What do Ed Yardeni, Chris Wood, and Thomas Kaplan have in common? In recent months, all three have mentioned a USD 10,000 price target for gold. Mr. Yardeni, founder of Yardeni Research, sees a global debasement of currencies and believes this target could be reached between 2028 and 2029. Chris Wood, Global Head of Equity Strategy at the research firm Jefferies, considers a five-digit valuation for the yellow metal possible within about five years. His reasoning includes a structural bull market, geopolitical uncertainty, and increasing central bank purchases. Finally, Thomas Kaplan of the Electrum Group also regards this target as realistic if gold is rediscovered as a monetary reserve. All of these arguments are understandable, though whether such a scenario will actually materialize remains uncertain. However, many of the factors cited are already evident today. We therefore look beyond the immediate horizon, broadening our view to include tourism and luxury goods – sectors that currently stand somewhat in the shadow of surging gold prices, yet remain no less interesting.

This article is disseminated in partnership with Apaton Finance GmbH. It is intended to inform investors and should not be taken as a recommendation or financial advice.

Gold in Central Africa – DRC Gold Builds Promising Project Portfolio

Those who bet on gold as an asset class can do so in many ways. On the futures market or through certificates, physically, or indeed in gold mines and exploration companies. Depending on preference and risk appetite, various options are available. DRC Gold (CSE:DRC) is the successor to the former exploration company AJN Resources. The company significantly sharpened its positioning in the gold sector at the beginning of 2026 with a strategic realignment. At the heart of the growth strategy is the planned majority stake in the Giro Gold Project within the geologically significant Kilo-Moto greenstone belt. The project area spans nearly 500 sq km and lies about 35 km from the highly productive Kibali Mine, one of Africa’s largest gold production sites.

Historical exploration data already points to significant resource potential, particularly in the Kebigada and Douze Match deposits, where previous drilling confirmed high-grade gold mineralization across substantial intervals. The historical results are now to be systematically validated and, in the medium term, converted into a formal resource estimate in accordance with internationally recognized standards. In addition, DRC Gold holds options on other promising properties, including the Nizi project with the historic King Leopold Mine, whose known ore veins have so far been only partially developed. A structural advantage also arises from the collaboration with the state-owned mining company SOKIMO, which is involved in several projects and facilitates access to promising exploration areas.

In addition to its activities in the Congo, the company is pursuing a second geological focus in Ethiopia, where it holds majority stakes in the Dabel and Okote projects. Okote, in particular, exhibits significant exploration potential due to extensive historical drilling, defined shear zones, and proven mineralization along several kilometers of strike length. Strategically, the company benefits from the long-standing African experience of its CEO, Klaus Eckhof, who has been active in the continent’s commodities sector for decades. Among other things, Eckhof played a key role in the development of Moto Goldmines, whose discoveries later formed the basis of today’s Kibali mine.

