After a long dry spell for oil, it took a war to bring the necessity of fossil fuels back into focus. But let’s not get carried away. The world markets are flooded with oil, and the US and Canada have built up so much capacity over the last 20 years that Iran’s 4 million barrels of production can easily be offset. “There’s plenty of oil” was the response to the repeated peak oil statements following the work of geologist Marion King Hubbert in 1949. Reserves were supposed to be depleted by 2000, but things turned out differently. Today, researchers estimate reserves to last well over 200 years, making it worthwhile for investors to look at oil stocks. There are many alternatives, including those from Pure Hydrogen and Oklo. The Iran crisis presents another opportunity to restructure portfolios.

This article is disseminated in partnership with Apaton Finance GmbH. It is intended to inform investors and should not be taken as a recommendation or financial advice.

Shell and BP – On the sunny side of the commodity sky

Iran crisis, yes – energy panic no! In its initial statements on the Iran crisis, the EU asserted that the stability of supply for Europe would be guaranteed. This statement is represented by the energy giants Shell and BP, as they are positioning themselves as key players in the new EU programs to secure energy supplies, each with their own strategic priorities. Shell is focusing heavily on expanding its LNG portfolio to meet Europe’s demand for reliable and more climate-friendly natural gas and plans to increase its liquefied natural gas volume by up to 30% by 2030. Shell is pursuing a balanced energy transition with investments in renewable energy and hydrogen, while at the same time maintaining its core fossil fuel production and aiming for moderate emissions reductions. BP is pursuing a somewhat more aggressive transition with a strong expansion of solar and onshore wind projects and is also focusing on bioenergy, while continuing to pursue its LNG business in the fossil fuel sector. The company has more ambitious CO2 reduction targets, aiming for net-zero emissions by 2045, five years ahead of Shell. Both companies are expanding their infrastructure investments in line with European climate targets, modernizing their existing networks and pushing new technologies such as CO2 capture and storage.

