By Chen Lin, chenpicks.com

For thousands of years, silver has been a globally recognized commodity. In China, silver was historically used as a standard form of currency, and the term “bank” in Chinese (银行) literally translates to “silver trading depot.”

Silver is uniquely multipurpose, valued as a financial asset, a decorative metal, and an industrial input. It is a key component in clean energy technologies including solar panels, an industry which is currently experiencing tremendous growth, fueled by environmental awareness, technological advances, and supportive policies. It is one of the best performing commodities in 2024, up more than 30% and currently outpacing gold. In May of this year, the price of silver broke the $32/oz barrier, marking an 11-year high for the coveted metal. Factors include:

- Safe-haven characteristics (hedge against inflation and geopolitical uncertainties).

- Weakness of the U.S. dollar.

- Continued increase in demand for industrial applications, primarily photovoltaics (PV) for the solar panel industry.

Market experts have indicated that this is just the beginning of the silver rally, as there is little technical resistance between $30/oz and $50/oz. I believe silver will break above $50/oz this cycle and settle in the $30-$50/oz range for the long term.

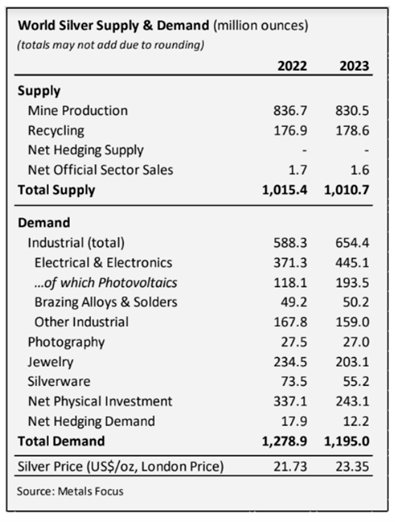

Prior to 2024, the largest silver deficit was recorded in 2022 at 263.5 million ounces. In 2024, the silver market is projected to experience the second-largest deficit on record at 215.3 million ounces. Over the past six years, the solar panel industry, through the use of photovoltaics, has been a consistently notable factor of increased silver demand, using 193.5 million ounces of silver in 2023, a 64% increase from 2022.

Demand for solar panels continues to soar year-over-year due in part to falling prices for this alternative clean energy source and an increase in climate-related energy disruptions.

As the technology and efficiency of solar panels evolve, future models will likely require as much as 150% more silver, further driving up demand. There are numerous factors contributing to the increase of silver in emerging solar panel technology:

- Tunnel oxide passivated contact (TOPCon), for example, is considered the new PV module technology and increases the silver load in solar panels by at least 25%. By the end of 2024, more than 50% of solar panels are expected to be based on TOPCon technology.

- Heterojunction technology (HJT), another development in the solar industry, is also expected to double the silver load in solar panels in future years.

Beyond its current applications and expanding role in the energy transition, silver will also become a critical component in the artificial intelligence (AI) sector, including transportation, nanotechnology, biotechnology, healthcare, consumer wearables, computing, and data centre energy storage.

