- Microsoft (NASDAQ:MSFT) is restructuring Xbox, cutting thousands of jobs and shifting away from a console-first strategy toward maximizing returns from its gaming content and platforms

- Sony (NYSE:SONY) is ending physical game releases in 2028, betting on a fully digital future to improve margins, but facing consumer backlash and potential legal challenges

- Nintendo (OTC Pink:NTDOF) remains the industry’s most stable player, relying on strong franchises like Mario, Zelda, and Pokémon while continuing to support physical media

- For investors, the biggest opportunity is no longer hardware sales but companies that can profit from valuable game IP, digital distribution, subscriptions, and gaming ecosystems

Let’s get physical

The video game industry is undergoing one of its most significant transformations since the transition from physical media to online gaming. For investors, the headlines are no longer centred solely on blockbuster game launches or new console hardware. Instead, the industry is increasingly defined by cost-cutting, platform diversification, digital distribution, artificial intelligence spending, and changing consumer behaviour.

All gaming is responding differently to these challenges, creating dramatically different investment narratives across the gaming sector.

Microsoft’s Xbox reset: Growth at any cost is over

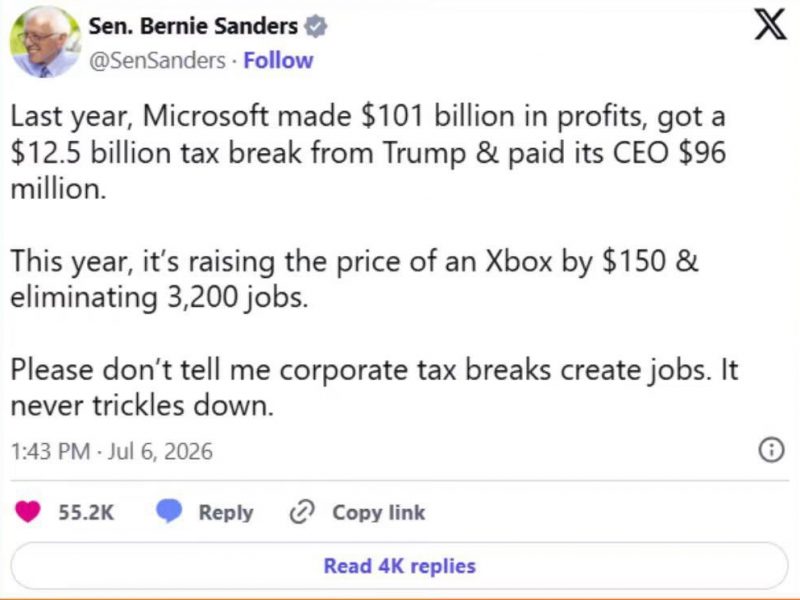

Microsoft’s (NASDAQ:MSFT) July 2026 announcement that it would cut approximately 4,800 jobs—around 2.1 per cent of its global workforce—marks a major strategic shift. Roughly 3,200 of those cuts are tied directly to Xbox and (sorry, XBOX) gaming operations.

The move follows years of aggressive spending. Microsoft invested tens of billions of dollars in gaming acquisitions, including Bethesda and the landmark US$68.7 billion Activision Blizzard purchase. The goal was straightforward: narrow the gap with Sony’s PlayStation and establish Xbox as a dominant gaming ecosystem.

Despite those investments, Xbox has struggled to gain meaningful console market share against PlayStation and Nintendo.

The restructuring appears less about shrinking gaming and more about redefining it. Microsoft is increasingly embracing a platform-agnostic strategy, bringing games to competing platforms rather than relying on hardware exclusivity to sell Xbox consoles.

That reality is reflected in the studio changes announced by Xbox head Asha Sharma. Compulsion Games and Double Fine will become independent studios, while Ninja Theory and Undead Labs will be spun off with greater autonomy around the Senua and State of Decay franchises. Arkane Studios is also reviewing strategic options.

This article is a journalistic opinion piece that has been written based on independent research. It is intended to inform investors and should not be taken as a recommendation or financial advice.

It’s a bluntly obvious message for investors: Microsoft appears focused on extracting returns from gaming assets rather than continuing an unlimited growth-at-all-costs approach.

The timing coincides with soaring AI expenditures across Big Tech. Microsoft has projected approximately US$190 billion in spending during 2026, much of it tied to AI infrastructure and data center expansion. While Azure continues benefiting from strong AI demand, investors have become increasingly focused on whether AI revenue growth can offset mounting capital expenditures.

As Equisights Research CEO Parth Talsania noted, the cuts appear more like portfolio management than a major growth catalyst. Markets now care less about workforce reductions and more about proof that AI monetization is accelerating faster than AI-related costs.

