Invisible Leaks, Visible Growth: Zefiro’s Formula for Success

The path from hydrogen to methane is not far and can deliver a good return. The Canadian company Zefiro Methane is positioning itself in a structurally growing segment of the environmental and energy sector that has long been underestimated but is now gaining momentum due to regulatory pressure and economic incentives. At its core, the company addresses a serious legacy environmental problem: abandoned or orphaned oil and gas wells that continue to emit methane, thereby having a climate impact many times greater than that of CO₂. The combination of environmental pressure to act and political support appears attractive to investors. This creates a market environment that is less cyclical and more budget-driven, thereby offering high visibility for future revenue. Zefiro succeeds in integrating operational engineering services with financial monetization by converting avoided emissions into tradable CO₂ credits.

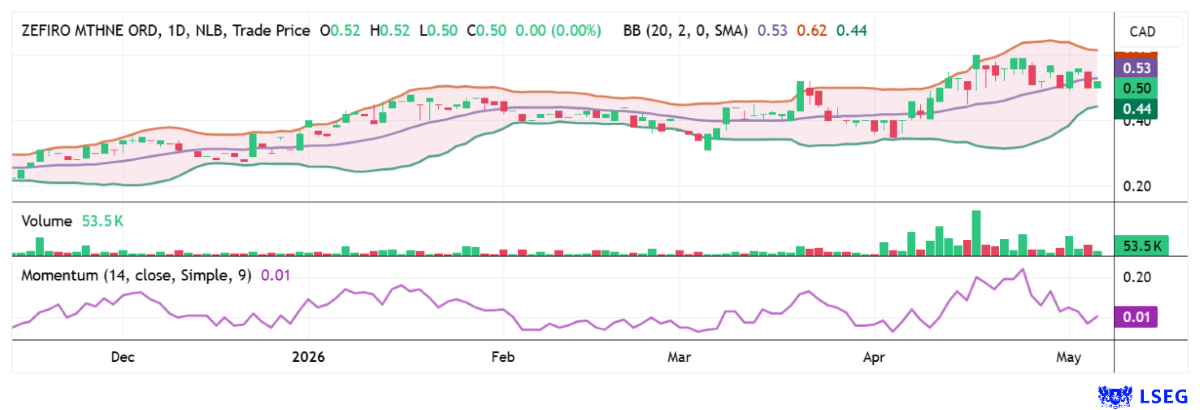

Operationally, Zefiro is transitioning from the build-up to the scaling phase, as evidenced by revenue exceeding USD 22 million over the past two quarters and positive EBITDA of approximately USD 3.8 million. At the same time, the order backlog is growing, driven in part by government projects worth tens of millions of dollars, which lay a solid foundation for the coming quarters. Particularly noteworthy is the improving margin quality: While the traditional plugging business provides stability, methane monitoring is emerging as a high-margin driver with roughly twice the profitability. This is where the trigger lies for investors!

A concrete example is provided by a recently completed measurement program involving 849 wells, which generated approximately USD 850,000 in revenue and is expected to yield an additional USD 450,000 in follow-on revenue. The efficiency of this business is evident in the fact that it is less capital-intensive, carries lower operational risks, and at the same time offers high scalability. This is precisely where the true ingenuity of the business model comes into play. Zefiro earns revenue not only from plugging sources but also from the precise quantification of avoided emissions, a capability essential for monetization via carbon credits.

CEO Catherine Flax will comment on the company’s latest developments at the 19th International Investment Forum (IIF) on May 20! Click here to register

This approach is technologically underpinned by proprietary solutions, such as a specialized measurement system at the wellhead, which enable accurate, reproducible data. This is complemented by patented tools for more efficient wellbore plugging, which not only reduce costs but can also serve as an independent source of revenue. As a result, the company is increasingly shifting from a pure service provider to a technology-driven provider with above-average margin prospects.

