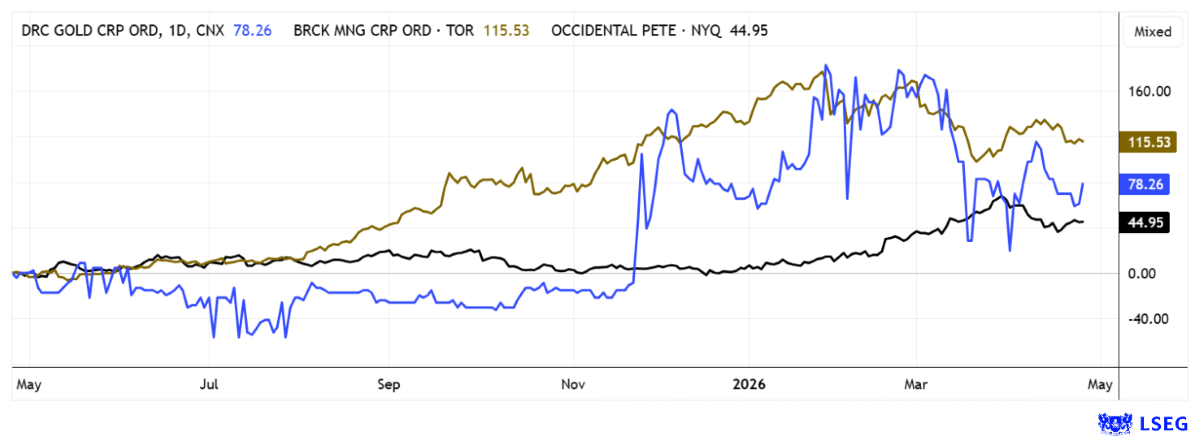

Barrick Mining – Diversification is Key

Barrick Mining’s stock is as steady as a rock. It continues to solidify its status as a global mining giant in 2026, benefiting not only from persistently high gold prices but also from the aggressive expansion of its copper business. The company closed 2025 with impressive revenue of USD 16.96 billion, generating operating cash flow of USD 7.69 billion. The bottom line was free cash flow of USD 3.87 billion, creating a solid foundation for future expansion. For the current year, Barrick plans for gold production to remain virtually unchanged at between 2.90 and 3.25 million ounces, as well as copper production of 190,000 to 220,000 tons; this diversification even absorbs the current high price volatility. In particular, the return of the Loulo-Gounkoto mine in Mali to full operation following the agreement with the government secures another 260,000 to 290,000 ounces of gold annually. It remains to be seen whether the death of the defense minister will further fuel the unrest in Mali. The good news for Barrick is that instability in Africa can be well offset by its core assets in North America and Latin America.

Looking ahead to the end of the decade, the mammoth Reko Diq copper-gold project in Pakistan remains one of the group’s growth drivers. After years of preparation, the first construction phase is now underway. This project of the century is expected to reach full production starting in 2028, aiming for an annual output of up to 500,000 tons of copper plus 300,000 ounces of gold. This could even double Barrick’s copper output in the long term, though an investment of over USD 10 billion must be made first. In Nevada, Fourmile is also coming into focus as a new high-grade project, with investment in development doubled. Barrick is ideally positioned with a geographic spread across three continents, which minimizes risks in volatile times. On the LSEG Refinitiv platform, analysts expect a 12-month average price target of CAD 85, a good 50% above the current price. Fundamentally, Barrick is a solid portfolio component with active gold and copper drivers!

DRC Gold – Well-positioned in East Africa

In addition to the major mining companies, there are always opportunities in the junior sector. The East African company DRC Gold has been unfairly overlooked. This is because its strategic realignment is increasingly taking shape and is acting as a deliberate lever in a market environment characterized by near-record precious metal prices. Gold prices above USD 4,500 per ounce are noticeably shifting institutional investors’ capital allocation. In this context, the company has secured access to two promising concession areas, where it aims to acquire a majority stake of up to 65%.

