MustGrow: Improving Yields, Improving Quality

The global agricultural system is at a turning point. Rapid population growth demands more food, while pressure is mounting to make farming methods more ecologically sustainable and to restore depleted soils. Instead of conventional chemicals, innovative pioneers like the Canadian company MustGrow Biologics rely on bio-based systems to activate soil organisms, combat pests naturally, and boost farmland productivity. Farmers’ testimonials report significant yield increases, a milestone for future global food programs.

The agricultural sector remains heavily reliant on chemicals. While the US and Canada together use around 20 million tons of mineral fertilizers annually, the fragility of this dependence is becoming apparent. Supply chains for fertilizers, pesticides, and seeds are vulnerable to geopolitical shocks. The crisis in the Middle East and the temporary closure of the Strait of Hormuz demonstrated how quickly global supply chains can be disrupted. Disruptions there not only drive up energy prices but also undermine the global agricultural supply of essential inputs.

The company’s core product, TerraSante™, a biofertility product registered and organically certified in key US states, including California, works on three levels: it revitalizes soil microbes, promotes stronger root growth, and makes plants more resilient to drought, pests, and nutrient deficiencies. At the same time, synthetic fertilizer and chemical stress on soils is reduced, and the risk of leaching losses decreases significantly. TerraMG™, a pre-registered mustard-derived biocontrol product, goes a step further by specifically combating soil-borne diseases and insect infestations. Field studies document exceptional efficacy and are impressing growers. As mineral fertilizers are increasingly viewed as problematic, MustGrow is gaining importance as a partner for resilient, sustainable, and regionally rooted agriculture. The recent expansion of TerraSante™ in the US is important for the company, as new registrations in Texas, Utah, and Montana bring the number of approved US states to 10. Texas, in particular, with its multi-billion-dollar agricultural markets for potatoes, melons, pecans, and citrus fruits, is considered a strategically attractive growth area for specialty organic products.

MustGrow’s stock has yet to fully price in the upcoming growth in the new licensed territories. For a market capitalization of approximately CAD 35 million, investors gain access to a defined sales territory and an extensive patent portfolio. To finance its current growth, MustGrow is seeking to raise CAD 2 million through a LIFE private placement offering at CAD 0.50 per unit, with each unit including a share purchase warrant exercisable at CAD 0.70.

IIF host Lyndsay Malchuk in conversation with COO Colin Bletsky about the future of biofertilizers and their advantages over conventional methods.

