Author: Matt Oliver

As Asian demand for mining equities strengthens, Silvercorp’s proposed Hong Kong listing could broaden its investor base and support a valuation re-rating.

For years, Alibaba was one of the most important companies in China, yet much of its shareholder base sat thousands of miles away in New York. Investors debated Chinese consumer spending, Chinese regulation and Chinese economic growth from Manhattan conference rooms while the company itself remained woven into the daily habits of hundreds of millions of Chinese consumers.

Then Alibaba came to Hong Kong.

The business did not suddenly become more profitable. Its warehouses did not become larger. Its customers did not wake up richer. Yet the listing mattered because ownership and understanding moved closer together. A company long analysed from abroad became easier to own at home.

Markets like to believe prices reflect perfect information. More often, they reflect who is allowed to participate, who is paying attention and which investor base feels comfortable underwriting the risk.

Silver is beginning to show a similar fault line.

The metal is priced and traded globally, but a growing share of the pressure building beneath the market is Asian. Chinese and Indian buyers are increasingly relevant to investment demand. Yet many Western investors still treat silver as though the marginal buyers, marginal sellers are solely based in the west.

That assumption looks stale.

Silver is no longer being pulled by one source of demand. Industrial consumption has held up despite repeated warnings of economic weakness. Solar demand continues to absorb enormous quantities of metal. Electrification is not a slogan in this market. It has a physical bill of materials, and silver keeps appearing on it. At the same time, investment demand is reawakening across Asia, where precious metals occupy a deeper cultural and financial role than they do in most Western portfolios.

The market is being squeezed from two sides.

According to industry estimates, silver is heading towards its eighth consecutive annual supply deficit. Mine supply has been broadly stagnant for years. Scrap has helped, but not enough. The balancing item has been inventory, and inventory-based comfort has a habit of lasting until the moment it does not.

China is where that comfort starts to look most fragile.

China’s silver is no longer the world’s silver

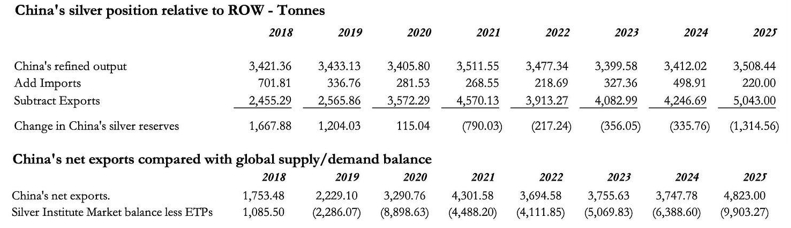

For years, China acted as an unofficial stabiliser of the global silver market. As one of the world’s largest producers, it supplied metal into international markets and, when required, drew down domestic inventories to satisfy global demand.

That arrangement appears to be weakening.

Recent import data suggest China has become a substantial net buyer of silver. New export licensing requirements have coincided with declining exports. The direction is not subtle. A country that spent years helping satisfy external demand now appears more focused on meeting its own industrial and strategic requirements.

The market becomes much harder to balance once a large source of marginal supply starts behaving like a buyer.

Deficits can persist for years when inventories are available. They become more dangerous when the inventory holder begins retaining metal rather than releasing it. The spike in London silver lease rates last year offered a brief look at what happens when physical availability tightens faster than paper markets expect.

At the same time, Asian investment demand may only be in the early stages of a new cycle.

Gold’s rise has created a familiar pattern. As gold becomes increasingly expensive, investors move down the precious metals curve in search of relative value. Silver has long benefited from that migration. In China and India, where precious metals are not treated merely as portfolio diversifiers but as monetary insurance, that shift can become powerful. Silver remains accessible in a way gold increasingly does not.

None of this requires a heroic price forecast.

It simply means that sizeable silver producers with long-life assets and operating leverage should be treated with more seriousness than they have received for much of the past decade. If China is consuming more silver while retaining more of its own supply, investors will begin paying more attention to companies positioned closest to that flow of metal.

This is where Silvercorp Metals (TSX:SVM) becomes more than a cheap mining stock with a good balance sheet.

A producer caught between two markets

Silvercorp Metals has spent years in an awkward corner of the mining market. It trades on the TSX and NYSE American. It reports to western investors. Yet most of its value comes from China, including the Ying Mining District, widely regarded as the country’s largest primary silver mine.

This has created a valuation problem that looks less operational than structural.