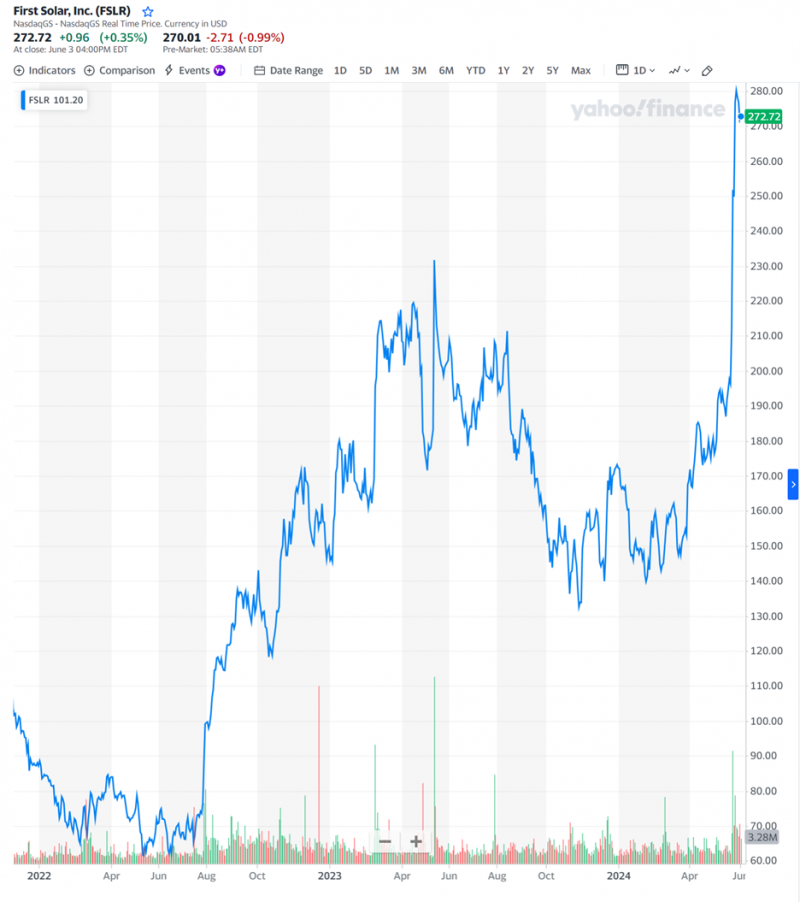

These compounding factors suggest a structural shortage of silver for decades to come. Recently, the Artificial Intelligence (AI) mad dash led to a huge power shortage in the U.S. AI leader Microsoft (NYSE American:MSFT) already turned to solar to be the answer for future AI data centres. Investors are embracing this new idea and solar stocks like First Solar (NYSE American:FSLR) added $10 billion in market valuation after Microsoft’s announcement a few weeks ago. Investors are right about the bright future of solar power, as Microsoft will likely be followed by Google, Meta, Apple and other leading technology companies in the world. I believe same will be replicated in the EU, as well as in Asian countries like China. Currently, Chinese solar panel production capacity is less than 50% utilized. If these factories are running at full capacity in 2025, PV production will double, and the silver supply and demand gap will reach 500 million oz/year, which never happened in human history. Every investor shouldn’t miss this potentially historical run of silver.

At present, silver is mainly a by-product of primary metals, and for production to keep pace with demand, the industry will need to build a number of new primary silver mines. This endeavour hinges upon maintaining elevated silver prices over a prolonged period of time.

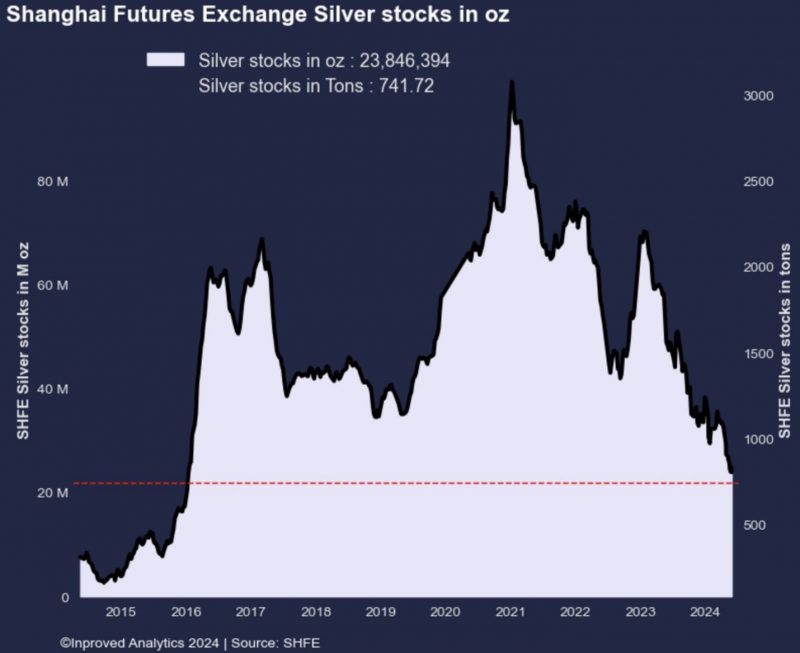

Since my last report, the fundamentals for a growing silver market have continued to improve and the long-term prospects are truly compelling. Even though some silver stocks have rallied in the last six months, they still have considerable room to run. In particular, Chinese investors are piling into silver as they are more informed on the silver shortage led by silver usage in the solar panels. In particular, Shanghai future exchange silver stockpile is about to go to zero before the end of 2024.

While I’ve been investing in silver for some time, I’ve substantially increased my stock holdings, futures and ETFs, as I’m confident in what the future holds for this coveted precious metal.

For those looking to capitalize on this long-term opportunity, I recommend investing in silver production companies that demonstrate significant growth potential. Here are two companies to consider in the current market environment:

- Silvercorp Metals (TSX:SVM; NYSE American:SVM): a Canadian pure-play silver mining company operating several low-cost, long-life mines in China. In its most recent fiscal year, Silvercorp produced 6.2 million ounces of silver at an all-in sustaining cost of $11.38 per ounce, net of by-products. Silver accounted for 58% of total revenue, one of the highest percentages among its peer group of silver miners. The company has US$185 million in cash, no debt, and is actively buying back shares and paying dividends. Silvercorp’s strong balance sheet funds a plethora of growth projects at its operations, and strategic M&A for increased diversification. Mining entrepreneur Dr. Rui Feng is the founder, chairman, and chief executive officer of the company.

- Cerro de Pasco Resources Inc. (CSE:CDPR; OTCPK: GPPRF; FRA: N8HP) (“CDPR”): is a Canadian mining company with several polymetallic mining assets in Peru. CDPR was recently awarded a long-waited easement enabling it to begin development of its Quiulacocha Project. The Project comprises the reprocessing of 75 million tons of tailings extracted from the legendary Cerro de Pasco mine between 1902 and 1992. Historical reports and metallurgical balances obtained by the CDPR show the tailings to contain around 458M ounces of silver equivalent across Ag, Cu, Zn and Pb. In addition, there is evidence of a significant presence of critical metals such as germanium, tellurium, indium and gallium. Mining cost per unit is expected to be the lowest in the industry as the material is on the surface. Studies will assume reprocessing at adjacent processing plants that have current capacity to treat at least 17.5K tons per day. The Quiulacocha Project is one of 6 mining projects on the Peruvian government’s priority list.

This is third-party content provided by Silvercorp Metals Inc. (NYSE-A:SVM; TSX:SVM). Please see full disclaimer here.

Join the discussion: Find out what everybody’s saying about this company on the Silvercorp Metals Inc. Bullboard investor discussion forum, and check out the rest of Stockhouse’s stock forums and message boards.

(Top image of a silver bull: Adobe stock)