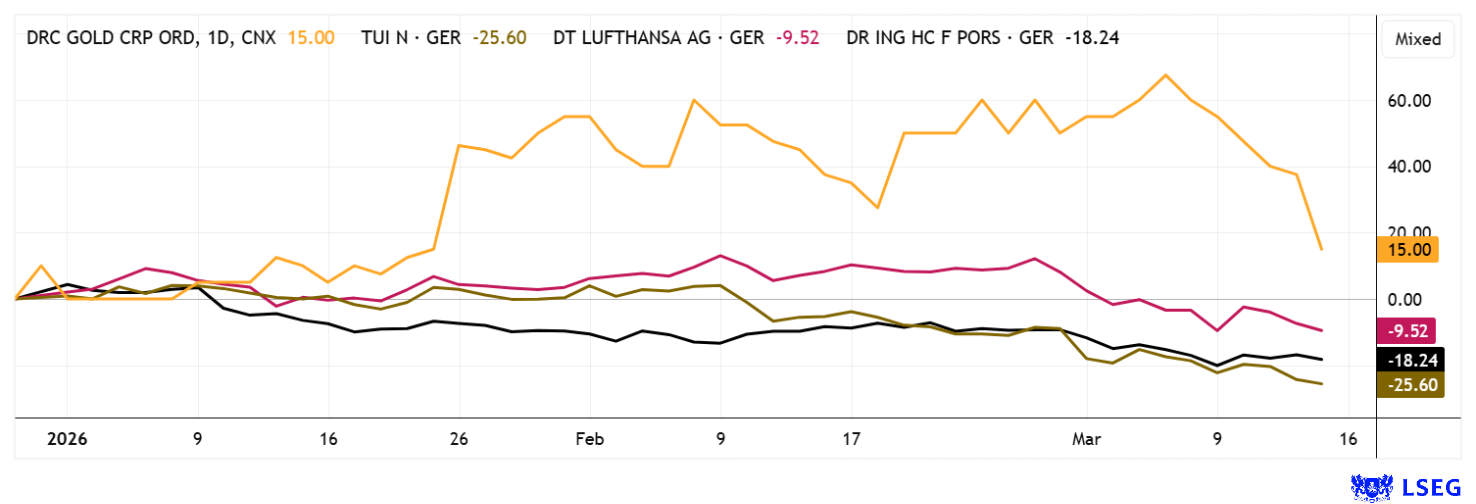

The market is increasingly recognizing this combination of experienced management and promising projects, which is reflected in significant share price momentum since the beginning of the year. Despite this development, the company’s market capitalization remains moderate at around CAD 27 million compared to industry peers. Should the company succeed in confirming and expanding the historical resources at the Giro Project, the company’s fundamental valuation basis could expand significantly as a result. The current market correction in commodities also offers potential entry opportunities for DRC in the range of CAD 0.23 to 0.26.

CEO and founder Klaus Eckhof explained his exploration strategy to IIF host Lyndsay Malchuk.

TUI and Lufthansa – Losers Amid Growing Uncertainty

In the current geopolitical crisis in the Middle East and Ukraine, there are not only war profiteers, such as arms and defense stocks and the energy sector, but also significant losers. TUI and Lufthansa have been hit unusually hard due to flight bans and the loss of an entire holiday region. Investors should nevertheless take a closer look! After all, large multinational travel groups and airlines can generally react flexibly to such negative events. This is because booked trips must be actively rebooked by vacationers, and a claim for a refund is rarely made due to the vacation time already being scheduled. With a little effort in redesigning trips, providers can also exercise their creativity and offer more lucrative deals that may even have higher margins. Another point is the current operational constraints facing all Gulf state airlines, as they cannot change their popular hubs like Abu Dhabi, Dubai, or Doha on short notice. However, since travelers want to take their vacations, they may opt for a European airline. Lufthansa is the market leader there. Investors should therefore pay close attention to CEOs’ statements in the press to determine whether the situation will truly be so costly for tour operators or if there are opportunities for additional profits. TUI and Lufthansa have each lost between 20% and 30%, with P/E ratios for 2026 now at 4.8 and 6.3, respectively. In addition, generous dividend payments are coming soon. The current bet on less negative figures could therefore pay off!

Porsche AG – It Could Always Be Worse

In the fall of 2022, Porsche AG staged a record-breaking IPO in Germany. With an issue price of EUR 82.50, Porsche AG’s calculated market value reached a full EUR 78 billion. Major shareholder Volkswagen had sold 25% of the common shares to the Piech family holding company Porsche International SE for EUR 10 billion at the time, while simultaneously placing EUR 9 billion in preferred shares with interested investors. Those who were savvy used the following three months to sell their shares, as the stock price reached a high of EUR 122.

Last Friday, the price stood at just EUR 37.70, 55% below the IPO price and a full 70% below the all-time high.

From an analytical perspective, a disaster. Unfortunately, however, the outlook for the Zuffenhausen-based company has darkened significantly. In the past fiscal year 2025, revenue fell from EUR 40.1 to just EUR 36.3 billion, while EBITDA collapsed to EUR 413 million, amounting to only a fraction of the EUR 5.6 billion recorded in 2024. A thriving luxury business has turned into a problem child with little prospect of improvement, even in the current year 2026. Porsche speaks of continued “challenging market conditions,” pointing to the weak luxury segment in China, various price wars, and ongoing tariff uncertainties in the US. The war in the Middle East is not even factored into the forecasts. Since sports cars are quite popular there, the conflict is unlikely to have any positive impact on Porsche. To keep investors happy, the dividend is falling by only 56% to EUR 1.01 per preferred share, so the yield remains at 2.7% following the price drop. They do not dare to provide guidance in Stuttgart, and that is for the best! Should Porsche ever be able to generate EUR 5 billion in EBITDA again, it would be a real bargain with a sales/EBITDA ratio of 5.5. Analysts on the LSEG platform expect a 12-month price target of EUR 41.80 – a 25% upside potential for the bold.

Geopolitical conflicts have a very negative impact when they disrupt supply chains or cause people to fear for their lives. The “Gulf States” vacation region currently offers neither a pleasant environment nor safety for people there. As a result, the tourism industry is suffering just as much as luxury consumption in the sports car sector. Gold often proves to be a lifeline in such times, and well-positioned stocks like DRC Gold have an opportunity to thrive here.

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as “Relevant Persons”) currently hold or hold shares or other financial instruments of the aforementioned companies and speculate on their price developments. In this respect, they intend to sell or acquire shares or other financial instruments of the companies (hereinafter each referred to as a “Transaction”). Transactions may thereby influence the respective price of the shares or other financial instruments of the Company.

In this respect, there is a concrete conflict of interest in the reporting on the companies.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is also a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.

Stockhouse does not provide investment advice or recommendations. All investment decisions should be made based on your own research and consultation with a registered investment professional. The issuer is solely responsible for the accuracy of the information contained herein. For full disclaimer information, please click here.