K+S: Downgrades Rain Down after the Rally

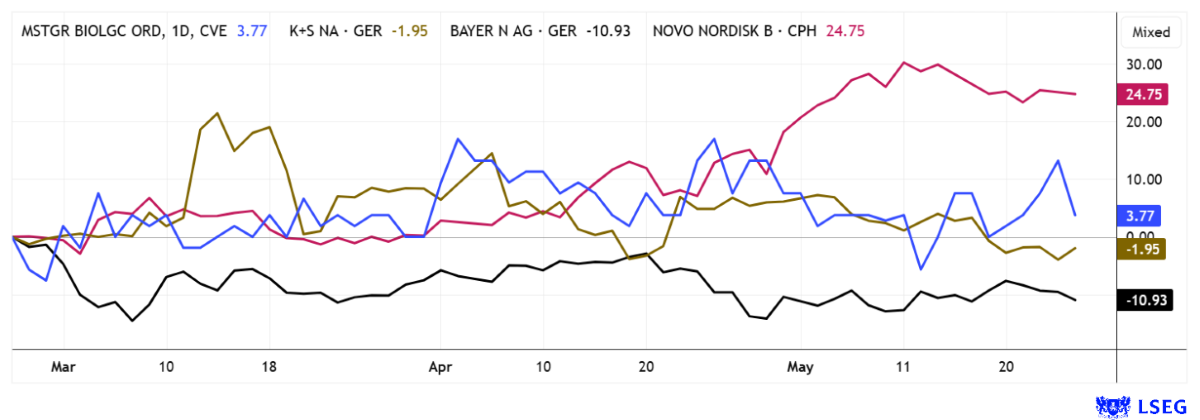

The German fertilizer and salt group K+S is facing increasing valuation pressure following the strong rally triggered by tensions in the Middle East. After the stock hit a three-year high of EUR 18.66 in March, it is now trading around EUR 14.70, while some short sellers are reappearing in the market. Analysts are particularly critical of rising energy and raw material costs, as these may allow for higher selling prices in the short term but could weigh on demand from farmers in the medium term.

UBS remains cautious and continues to recommend selling, despite a slight increase in the price target to EUR 12.00. Potash prices of around USD 450 per ton in Brazil are deemed crucial to reaching the upper end of the company’s forecast, a scenario currently considered rather unlikely. JPMorgan Chase also remains cautious with a “Neutral” rating and a price target of EUR 13.70. They note that the strong quarterly figures have barely triggered any new momentum in the share price, and investors are increasingly questioning the earnings potential for 2026. At least DZ Bank takes a slightly more constructive stance with a “Hold” rating and a price target of EUR 15.25, pointing to stable global fertilizer demand. Deutsche Bank is the most bearish, setting a price target of just EUR 10.50. It even recommends selling. The consensus on the LSEG platform stands at EUR 15.48, but only 4 out of 18 experts would buy more shares. Too bad—a brief hype and it is already over!

Bayer and Novo Nordisk: Analysts Are Becoming More Positive

The situation is different for Bayer and Novo Nordisk; both companies are currently enjoying a strong recovery from their lows. Of course, investors are expecting further gains here, as Bayer was a DAX heavyweight seven years ago with a market value of EUR 150 billion, and Novo Nordisk had staged a 400% rally in its weight-loss drugs by the end of 2024.

At Bayer, relief is primarily driven by hopes of a resolution to the multi-billion-euro glyphosate litigation in the US, while agricultural markets are also stabilizing somewhat. Following the major restructuring program in 2025, the pharmaceutical division can also regain its former strength with new products such as Beyonttra or Lynkuet. With 16 out of 22 “Buy” recommendations, the Leverkusen-based company is well in the running; according to calculations by LSEG experts, the stock is expected to reach EUR 48.50 in 12 months. That is a solid 20% gain!

At Novo Nordisk, sentiment is brightening again following the sometimes heavy profit-taking in the weight-loss and diabetes drug sectors. Market participants continue to see enormous growth potential for drugs like Wegovy and Ozempic, particularly given the consistently high global demand for obesity therapies. Positive analyst comments are increasing, especially since an oral formulation is also in the works. This would likely attract more buyers than the injectable version. Technically, Novo Nordisk must now break through the EUR 38 to EUR 40 range as quickly as possible before the positive momentum turns downward again.

Returns in the Food & Life Sciences sector are still modest. The two industry titans, Bayer and Novo Nordisk, are now going through their third difficult year in a row. While Bayer is bringing new growth drivers on board, Novo Nordisk is facing strong competition in the obesity sector. K+S experienced a brief boom but must now contend with higher input costs. For MustGrow, licensing in three additional US states should lead to noticeable revenue growth.

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as “Relevant Persons”) currently hold or hold shares or other financial instruments of the aforementioned companies and speculate on their price developments. In this respect, they intend to sell or acquire shares or other financial instruments of the companies (hereinafter each referred to as a “Transaction”). Transactions may thereby influence the respective price of the shares or other financial instruments of the Company.

In this respect, there is a concrete conflict of interest in the reporting on the companies.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is also a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.

Stockhouse does not provide investment advice or recommendations. All investment decisions should be made based on your own research and consultation with a registered investment professional. The issuer is solely responsible for the accuracy of the information contained herein. For full disclaimer information, please click here.