What is compelling to investors is the business’s sustainable nature: Zefiro acts not only as a problem-solver but also as a lever with disproportionate impact—in a sense, turning an environmental liability into a tangible asset. Here we see a company operating in a niche but expanding into a viable market through increased scale and innovation. With 75.68 million shares outstanding, Zefiro Methane is currently valued at just CAD 37 million. Given its high ESG relevance and rising environmental awareness, the timing for an investment is excellent. Extremely exciting!

Plug Power or Nel ASA – Who Will Win the Next Race for Returns?

In the hydrogen sector, the choice is becoming increasingly difficult, as most stocks have staged significant catch-up rallies in recent weeks. For instance, the battered Plug Power stock rose from around USD 1.20 to a high of USD 4.58 shortly after the CEO transition from Andy Marsh to Jose Luis Crespo. The subsequent correction cut that gain by 60%, but in the last few trading days, the stock has already climbed back above USD 3.25. Analysts on the LSEG platform have used the company’s reorientation to issue strong upgrades. As a result, the 12-month consensus average now stands at USD 3.02, after many experts had all but written off the stock for a long time. However, after a rise of over 300%, investors should now exercise caution, as the price-to-sales (P/S) ratio is already back at a factor of 5. Price turbulence has always occurred at this level.

Competitor Nel ASA had to quickly regain lost ground after this prominent peer group staged such a rally. In mid-April, the Norwegian company’s recovery also began, rising from EUR 0.18 to 0.33—a 75% gain, no less —who would have thought? Operationally, however, little has changed regarding the difficult order situation. Nevertheless, Nel ASA was able to generate significant attention with its new electrolyzer platform. Business with this innovation is likely now slowly picking up. Following a successful restructuring, at least the cost base has already dropped significantly. Setbacks in this liquid stock down to the EUR 0.27 to EUR 0.30 range appear to be a good entry opportunity from a timing perspective.

ITM Power – Are investors taking their foot off the gas now?

And another shooting star: ITM Power! The share price has quadrupled over the past 12 months. The British manufacturer of hydrogen technology has really made a splash operationally. There are plenty of reasons for this surge. The company has announced several major project wins and new partnerships, including with well-known clients such as the British energy supplier SSE, the Dutch industrial group OCI, and the Australian energy company Fortescue, all of which are using ITM Power’s electrolysis systems for green hydrogen. Nevertheless, demand for green hydrogen remains volatile because it depends heavily on subsidy programs, regulatory frameworks, and the pace of implementation of energy transition projects. In the short term, therefore, a “cool-down phase” could also be on the horizon for the British high-flyer, during which the share price and fundamentals will need to realign. After all, according to LSEG Refinitiv, a price-to-sales multiple of a staggering 22 is now being quoted based on 2026 figures. Such a figure was only observed at Plug Power in 2021, after which the stock fell by 95%. Traders should therefore remain extremely vigilant!

The capital markets are currently delivering a new script every day: First, hope flickers that the conflict in the Middle East is finally coming to an end, then the next escalation casually interrupts. Yet it is precisely this uncertainty that acts as a turbocharger for doubts about fossil fuels—and the fire spreads directly to alternative energies. Hydrogen and methane stocks, in particular, are benefiting significantly from this shift in sentiment. While ITM Power and Zefiro Methane are ambitiously pushing themselves into the spotlight, a much more cautious tone seems appropriate for Plug Power and Nel ASA.

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as “Relevant Persons”) currently hold or hold shares or other financial instruments of the aforementioned companies and speculate on their price developments. In this respect, they intend to sell or acquire shares or other financial instruments of the companies (hereinafter each referred to as a “Transaction”). Transactions may thereby influence the respective price of the shares or other financial instruments of the Company.

In this respect, there is a concrete conflict of interest in the reporting on the companies.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is also a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.

Stockhouse does not provide investment advice or recommendations. All investment decisions should be made based on your own research and consultation with a registered investment professional. The issuer is solely responsible for the accuracy of the information contained herein. For full disclaimer information, please click here.