Government Programs as a Growth Engine: Tailwind for Zefiro’s Business Model

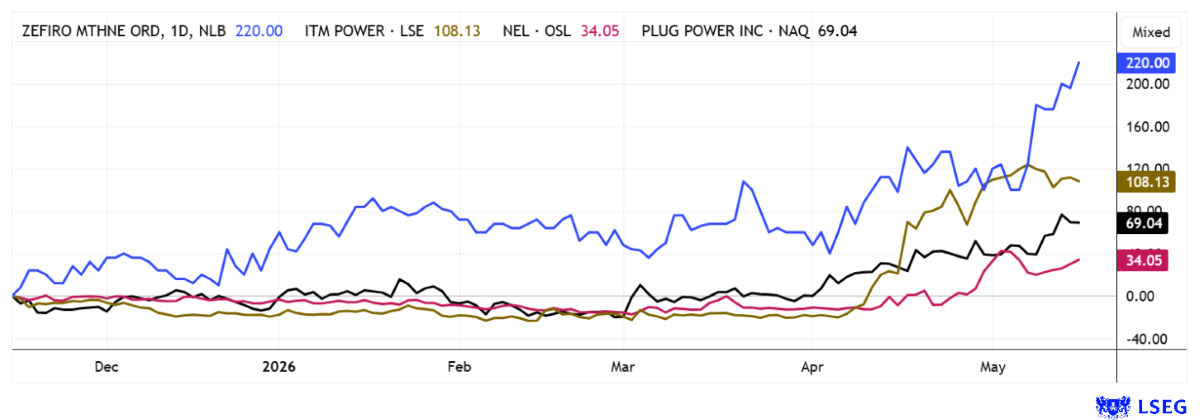

Zefiro Methane was still relatively unknown just three months ago. But in recent weeks, its soaring stock price in particular has caught the attention of investors. The company operates in a structurally growing niche segment of the energy transition characterized by abandoned and orphaned oil and gas wells that continue to emit significant methane emissions even after their production phase has ended. Driven by regulatory programs and government funding, a largely budget-driven demand channel is emerging with high visibility and low cyclicality.

The latest quarterly figures are nothing short of a wake-up call. In Q3 of fiscal year 2026, Zefiro Methane already generated revenue of approximately USD 11.0 million (+58% YoY) while significantly improving its cost structure. Operating expenses fell by more than 14%, while the company achieved positive adjusted EBITDA for the third consecutive quarter. For the nine-month period, revenue now totals USD 33.2 million, accompanied by a significant expansion of the gross margin and a doubling of gross profit to approximately USD 10.7 million. At the same time, there has been a noticeable improvement in the balance sheet. Debt was reduced from USD 12.3 million to USD 8.2 million, marking Zefiro’s transition from the build-up phase to the scaling phase with increasing earnings stability.

A key strategic move is the expansion of operational capacity through the USD 4.3 million acquisition of Viking Well Service equipment. The integration of additional rigs expands the company’s geographic presence to 13 US states. It lays the foundation for estimated additional annual revenue of approximately USD 10 million, strengthening Zefiro’s reach in state tenders as well as its operational throughput capacity. Methane monitoring has now been integrated. In a project in West Virginia, 849 wells were analyzed, generating approximately USD 850,000 in revenue, with expected follow-on revenue of an additional USD 450,000. This segment is less capital-intensive and features significantly higher margins than the traditional plugging business.

Structurally, the business model is increasingly expanding to include the monetization of avoided emissions via CO₂ credits. This creates a long-term, recurring revenue stream in addition to operational services. The long-term outlook is key for the stock market: Zefiro is successfully positioning itself as an integrated environmental and infrastructure service provider with growing scale, improved margins, and increasing government demand. The ability to convert the newly created capacity into sustainable cash flows and long-term contract volumes, therefore, remains crucial for further development. Here, the setup points to a steep upward trajectory!

CEO Catherine Flax will comment on the latest developments tomorrow, Wednesday, May 20, at the 19th International Investment Forum. Click here to register

Plug Power or Nel ASA – Is the rally over in the short term?

It is worth taking another look at the international hydrogen sector. Last week, Plug Power reported its Q1 results. This time, there was no disappointment at all; on the contrary, some details were even surprising. Overall, the company posted the expected losses with an earnings per share (EPS) of USD -0.18. This means the losses were reduced less significantly than hoped. Analysts had previously projected an EPS of USD -0.097 for the company. Meanwhile, revenue rose from USD 133.7 million to USD 163.5 million, significantly exceeding market expectations of USD 139.9 million. Although this news helped drive the stock higher to over USD 4 in the short term, profit-taking resumed yesterday, pushing the price back below USD 3.40. From a technical chart perspective, things are now getting interesting, as the breakout line at around EUR 2.50 or USD 2.95 is drawing closer again. Set a stop at EUR 2.57; this will secure the gains of the past few weeks quite well.

At Nel ASA, short sellers are likely covering their positions right now, as the price closed at EUR 0.313 yesterday, close to the all-time high from May 5. Very striking: Volume is currently approaching 20 million shares per day in Germany alone. The research firm Alpha Value has upgraded its rating to “Buy” and simultaneously set a 12-month price target of NOK 4.12. They are thus the first experts to see a future for Nel stock again. There are also 7 “Neutral” ratings and 6 “Sell” recommendations, though these have not yet been updated following the quarterly results. Therefore, expect upside surprises!

ITM Power – On the ropes, but still on cloud nine

A miracle is currently unfolding with the hydrogen stock ITM Power. We put the stock on our radar last week after the price jumped to a new 3-year high in just 8 weeks. The momentum came from a series of major deals and fresh partnerships with heavyweights like SSE, OCI, and Fortescue, which are betting on electrolysis technology for green hydrogen. It sounds like a smooth ride, but the reality remains volatile for now: demand is hanging by a thread on subsidies, regulation, and the actual pace of the energy transition. Accordingly, this surge could soon be followed by a breather, where valuation and operational performance must realign. Memories of Plug Power from 2021 come to mind—the aftermath was truly painful back then. After all, there have already been a few setbacks. It is worth keeping a close eye on things!

High volatility, but stock prices are trending upward. That has been the conclusion since the end of April. While an agreement in the Middle East would certainly be on investors’ wish list, the current back-and-forth seems to be becoming the prevailing trading pattern. The long-term outlook promises significantly more gains for Zefiro Methane, whereas for hydrogen stocks, stop-loss orders should be placed on the surging charts.

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as “Relevant Persons”) currently hold or hold shares or other financial instruments of the aforementioned companies and speculate on their price developments. In this respect, they intend to sell or acquire shares or other financial instruments of the companies (hereinafter each referred to as a “Transaction”). Transactions may thereby influence the respective price of the shares or other financial instruments of the Company.

In this respect, there is a concrete conflict of interest in the reporting on the companies.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is also a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.

Stockhouse does not provide investment advice or recommendations. All investment decisions should be made based on your own research and consultation with a registered investment professional. The issuer is solely responsible for the accuracy of the information contained herein. For full disclaimer information, please click here.