The human cost and growing questions around leadership

Microsoft insists the Xbox layoffs are not directly being replaced by AI, but that is hard to believe.

Amy Coleman, Microsoft’s Chief People Officer, acknowledged AI is fundamentally changing how work gets done, even while stating the eliminated roles are not AI replacements.

Further controversy emerged when Sharma was named to a newly formed Federal Reserve task force focused on jobs, productivity, and the economic impact of AI. Critics have noted that the panel includes business and technology leaders such as Stanford economist Charles Jones and venture capitalist Marc Andreessen but reportedly features no direct representation from workers affected by technological disruption.

For investors, it highlights a growing societal and political debate surrounding AI-driven productivity gains and workforce reductions. While markets often reward efficiency, public perception and regulatory scrutiny can increasingly influence corporate strategy.

What this means for Bethesda and The Elder Scrolls VI

The layoffs have also sparked concerns inside Bethesda Game Studios.

Developers reportedly expressed fears that Microsoft’s restructuring could delay The Elder Scrolls VI, one of the most anticipated games in the industry. Sources have described morale as severely damaged following staff reductions that affected multiple disciplines, including engineering, design, and art.

Investors should pay close attention.

The Elder Scrolls VI is more than just another game. It is one of Microsoft’s largest future content assets. Any substantial delay could affect long-term engagement, subscription growth for Game Pass, and broader Xbox ecosystem value.

Management appears increasingly focused on projects with clear commercial potential, which may improve overall profitability but could also reduce creative experimentation.

MSFT stock lost 0.42 per cent last week and is down 20.37 per cent since the year began, but has risen 0.19 per cent over the past three months.

The bigger problem: Console gaming is slowing

Beyond company-specific issues, the gaming hardware market is experiencing significant pressure.

Recent Circana data showed alarming declines across the industry:

- Xbox Series sales down roughly 70 per cent year over year.

- PlayStation 5 sales down roughly 40 per cent.

- Nintendo Switch family sales down around 10 per cent, even following the release of Switch 2.

The primary reason is simple: consoles are getting more expensive rather than cheaper.

Historically, console prices declined as generations matured. Instead, today’s consoles are becoming more costly due largely to ongoing memory shortages driven by AI infrastructure demand.

The Xbox Series X now costs between $600 and $800, depending on configuration. Sony’s PS5 family has also seen major price increases, while Nintendo launched the Switch 2 at a significantly higher price point than the original Switch.

At the same time, consumers are facing higher spending on housing, food, and other essentials. For many households, a new gaming system has become a discretionary purchase that can easily be postponed.

Sony bets on an all-digital future

While Microsoft is restructuring, Sony (NYSE:SONY) is pursuing a different long-term strategy.

In fact, there was a time when Sony clowned on Microsoft for this behaviour … oh, how things have changed since this video:

The company announced that physical game disc production for new PlayStation releases will end in January 2028. Going forward, new titles will be distributed digitally through the PlayStation Store and retail digital channels.

From a financial perspective, the move makes sense.

Digital sales generate higher margins, eliminate manufacturing costs, reduce retailer influence, and allow Sony to retain greater control over pricing.

However, the strategy has generated significant backlash.

More than 250,000 people have reportedly signed petitions opposing the move, while some players have canceled PlayStation Plus subscriptions in protest.

The concerns go beyond nostalgia.

Physical games allow ownership, resale, lending, and preservation. Digital distribution shifts control almost entirely toward platform holders. The issue is not so much about physical versus digital, since a lot of physical PS discs do not even have a complete game on them, they just serve as keys to activate access to a game. It is not without precedent that people who bought a physical game on a disc lost access to that game due to an expired license.

Sony’s simultaneous decision to begin winding down PlayStation Store support for PS3 and PS Vita has amplified fears about long-term access to purchased content.

It is fitting that I recently dug out this old back issue of Game Players magazine from July 1994 … 32 years ago! Nestled between news about the “new” Street Fighter and Mortal Kombat movies (funnily enough, we are also getting movies based on those game franchises this year), was this small news item about the formation of Sony’s game development team, Sony Computer Entertainment of America, and the first time I had seen a mention of the PlayStation, or PSX as it was known at the time.

Legal risks are emerging

For investors, the most significant issue may not be public relations but legal exposure.

A Dutch consumer group has launched a lawsuit seeking roughly US$457 million in damages, arguing that Sony’s control of digital distribution could inflate game prices once physical alternatives disappear.

Economists have pointed out that physical retail competition historically served as part of Sony’s defence against monopoly-related concerns. Removing physical media could make those arguments harder to sustain.

Even though approximately 85 per cent of PlayStation game sales are already digital, the remaining physical market remains meaningful, particularly for price-sensitive consumers who rely on used-game sales to reduce the effective cost of ownership.