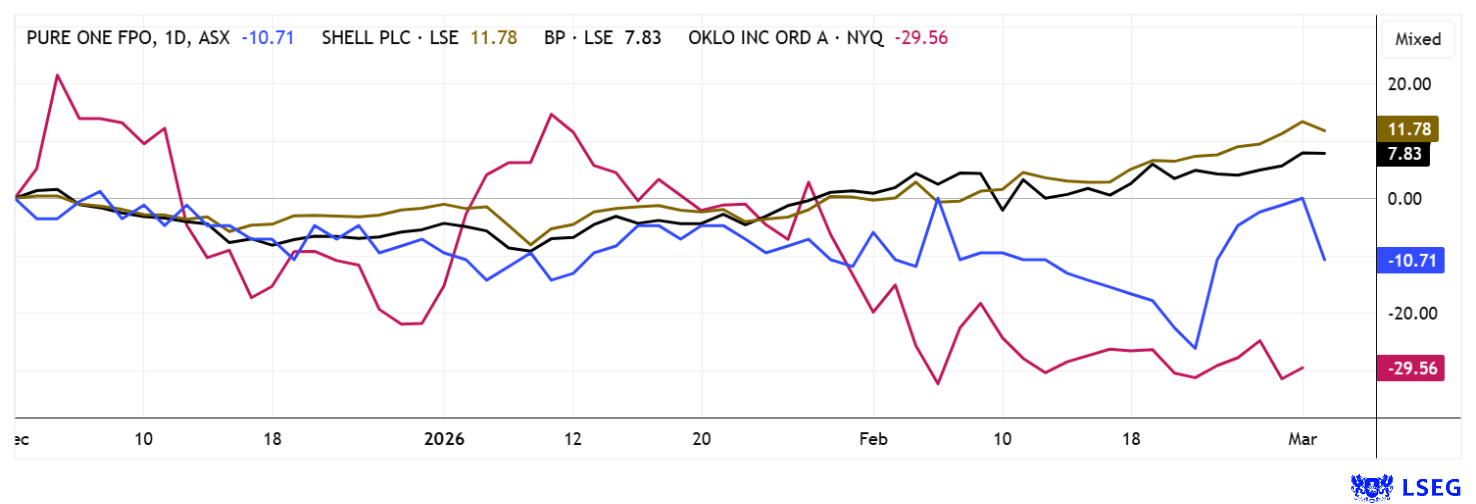

Overall, Shell and BP aim to strengthen Europe’s security of supply by investing in renewable and gas-related technologies, while also ensuring profitability in a more volatile energy market. While Shell is managing its transition with greater financial restraint and conservative emissions targets, BP is actively driving the energy transition with more ambitious change and a greater focus on sustainability and innovation. Investors should keep an eye on these different strategies as well as regulatory risks. On the stock market, investors continue to favor the relatively stable blue chip Shell. Following a minor correction, the share price is trading just under 5% below its all-time high of around 37.30, which was reached during the turbulent Monday morning session. BP is experiencing a different situation. With only a moderate increase to EUR 6.05, the stock has gained at least 12% on a 12-month basis. However, it is still almost 50% off its all-time highs. Despite all the cautious analyst comments on the recently increased levels, they offer their shareholders a stable dividend of 3.5 to 5.5% and are trading at a P/E ratio of 12 to 14 for 2026. In the current environment, it is a solid rock in turbulent waters.

Pure One – Revaluation potential through unbundling and focus

The Australian Pure One Corporation (ISIN: AU0000442865) operates in an energy market that is increasingly characterized by a conflict between politically driven decarbonization and real economic security of supply. On Australia’s east coast in particular, there are growing signs of structural gas shortages from 2028 onwards, as declining production volumes from established fields and the accelerated phase-out of coal are increasing demand for flexible gas capacities. Gas is thus effectively evolving from a transitional technology to a strategic anchor of stability for power grids and energy-intensive industries. In this environment, companies with secure resources and reliable access to infrastructure are gaining significant strategic value.

Pure One, through its majority stake in Eastern Gas, owns promising production rights in the Cooper Basin and is thus addressing precisely this supply gap. The Windorah project has resource profiles that are comparable to those of competitors that are already significantly higher valued, but have not yet been adequately reflected on the capital market within the group. With the now completed IPO listing of Eastern Gas on the Australian Securities Exchange (ASX), this value is becoming transparent for the first time. The accompanying placement met with lively investor interest of over AUD 5 million and was thus oversubscribed. This underscores the attractiveness of a focused gas pure play in the current market environment. Pure One remains the majority shareholder and thus continues to participate substantially in the operational development, while the spin-off enables a clearer valuation structure.

Strategically, management is using the IPO to free up capital for the further development of gas projects and, at the same time, to sharpen the group structure. The funds can be reinvested in a targeted manner in the core business, which focuses on emission-free mobility and energy solutions. Following the renaming of Pure Hydrogen to Pure One, the company is pursuing a technology-neutral approach that encompasses battery electric vehicles, fuel cell drives, swappable battery systems, and refueling and charging infrastructure. The portfolio is complemented by hydrogen generators for decentralized energy supply, which can be used both as a backup solution and as a primary power source, for example for energy-intensive data centers. With expected annual sales of around AUD 42 million, the current market capitalization of around AUD 30 million represents a significant operating foundation. This results in a valuation ratio that appears moderate compared to industry, especially since the value of the gas stake becomes more clearly quantifiable due to the separate listing. All of the above parameters and improved capital allocation argue in favor of a revaluation of the stock. Research firm MST Access values Pure One’s stake in Eastern Gas at AUD 37 million – more than the entire market capitalization of Pure One itself. Given this discrepancy, the price is therefore unlikely to remain at AUD 0.075 for long, so investors may want to stock up!

