresses the vast existing fleet of engines in transportation, mining, the oil and gas industry, and stationary power generation. The HydraGEN™ systems developed by the company generate hydrogen directly during operation, thereby optimizing the combustion process, which can reduce both fuel consumption and emissions intensity. Especially in times of sharply rising energy prices, this approach is gaining economic relevance, as efficiency gains for operators can be directly translated into cost savings.

The recent sharp rise in oil prices once again highlights how sensitive the global energy market is to geopolitical tensions and how quickly efficiency solutions come into focus. Technologies that make existing engines more economical could therefore gain importance in many industries in the short term. dynaCERT is responding to this with a clearly sharpened sales strategy and is focusing on markets with particularly high diesel consumption and growing emissions pressure. At the same time, ongoing discussions with fleet operators and industry partners are continuing, even though decision-making processes in traditional industries naturally involve longer cycles. On the production side, the company already considers itself well-prepared to deliver larger quantities as demand rises. A central component of the long-term strategy is also the monetization of emission savings through international CO₂ markets. Using its proprietary data platform HydraLytica, consumption and emission data can be collected and processed for verification purposes, which will form the basis for tradable emission credits in the future. As a result, the business model is potentially evolving beyond the mere sale of hardware toward recurring revenue streams. Strategically, management is currently focusing on those certification pathways where regulatory clarity and robust data enable timely implementation.

From an investor’s perspective, this provides access to a CleanTech company that relies on a pragmatic efficiency solution for existing industrial infrastructure. It is also noteworthy that the current market valuation remains significantly below the cumulative development costs of recent years. With a price target of CAD 0.75, the research firm GBC signals a potential upside that, based on the current level of CAD 0.10 to 0.11, implies a potential increase of approximately sevenfold. Highly interesting from a speculative perspective!

President Bernd Krüper and COO Kevin Unrath explained their sales strategy at the recent 18th International Investment Forum.

Hensoldt – High order intake, but trading sideways for a year

The Hensoldt AG stock price has been remarkably unspectacular, with zero returns over the past 12 months. No wonder, since after an 800% surge since 2022, the price first had to realign with the fundamental situation. However, there is still a strong tendency toward overvaluation here. While revenue has risen cumulatively from just EUR 1.71 to 2.46 billion (+43%) since the start of the war in Ukraine in 2022, profits have risen even more moderately. EBIT rose from EUR 158 million to just EUR 204 million, and net earnings per share for shareholders in 2025 amounted to a mere EUR 0.77. With a 2025 P/E ratio of approximately 100, Hensoldt is thus reaching record levels typically seen only with Tesla or Nvidia. One might assume that the company first had to establish the necessary operational structures to handle the new flood of orders. The outlook from management led by CEO Oliver Dörre is therefore interesting. Revenue is expected to increase by a further 11.7% to EUR 2.75 billion in 2026, and adjusted cash flow is projected to rise to 40% of EBITDA; in 2025, it stood at EUR 347 million. With a market capitalization of over EUR 9 billion, the price-to-cash-flow ratio is thus just under 26. Very low for a thriving defense business!

This does not bother Barclays analysts much; they set the price target at EUR 97.50 but only recommend “Equal Weight.” Jefferies upgrades to “Buy” and expects EUR 90. On the LSEG platform, 6 out of 15 analysts give it a thumbs-up; the mixed 12-month price target totals EUR 88.57 – a EUR 10 premium over the last price. That is not much upside potential for a very highly valued stock. Therefore, there remains a significant risk of a correction!

The capital markets continue to struggle with having to reflect current issues more strongly than long-term prospects. As a result, investors are repeatedly flocking to the arms and defense sector in the hope of capitalizing on further gains. DroneShield is now securing its first NATO contracts, while Hensoldt is already well-established in this sector. dynaCERT has also recently turned a corner; here, energy-saving hydrogen technology appears to be gaining traction amid fossil fuel shortages.

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as “Relevant Persons”) currently hold or hold shares or other financial instruments of the aforementioned companies and speculate on their price developments. In this respect, they intend to sell or acquire shares or other financial instruments of the companies (hereinafter each referred to as a “Transaction”). Transactions may thereby influence the respective price of the shares or other financial instruments of the Company.

In this respect, there is a concrete conflict of interest in the reporting on the companies.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is also a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.

Stockhouse does not provide investment advice or recommendations. All investment decisions should be made based on your own research and consultation with a registered investment professional. The issuer is solely responsible for the accuracy of the information contained herein. For full disclaimer information, please click here.