In particular, the Giro project area spans approximately 497 km² within one of Africa’s most productive greenstone belts. It is located in the immediate vicinity of one of the continent’s highest-producing gold mines, the Kibali Mine, which produces an astonishing 600,000 ounces annually. Such geological analogies are no guarantee in the exploration business, but they are a proven indicator of structural potential that can be systematically developed by experienced teams. In parallel, the historic Nizi area opens up a second growth pillar, whose significance derives less from the past than from the system’s previously untapped depth. Earlier mining activities focused only on a small portion of the known quartz veins, leaving the remaining exploration area largely underdeveloped geologically—a classic scenario for subsequent resource jumps.

Management has internally defined a timeframe of approximately 12 to 18 months in which an initial resource estimate in the range of 2 to 3 million ounces of gold is targeted. And all this at sustainable costs (AISC) of USD 1,100 to USD 1,200 – a dream. Should this goal be achieved, it would create the rare situation of developing two advanced projects in parallel toward production, resulting in economies of scale in infrastructure and financing. The key question now is whether the announced resource data and exploration results can close the implied valuation discount currently reflected in the market capitalization. Strategically noteworthy is also the clear focus on a core region with comparatively short permitting cycles, which could enable projects to transition to the production phase under favorable conditions within 4 to 5 years. A market capitalization of CAD 18 million is a drop in the bucket given the current outlook. Go ahead and grab a few shares at around CAD 0.20; the stock was recently trading at CAD 0.37. Extremely exciting!

IIF host Lyndsay Malchuk in conversation with founder Klaus Eckhof about the unique opportunities for gold in East Africa.

Occidental Petroleum – The Secret Winner of the Oil Crisis

In the wake of geopolitical tensions and persistent supply risks, the US company Occidental Petroleum is emerging for many market observers as one of the quiet beneficiaries of the current oil market turmoil. Since the start of the year, the stock has risen by over 40% at times, significantly outperforming the broader market. The key driver lies in its production structure. With output of around 1.43 million barrels of oil equivalent per day, the company reacts disproportionately sensitively to price movements, which quickly leads to margin expansion when oil prices exceed USD 80 to USD 90 per barrel. Unlike integrated heavyweights such as ExxonMobil or Chevron, earnings momentum is more closely tied to the upstream business, a classic profit multiplier in volatile market phases.

Meanwhile, the balance sheet is looking strong again. Debt has been significantly reduced in recent years, while strategic divestments and operating surpluses have strengthened the equity base. The market continues to closely monitor Warren Buffett’s involvement and that of his holding company, Berkshire Hathaway, which holds approximately 26.7% of the shares and thus serves as a significant anchor of confidence. Analysts see this not only as financial backing but also as an implicit test of the business model’s quality in an increasingly strained energy market.

At the same time, many research firms are urging caution, as the stock’s valuation is now well above the industry average, which could limit its short-term upside potential. On the LSEG Refinitiv platform, 8 analysts still recommend buying, while 15 firms have already downgraded their rating to “Hold” due to the strong performance this year. The bottom line is a company that scores points less through spectacular expansion and more through operational leverage and financial discipline. That is precisely why it can be considered one of the quiet winners in a tense oil market environment. If the oil crisis persists, Occidental remains a solid addition to your portfolio even at this level!

High volatility is testing investors’ nerves. However, that is something that has to be tolerated in this environment. There is also a positive aspect: high-quality stocks are under pressure because some companies are caught in a liquidity trap and forced to sell. This is the moment for bargain hunters. Barrick Mining and DRC Gold appear clearly undervalued. Occidental Petroleum is also trading at an attractive valuation, with a 2026 price-to-earnings (P/E) ratio of just 13.6. Interesting!

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as “Relevant Persons”) currently hold or hold shares or other financial instruments of the aforementioned companies and speculate on their price developments. In this respect, they intend to sell or acquire shares or other financial instruments of the companies (hereinafter each referred to as a “Transaction”). Transactions may thereby influence the respective price of the shares or other financial instruments of the Company.

In this respect, there is a concrete conflict of interest in the reporting on the companies.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is also a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.

Stockhouse does not provide investment advice or recommendations. All investment decisions should be made based on your own research and consultation with a registered investment professional. The issuer is solely responsible for the accuracy of the information contained herein. For full disclaimer information, please click here.