Oklo – SMR pioneer caught between AI boom and regulation

There is also a nuclear answer to tense fossil fuel markets. Oklo Inc. is positioning itself in the SMR market as a technologically differentiated developer with a focus on compact, sodium-cooled fast reactors. With the Aurora Powerhouse, Oklo addresses power ranges of around 15–50 MW and specifically targets industrial applications and energy-intensive data centers. Unlike providers such as NuScale Power or Rolls-Royce SMR, the company does not rely on classic light water technology, but on an advanced reactor design with higher fuel efficiency, albeit with increased regulatory requirements.

The strategic core of the equity story is the rapidly growing demand for electricity from AI infrastructure, which requires base-load-capable, low-CO₂ energy sources. Oklo is positioning itself here as a potential supplier for hyperscalers and data-intensive industries. In addition to Aurora, the company is pursuing further micro-reactor concepts with “Pluto” and is building up additional expertise in the field of fuel and isotope cycles through Atomic Alchemy. In a competitive comparison, Oklo is one of the more ambitious SMR players in terms of technology, but, like most of the industry, is still awaiting broad commercialization. The realization of the first reference project in Idaho, which is to serve as proof of concept for scaling and financing, remains crucial. The current valuation of just under USD 11 billion already reflects significant growth expectations, which means that the opportunity-risk profile is heavily dependent on regulatory progress and operational implementation. Interesting during corrections – currently rather overpriced!

With the sudden unrest in the Middle East, the energy sector is once again attracting a lot of attention. Standard oil stocks such as BP and Shell are well-positioned here, as they can align their output very precisely with market requirements. Special models such as Pure One are also coming onto the scene. Here, there are value clarifications that should accelerate the share price. With the SMR specialist Oklo, things are very volatile – this is a case where timing experts are needed in an overvalued stock.

Conflict of interest

Pursuant to §85 of the German Securities Trading Act (WpHG), we point out that Apaton Finance GmbH as well as partners, authors or employees of Apaton Finance GmbH (hereinafter referred to as “Relevant Persons”) currently hold or hold shares or other financial instruments of the aforementioned companies and speculate on their price developments. In this respect, they intend to sell or acquire shares or other financial instruments of the companies (hereinafter each referred to as a “Transaction”). Transactions may thereby influence the respective price of the shares or other financial instruments of the Company.

In this respect, there is a concrete conflict of interest in the reporting on the companies.

In addition, Apaton Finance GmbH is active in the context of the preparation and publication of the reporting in paid contractual relationships.

For this reason, there is also a concrete conflict of interest.

The above information on existing conflicts of interest applies to all types and forms of publication used by Apaton Finance GmbH for publications on companies.

Risk notice

Apaton Finance GmbH offers editors, agencies and companies the opportunity to publish commentaries, interviews, summaries, news and the like on news.financial. These contents are exclusively for the information of the readers and do not represent any call to action or recommendations, neither explicitly nor implicitly they are to be understood as an assurance of possible price developments. The contents do not replace individual expert investment advice and do not constitute an offer to sell the discussed share(s) or other financial instruments, nor an invitation to buy or sell such.

The content is expressly not a financial analysis, but a journalistic or advertising text. Readers or users who make investment decisions or carry out transactions on the basis of the information provided here do so entirely at their own risk. No contractual relationship is established between Apaton Finance GmbH and its readers or the users of its offers, as our information only refers to the company and not to the investment decision of the reader or user.

The acquisition of financial instruments involves high risks, which can lead to the total loss of the invested capital. The information published by Apaton Finance GmbH and its authors is based on careful research. Nevertheless, no liability is assumed for financial losses or a content-related guarantee for the topicality, correctness, appropriateness and completeness of the content provided here. Please also note our Terms of use.

Stockhouse does not provide investment advice or recommendations. All investment decisions should be made based on your own research and consultation with a registered investment professional. The issuer is solely responsible for the accuracy of the information contained herein. For full disclaimer information, please click here.