How Zefiro Methane Beats the Winter Cycle

Plugging abandoned and orphaned oil wells is rarely a glamorous business. It is a messy job, its customers are among the world’s largest corporations or even governments, and seasonality can be a major challenge. Between January and March, when frost grips the production regions in the northeastern US, order books traditionally remain thin.

But it is precisely this cyclical pattern that an environmental services provider from Pennsylvania has managed to break. The name Zefiro Methane is worth noting. Investors who placed the company on their watchlist after its 2023 IPO but have since lost sight of it may want to take another closer look.

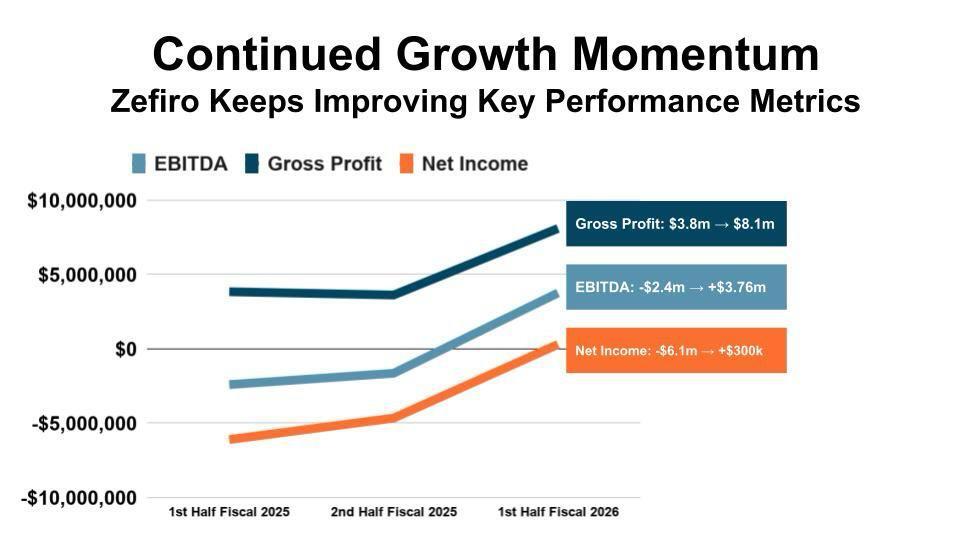

The raw figures for the third quarter of 2026 provide an initial sign. Revenue of approximately USD 11 million represents a 58% increase compared to the same period last year. Gross profit climbed from USD 1 million to USD 2.6 million. And at USD 445,000, adjusted EBITDA is in positive territory for the third consecutive time. This is no flash in the pan; it is a trend.

The Strategic Positioning

What Zefiro Methane CEO Catherine Flax calls a “phase of major transformation” goes far beyond quarterly figures. First, there was the capital increase. Two European institutional investors have invested approximately USD 3.3 million through a private placement. It is the first equity round since the IPO. The funds are being allocated to new assets and working capital.

Then came the acquisition. For USD 4.3 million, the wholly-owned subsidiary, Zefiro Ohio Holdings, acquired five drilling rigs and related equipment from Viking Well Services. Management expects this to generate USD 10 million in additional annual revenue. Luke Plants, Senior Vice President of Corporate Development, puts it this way: “Since we can take on additional contracts in our existing regions while simultaneously expanding into new markets, I expect that we can roughly double our customer base in the exploration and production (E&P) sector as corporate clients.”

This is more than just wishful thinking. With this acquisition, Zefiro is expanding its operational footprint to include five new states: New Jersey, Michigan, Indiana, Illinois, and Iowa. In addition, the company is strengthening its presence in Ohio, Pennsylvania, New York, and West Virginia. The company is now active in 13 of 26 relevant states, leaving significant room for further expansion.

Betting on the State

However, Zefiro Methane’s true unique selling point lies elsewhere. While many competitors are still struggling to even qualify as bidders for public tenders, the company boasts an almost remarkable success rate.

