SAP and Oracle: The Comeback of the Software Giants

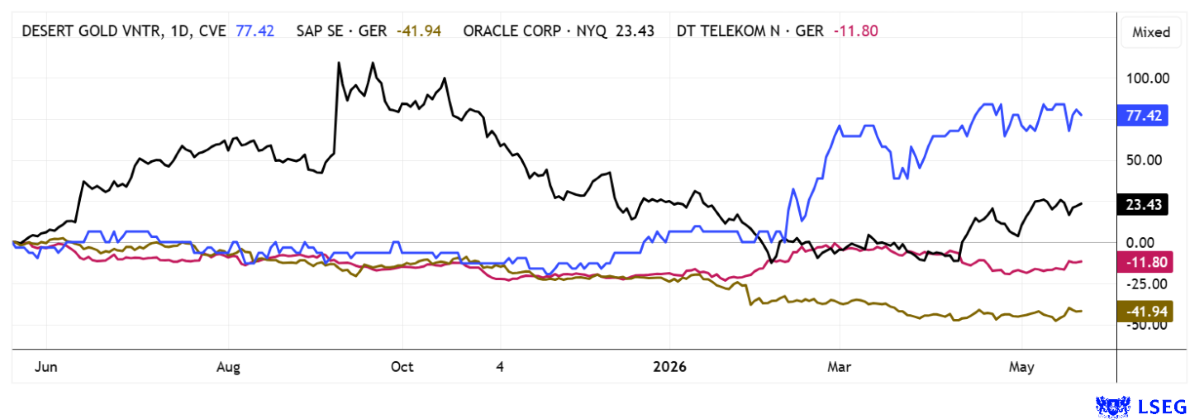

The charts speak for themselves. After months of sell-offs, SAP and Oracle are back on investors’ buy lists. The reason: the quarterly results at the start of the year showed solid growth again, and the outlook for the cloud business was also revised upward. The major software companies are currently experiencing a remarkable renaissance, as it is slowly becoming clear that established platform providers are among the biggest beneficiaries of the global AI and cloud boom. Oracle, in particular, has recently demonstrated impressively how rapidly demand for scalable computing power and enterprise databases is accelerating. With Oracle Cloud Infrastructure growing by around 84% year-over-year, the company is increasingly evolving from a traditional database provider into a serious rival to hyperscalers like Amazon Web Services and Microsoft Azure. Noteworthy is the massive increase in the cloud order backlog of around USD 30 billion, bringing the total order pipeline to more than USD 550 billion—an exceptionally high level of visibility for the coming years.

SAP is also benefiting from this structural shift, as more companies are moving their business-critical processes to the cloud while simultaneously seeking to integrate AI capabilities directly into ERP and data platforms. While many technology stocks have recently suffered from rising interest rates and valuation pressure, Oracle’s and SAP’s prior price declines now appear increasingly excessive, especially given analysts’ expectations of earnings growth of over 30% per year in the coming years. Against this backdrop, an estimated 2027 P/E ratio of 21.3 for SAP on the LSEG platform appears comparatively moderate, especially for a company with a rapidly growing infrastructure business and a strong recurring revenue base. For Oracle, the figure is calculated at 24. The price targets could be exciting. For SAP, the 12-month average target is EUR 217, backed by 26 “Buy” recommendations; for Oracle, there are 31 “Buy” ratings with a price target of USD 248. Technically, both charts are already looking very promising, and now upward momentum is joining the mix. Get in now!

Between Drill Cores and Cash Flow: Desert Gold’s Operational Transformation

Another opportunity for substantial profits is emerging at Desert Gold. While many junior explorers in West Africa are still focused on early-stage drilling programs and capital measures, Desert Gold Ventures is increasingly shifting its focus to the start of mining operations. The company controls a project area of approximately 440 km² along the resource-rich Senegal-Mali Shear Zone (SMSZ), nestled between established mine sites of international producers such as Barrick Mining and B2Gold. In a region known for decades for gold discoveries worth millions, exploration of the area to date appears surprisingly early-stage despite already defined resources, as only a small portion of the entire land package has been systematically investigated. It is precisely this mix of existing resource potential and open-ended expansion potential that currently gives the company its unique momentum.

