- Goodfood Market Corp. (TSX:FOOD) is shrinking by design, prioritizing survival through cost discipline, margin protection, and cash generation rather than betting on a rebound in meal‑kit demand

- A CFIA licence suspension and sharply lower Q2 2026 sales underscore operational fragility, but new leadership, salary sacrifices, and a simplified operating model signal a serious reset effort

- At a depressed share price, FOOD offers upside only if management can stabilize cash flow and avoid dilution—making it a high‑risk, survival‑optional small‑cap opportunity

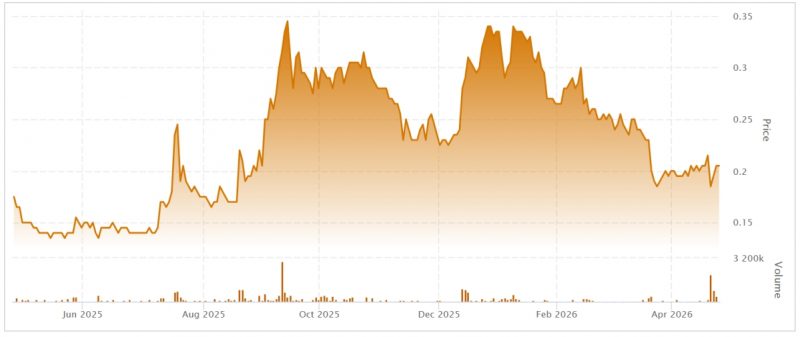

- Goodfood stock (TSX:FOOD) closed trading at $0.19

Goodfood Market Corp. (TSX:FOOD) is attempting a rare and difficult feat: a full operational reset in one of the most unforgiving corners of the food industry—direct‑to‑consumer meal solutions.

Once considered a pandemic‑era growth story, the Montreal‑based company now finds itself repositioned as a deeply discounted small‑cap that investors are watching for signs of survival rather than expansion.

At $0.19 per share, Goodfood’s stock is trading near distressed levels. The company’s market capitalization sits close to C$20 million, reflecting years of declining revenue, customer attrition, and ongoing cash burn. And yet, despite the challenges, FOOD remains 5.4 per cent higher than its level this time last year, even after falling nearly 44 per cent year‑to‑date—suggesting that some investors continue to see optionality in a successful turnaround.

This article is a journalistic opinion piece that has been written based on independent research. It is intended to inform investors and should not be taken as a recommendation or financial advice.

A reset triggered by crisis

In December 2025, Goodfood faced one of its clearest reputational setbacks when the Canadian Food Inspection Agency (CFIA) temporarily suspended the company’s operating licence related to its Montreal production facility. The suspension stemmed from non‑compliance with food safety regulations, an issue that raised immediate concerns among customers and investors alike.

The company responded by emphasizing that no food safety issues were identified. According to Goodfood, the suspension related primarily to procedural and documentation deficiencies, including how customer complaints were reviewed and tracked, rather than contamination or unsafe food handling. While this distinction mattered operationally, the incident nonetheless arrived at a vulnerable time for the business.

The financial impact was immediate.

Goodfood’s Q2 fiscal 2026 results, released in April, reflected both the disruption caused by the CFIA suspension and an already weak demand environment. Net sales fell to C$23 million, representing a 30 per cent year‑over‑year decline. Gross profit dropped to C$7 million, down roughly 12 per cent from the same quarter in 2025, while adjusted EBITDA posted a loss of C$1 million.

The results reinforced the scale of the challenge facing management—yet they also set the baseline for a more intentional reset.

New leadership, new priorities

Rather than attempting to restart growth, Goodfood has elected to rebuild the business around cash discipline and operational simplicity. At the start of 2026, the company appointed a new chief executive officer, alongside a new president and chief operating officer, to lead the restructuring effort. In a symbolic but notable move, senior executives chose to forgo their base salaries for the fiscal year.

Management has positioned this decision as an accountability measure rather than a publicity gesture. On recent earnings calls, executives framed the reset as a long‑term effort to build a model capable of operating profitably at a lower revenue base, without assuming a rebound in meal‑kit demand.

This shift in tone stands in contrast to earlier years, when Goodfood—like many direct‑to‑consumer brands—prioritized customer acquisition over margin protection. Today, the stated focus is markedly different: cost discipline, margin protection, cash generation, and selective investment.

Signs of a narrow path forward

Investors looking for evidence that the strategy could work point to Goodfood’s Q1 fiscal 2026 performance, when the company briefly demonstrated that positive cash flow is possible under tighter operating conditions. That quarter showed positive adjusted EBITDA and more than C$1 million in free cash flow, driven by reduced marketing incentives, higher average order values, and improved gross margins above 40 per cent.

The Q2 setback reversed that progress, but management attributed much of the deterioration to the CFIA disruption. More importantly for the investment case, leadership continues to emphasize unit economics over volume, arguing that a smaller but healthier customer base is preferable to loss‑making growth.

Improving the product, not just the spreadsheet

One of the more unusual elements of Goodfood’s turnaround story lies on the customer side of the equation. While many food brands have faced criticism for raising prices while reducing portion sizes or ingredient quality, Goodfood claims it is pursuing the opposite strategy.

Despite reporting a negative adjusted EBITDA of C$1 million in Q2, management highlighted initiatives to increase portion sizes and source higher‑quality ingredients, aiming to improve customer retention and lifetime value. The logic is straightforward: if growth is no longer the objective, the remaining customers must be worth keeping.

Whether these improvements are sufficient to offset rising input and fulfillment costs remains uncertain. But the strategy underscores a broader reality: Goodfood is no longer trying to be a high‑growth technology‑enabled food company. It is attempting to become a durable, smaller‑scale operator in a difficult category.

The investment angle: Survival optionality

From an investment perspective, Goodfood does not resemble a traditional consumer staples opportunity. It has negative shareholders’ equity, meaningful leverage, and a limited cash runway, with cash and marketable securities hovering around C$9 million as of Q2 fiscal 2026.

As such, the stock’s appeal rests almost entirely on survival optionality. At current prices, the market is not valuing growth, brand strength, or future cash flows—it is assigning a probability to the company’s ability to stabilize without resorting to a highly dilutive capital raise.

If management succeeds in restoring consistent breakeven or modestly positive free cash flow, the equity could re‑rate meaningfully from depressed levels. If not, dilution—or worse—remains a real risk.

Order up!

Goodfood’s ongoing reset places it among a rare group of publicly traded food companies openly acknowledging that less can be more. The company is attempting to trade ambition for discipline, scale for sustainability, and growth narratives for operational realism.

For investors, FOOD is neither a defensive play nor a turnaround guarantee. It is a speculative special situation, best understood as a wager on execution, leadership credibility, and the unforgiving math of food logistics. In a market where many small‑cap consumer stories trade on hope, Goodfood’s strategy offers something less glamorous—but potentially more honest: a fight to survive first, and only then, perhaps, to grow again.

Goodfood stock (TSX:FOOD) closed trading down 9.76 per cent at $0.19.

Join the discussion: Find out what the Bullboards are saying about Goodfood Market and check out Stockhouse’s stock forums and message boards.