In the state of Ohio, approximately 37% of all funds awarded so far from the first phase of the IIJA Formula Grant Program went to Zefiro. In the core regions, the company received around 25% of all contracts.

This is no coincidence. Its subsidiary, Plants & Goodwin, has been doing nothing but plugging wellbores since 1970. That is 56 years of practical experience. Consequently, the company has the equipment, experienced crews, and, above all, industry contacts to complete projects on time and within budget.

The major driver is the Infrastructure Investment and Jobs Act. The US government has allocated USD 4.7 billion for the decommissioning of abandoned oil and gas wells. If the company maintains a 25% share of the contracts awarded, the volume would exceed USD 1 billion. The estimated number of abandoned wells in the US alone is just under 4 million, and the total addressable market volume is estimated at USD 400–600 billion.

The Activist Investor Has Fallen Silent

Internal disputes are an often-underestimated risk factor for smaller growth companies. Zefiro Methane has also addressed this issue in recent months. At the Annual and Special Meeting of Shareholders on March 20, a dissident shareholder group failed decisively in its attempt to push through its own slate of five directors. Each of the management’s five candidates received approximately 55.3 million votes, while the opposing candidates received only around 21.8 million, a clear vote of confidence given a participation rate of 86.7% of all outstanding shares.

The tiresome power struggle for control of the supervisory board is thus off the table. Management can once again focus on the core business.

A Look at the Technology

In addition to pure drilling operations, Zefiro is establishing a second pillar of business that is expected to improve margins significantly. In April, the company reported its first revenue from a patented tool for expanding wellbore casings, the REED tool. Two commercial deployments for clients in Pennsylvania were successful. Luke Plants explains the significance: “Gas often escapes to the surface due to sustained pressure in the wellbore or through venting flows from the surface casing. In such cases, the cost of fixing the problem can range from several hundred thousand to several million USD—while expanding the well casing with the REED tool costs only a fraction of that amount.”

At the same time, methane monitoring is underway in West Virginia. Measurements were taken from 849 wells. The margin here is roughly twice that of traditional plugging operations. This changes the entire profitability dynamic.

Looking Ahead

The pipeline for the coming quarters is fully loaded. The major contract from Ohio worth USD 19.6 million for methane reduction is now set to begin following initial delays in regulatory approval. Management expects approximately USD 500,000 in revenue from this contract in the current quarter, with the remainder spread out through May 2029. In addition, there are projects such as the continuation of work on 37 production facilities slated for decommissioning in Ohio, a new contract in Richland worth USD 816,000, and the remediation of disposal wells with an expected volume of approximately USD 1.5 million.

In addition, the company generates emission credits over 20 years for each plugged well. These credits can subsequently be sold.

For the nine-month period, Zefiro Methane reported revenue of USD 33.2 million, up from USD 24.4 million in the prior year, an increase of 36%. The stock has recently gained significantly and is currently trading at CAD 0.80.

Zefiro Methane has completed its restructuring and is now scaling up with multiple business units operating in parallel. The balance sheet is becoming cleaner, the customer base broader, and the geographic reach greater. With 56 years of operational experience, a fresh capital cushion, and a resolved shareholder dispute, the foundation is set. Investors looking to capitalize on the multi-billion-dollar remediation market for methane emissions cannot ignore this specialist. The direction is right, and so is the pace.

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as “Relevant Persons”) currently hold or hold shares or other financial instruments of the aforementioned companies and speculate on their price developments. In this respect, they intend to sell or acquire shares or other financial instruments of the companies (hereinafter each referred to as a “Transaction”). Transactions may thereby influence the respective price of the shares or other financial instruments of the Company.

In this respect, there is a concrete conflict of interest in the reporting on the companies.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is also a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.

Stockhouse does not provide investment advice or recommendations. All investment decisions should be made based on your own research and consultation with a registered investment professional. The issuer is solely responsible for the accuracy of the information contained herein. For full disclaimer information, please click here.