The lawsuit may ultimately fail, but it demonstrates how Sony’s transition introduces new regulatory and legal risk.

Why Sony investors are watching Hiroki Totoki

Adding another layer to the story, Sony CEO Hiroki Totoki sold roughly 225,000 shares shortly after the physical media announcement. I had said that this move was great for investors, but now I am not so sure.

Importantly, there is currently no evidence connecting the transaction to concerns about Sony’s future prospects. Executives regularly sell shares for tax planning, diversification, or personal financial reasons.

Nevertheless, insider sales always attract investor attention, particularly when they occur near major strategic shifts.

The timing has become part of a broader discussion surrounding Sony’s digital-first future.

Speaking of timing, these price hikes have caused PlayStation console sales to fall to their lowest May total in 26 years … a time when no one was buying the original PlayStation anymore because they were busy clearing shelf space for the incoming PlayStation 2.

Sony stock lost 1.47 per cent last week and is down 18.55 per cent since the year began, but has risen 0.95 per cent over the past month.

Nintendo wins in the most boring way possible

Imagine winning a race by not moving. While Microsoft restructures and Sony embraces digital distribution, Nintendo remains comparatively stable.

Nintendo (OTC Pink:NTDOF) continues supporting physical products, and reports suggest additional cartridge sizes may be coming to the Switch 2 ecosystem. That could reduce reliance on controversial game-key cards, which contain licenses rather than full game data.

Nintendo’s software momentum also remains impressive.

According to Famitsu’s latest Japanese boxed charts, Rhythm Heaven Groove debuted with nearly 400,000 physical copies sold in its first week. Tomodachi Life: Living the Dream continues performing strongly as well.

For investors, Nintendo’s greatest strength remains unchanged: its intellectual property. Mario, Zelda, Pokémon, Animal Crossing, and numerous other franchises generate consistent demand regardless of broader industry cycles.

In its home in Japan, Nintendo stock lost 1.43 per cent over the past week and lost 33.65 per cent since the year began.

However, in the U.S., its stock rose 1.86 per cent over the past week, though since the year began, it is down 34.90 per cent.

Other gaming stocks worth watching

Ubisoft (OTC Pink:UBSFF) has struggled for years with execution issues and 2026 has been no different, but Assassin’s Creed Black Flag Resynced appears to be a major success.

The remake reportedly became the largest Steam launch in franchise history, significantly outperforming Assassin’s Creed Shadows and demonstrating the enduring value of Ubisoft’s strongest brands.Ubisoft stock has risen 8.20 per cent last week on Euronext Paris, though it has lost 8.57 per cent year-to-date. Its Wall Street stock was up 3.52 per cent last week and has fallen 14.51 per cent since the year began, but it is up 31.86 over the past three months.

Take-Two Interactive Software (NASDAQ:TTWO)remains one of the most compelling stories in gaming.

Grand Theft Auto VI is expected to become one of the largest entertainment launches ever, potentially generating billions in sales and recurring revenue. Investors continue viewing GTA VI as a major catalyst for the company.

Take Two stock was down 5.89 per cent last week but is up 20.78 per cent over the past three months thanks to the GTA VI hype, though it has lost 5.01 per cent since the year began.

Capcom (OTC Pink:CCOEF) continues executing successfully thanks to careful franchise management and new IP development.

Positive momentum surrounding Pragmata and continued support for Street Fighter VI demonstrate Capcom’s ability to balance fresh ideas with established properties, a combination many publishers struggle to achieve. We’ve recently covered the Japanese gaming publisher’s 13 consecutive years of operating profit growth and nine straight years of record growth.

Capcom stock rose 2.33 per cent last week in Japan and 19.05 per cent on the OTC market. Since the year began, it is down 9.42 per cent back home and down 16.61 per cent on Wall Street.

Welcome to the next level

The gaming industry’s investment story is increasingly shifting away from hardware and toward ecosystems, intellectual property, digital distribution, and profitability.

Microsoft is prioritizing returns after years of acquisition-driven expansion. Sony is attempting to increase margins through an all-digital future, though not without legal and consumer backlash. Nintendo remains the industry’s most stable platform holder, largely because of its unique software portfolio and loyal customer base.

For investors, the most important question is no longer who sells the most consoles.

Instead, it is which companies can best monetize their content libraries, navigate AI-era cost pressures, maintain consumer trust, and adapt to a market where physical ownership, digital distribution, and platform economics are all being redefined simultaneously.

The next phase of gaming may be less about boxes under televisions and more about control—control of content, distribution, ecosystems, and ultimately the customer relationship itself. That battle is now fully underway.

Join the discussion: Find out what the Bullboards are saying about electronic gaming and multimedia, then check out Stockhouse’s stock forums and message boards.