- Long‑life, low‑decline oil sands assets give Canadian Natural Resources (TSX:CNQ) exceptional production stability, supported by diversified operations across Canada, the North Sea, and offshore Côte d’Ivoire

- Strong financial discipline underpins CNQ’s 25‑plus‑year streak of dividend increases, low debt levels, and consistently high free‑cash‑flow generation

- Cost‑efficient, high‑margin production and strategic growth initiatives position CNQ as a resilient, due‑diligence‑worthy candidate for long‑term energy investors

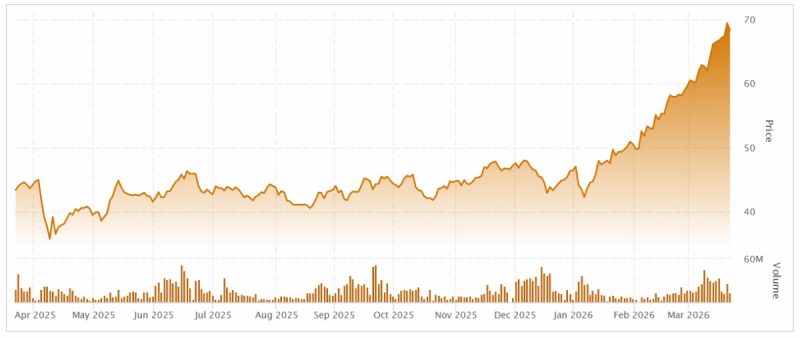

- Canadian Natural Resources stock (TSX:CNQ) opened trading at C$68.66

In a year marked by geopolitical frictions, shifting commodity cycles, and questions about the future of global energy security, investors continue seeking oil and gas companies that combine durability with disciplined capital allocation.

One name that quietly stands out—yet often receives less attention than flashier peers—is Canadian Natural Resources (TSX:CNQ).

While many energy producers rise and fall with market sentiment, CNQ has built a track record of operational consistency, financial strength, and long‑cycle asset security. For investors conducting deeper due diligence into resilient energy names, CNQ offers a compelling blend of stability and upside potential.

A massive, diversified asset base anchored in stability

CNQ is one of the world’s most diversified independent energy producers, operating across Western Canada, the U.K. North Sea, and offshore Africa. The company’s asset mix spans natural gas, light and heavy crude, bitumen, and synthetic crude, enabling multiple revenue levers across commodity cycles.

A cornerstone of CNQ’s business is its long‑life, low‑decline oil sands assets, such as the Horizon Oil Sands facility (264,000 barrels per day SCO capacity) and its major stake in the Athabasca Oil Sands Project, producing roughly 328,000 barrels per day. These world‑class operations provide decades of stable production, a strategic advantage few global producers can match.

Additionally, CNQ maintains strategic exposure to offshore Africa through its operated interests in Côte d’Ivoire, including the Espoir Field and the Baobab Field, located well outside regions currently experiencing heightened instability such as Sudan. The Baobab field lies roughly 3,895–3,961 km (≈2,420–2,461 miles) from Sudan—demonstrating CNQ’s African assets are geographically insulated from recent conflicts.

Operational strength backed by record production

In the most recent reporting periods, CNQ has delivered record production levels, hitting approximately 1.62 million barrels of oil equivalent per day (BOE/d)—an 18.9 per cent year‑over‑year increase driven by strong execution across oil sands, thermal, and conventional operations.

The company’s operating costs remain among the lowest in the sector, with oil sands mining and upgrading costs averaging around C$21 per barrel—a significant competitive advantage during commodity downturns.

This combination of high production output and cost efficiency supports robust free cash flow generation and contributes to CNQ’s reputation as one of the most financially disciplined operators in the industry.

A dividend track record few producers can match

For income‑minded investors, CNQ’s dividend history alone warrants deeper examination. The company has increased its dividend for 25+ consecutive years, an achievement that places it among a select group of global energy “Dividend Aristocrats.”

With recent annualized dividend levels around C$2.35 per share, translating to yields near 5 per cent, CNQ has demonstrated the ability to maintain—and grow—payouts through both bullish and bearish oil cycles.

This durability in shareholder returns is supported by:

- Strong free cash flow

- A low net debt‑to‑EBITDA ratio (around 0.9x)

- Over C$4.3 billion in liquidity entering 2026

CNQ’s measured approach—prioritizing debt reduction, then buybacks, then dividends—gives investors confidence that the payout is backed by sustainable cash flows, not financial engineering.

Strategic growth, not just production for production’s sake

CNQ has pursued growth that complements—not compromises—its financial strength. Recent business moves include the acquisition of Chevron’s Alberta assets, providing high‑margin barrels that contribute immediately to production and earnings. For 2026, CNQ is targeting 1.59 to 1.65 million BOE/d, representing meaningful year‑over‑year growth.

Crucially, this growth comes with continued discipline: a capital budget around C$6.3 billion, aimed at lowering per‑barrel costs and improving long‑term break‑even levels.

The company’s scale in the oil sands gives it a structural cost advantage—CNQ remains profitable even if crude were to fall toward US$40 per barrel, thanks to its low‑decline, long‑life assets.

Why CNQ is worth deeper due diligence

For investors looking beyond short‑term commodity moves, Canadian Natural Resources offers a rare set of qualities:

1. Long‑duration reserves and production stability

Oil sands assets deliver predictable output for decades—a powerful hedge against global supply shocks.

2. Consistently strong capital allocation

A 25‑year streak of dividend increases reflects financial discipline—not just high oil prices.

3. Low‑cost, high‑margin operations

Top‑tier cost structure allows CNQ to outperform peers when oil weakens.

4. Geopolitically stable footprint

Core assets are in Canada, one of the world’s safest jurisdictions, with offshore holdings far from volatile conflict zones.

5. Financial strength and flexibility

Low leverage, ample liquidity, and buyback capacity support shareholder value creation.

Investor’s corner

With its combination of scale, low‑risk assets, financial stability, and reliable long‑term returns, Canadian Natural Resources stands as a compelling candidate for investors seeking durable exposure to the energy sector. It isn’t a speculative bet on commodity spikes or geopolitical turbulence—it’s a company built to weather cycles, deliver cash flow, and compound shareholder value over time.

For investors willing to conduct thorough due diligence, CNQ may prove to be not just another oil producer, but a cornerstone asset in a well‑constructed energy portfolio.

Canadian Natural Resources Ltd. is a senior oil and natural gas production company with operations in Western Canada, the U.K. portion of the North Sea and Offshore Africa.

Canadian Natural Resources stock (TSX:CNQ) opened trading at C$68.66 and has risen more than 55 per cent since this time last year.

Join the discussion: Find out what everybody’s saying about Canadian Natural Resources and check out the rest of Stockhouse’s stock forums and message boards.

Stockhouse does not provide investment advice or recommendations. All investment decisions should be made based on your own research and consultation with a registered investment professional. The issuer is solely responsible for the accuracy of the information contained herein. For full disclaimer information, please click here.