However, the focus is now less on the mere discovery of new deposits and more on the concrete path toward initial gold production. Preparatory work is underway on the Barani East sub-project, with larger areas already cleared for facilities, storage, and workshops. The modular processing plant, which consists of several container units including a generator and spare parts, has already successfully passed technical acceptance and is currently en route to West Africa. If the current schedule holds, the first gold pour could take place as early as midsummer. A milestone that is likely to fundamentally change the perception of the company. The plant, initially designed for a daily processing capacity of approximately 200 to 240 tons, is intended to be significantly expandable in the future. This modular approach reduces capital requirements in the early phase while simultaneously providing management with operational flexibility in case additional deposits can be integrated faster than expected. Internal economic models already point to robust key figures today. At current gold prices, net present values are reported to be well over USD 150 million, while the current market valuation of just under USD 30 million still appears comparatively moderate. GBC Research has calculated a potential of over 500% and a price target of CAD 0.93. Currently, risk-aware investors can buy in at CAD 0.14 – highly exciting!

IIF host Lyndsay Malchuk in conversation with CEO Jared Scharf about the ongoing mine development in Mali and the opportunities in Côte d’Ivoire.

Deutsche Telekom: Speculation About T-Mobile is Heating up

Things could get really exciting here! Speculation is currently mounting around Deutsche Telekom regarding a possible merger with its US subsidiary T-Mobile US; with a total valuation of EUR 300 billion, this would be one of the largest merger deals on the DAX since Linde-Praxair. Deutsche Telekom currently holds a roughly 53% stake in T-Mobile US, meaning it already controls the group’s most important operational growth driver. The US subsidiary is still valued 20% higher than the parent company—an imbalance considered one of the main reasons for the ongoing strategic deliberations. According to media reports, a holding structure is being examined internally under which both companies could be bundled and subsequently listed on both a European and an American stock exchange. The former Linde-Praxair transaction, in which a neutral holding company was created outside Germany, is seen as a possible model. The merged shares have more than doubled in value since then.

However, investors have so far reacted cautiously because such a structure would be complex and leave numerous questions regarding future valuation, governance, and the structure of influence unanswered. Analysts also point out that management deliberately refrained from making any concrete statements about the reports during the most recent quarterly earnings calls, which tends to increase short-term uncertainty. Accordingly, the Telekom share has recently been somewhat weaker, fluctuating between EUR 27 and 29, after having already surpassed EUR 34 in February. The current rumours appear to be doing the German blue-chip stock more harm than good. Merger or no merger—with a 4% dividend yield and a projected 2027 P/E ratio of 11.8, the “people’s stock” is anything but expensive. Long-term investors are adding to their positions!

The commodities sector remains a hot topic on the stock markets. High demand for real assets, tight supply structures, and expectations of a new wave of takeovers continue to fuel investor enthusiasm. Precious metal stocks, in particular, have risen sharply since mid-2025, but the massive profit jumps and recent acquisition deals in the mining sector suggest the revaluation is likely not yet complete. Desert Gold is a prime example of a stock with high upside potential: lowly valued, with production prospects, and thus a potential candidate for rapid price movements. The situation remains exciting outside the commodities sector as well. Oracle and SAP are showing new upside potential, while in the telecoms sector, the possible merger of Deutsche Telekom and T-Mobile US is coming into focus. Plenty of opportunities for risk-aware investors—a healthy level of diversification helps avoid concentration risks!

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as “Relevant Persons”) currently hold or hold shares or other financial instruments of the aforementioned companies and speculate on their price developments. In this respect, they intend to sell or acquire shares or other financial instruments of the companies (hereinafter each referred to as a “Transaction”). Transactions may thereby influence the respective price of the shares or other financial instruments of the Company.

In this respect, there is a concrete conflict of interest in the reporting on the companies.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is also a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.

Stockhouse does not provide investment advice or recommendations. All investment decisions should be made based on your own research and consultation with a registered investment professional. The issuer is solely responsible for the accuracy of the information contained herein. For full disclaimer information, please click here.