Western investors have often applied a discount to Chinese mining exposure almost by reflex. Some of that caution is understandable. Jurisdiction matters in mining. Governance, permitting, repatriation of capital and political risk are not footnotes. Yet Silvercorp’s operating history does not receive the valuation credit one would expect for a profitable, cash-generative primary silver producer with long-life assets and a strong balance sheet. The company also has a funded growth pipeline for global diversification.

Chinese and Hong Kong investors have historically had relatively limited access to Silvercorp despite the company operating some of China’s most significant silver assets. A Hong Kong listing would place the company in front of a much broader regional investor base that already follows mining companies closely.

The opportunity is therefore less about changing the business than broadening the audience able to evaluate it.

Its proposed Hong Kong listing could begin to correct that.

More than just another listing

A listing is easy to dismiss as paperwork. Another ticker. Another exchange. Another investor presentation.

In mining, venue matters more than that.

Capital markets are not neutral pipes. They sort companies into categories, shape the shareholder register and determine which investors see a stock often enough to form a view. Hong Kong’s renewed strength as a listing venue is therefore more than a background detail for Silvercorp. It is central to the thesis.

After several subdued years, Hong Kong has regained momentum as a serious capital market. New listings have drawn larger pools of capital, trading activity has improved and mainland participation has helped restore depth to areas of the market that had gone quiet. The mining sector has been one of the clearer beneficiaries.

The Hong Kong listings of Zijin Gold International and Chifeng Gold were watched closely for a reason. they showed that Chinese and Hong Kong investors continue to have strong demand for precious metals companies, those with assets and operating exposure already well represented in the region, but also with international growth aspirations. These were not obscure technology listings inflated by fashion. They were mining businesses attracting capital in a market that knows how to value resource exposure when the story sits close enough to home.

That is the difference.

Hong Kong and mainland investors are already active participants in valuing Chinese mining companies. While Silvercorp would still need to introduce its investment case through active marketing and investor engagement, a Hong Kong listing places the company in a market where investors are familiar with the sector and where demand for mining exposure has been strengthening.

Greater familiarity with the broader mining ecosystem does not eliminate investment risk, but it can influence how companies are valued relative to comparable businesses.

Silvercorp’s proposition is unusually clean.

It would become the only primary silver producer listed in Hong Kong.

Scarcity has a real price in capital markets, particularly when it gives investors a direct route into a theme they otherwise struggle to express. Hong Kong investors have access to gold producers, industrial metals companies and diversified miners. They do not have a direct equivalent to Silvercorp.

If silver continues to attract greater investor attention across Asia, that absence could become increasingly significant.

At some point, the numbers start arguing back

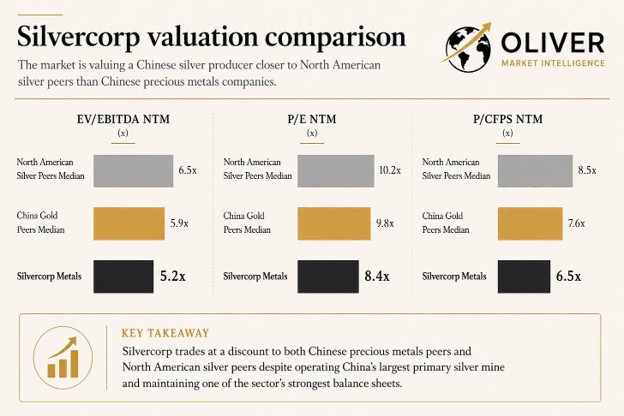

The valuation gap is not subtle.

Compared with Chinese precious metals peers, Silvercorp trades at lower earnings, cash flow and EV/EBITDA multiples. The discount is also visible against North American silver producers, despite Silvercorp’s scale, operating record and balance sheet strength.

On forward EV/EBITDA, Silvercorp trades at roughly 5.2x compared with approximately 6.1x for North American silver peers and around 7.0x for Chinese precious metals peers. Similar gaps appear across earnings and cash flow metrics. On forward earnings, Silvercorp trades near 8.4x, while peer averages sit comfortably above that level.

The valuation gap reflects, at least in part, the different investor bases that currently dominate each market.

Western investors have historically applied a discount to companies with significant China-based assets. By contrast, Chinese precious metals companies listed in Hong Kong and mainland markets have generally traded on higher valuation multiples.

A Hong Kong listing gives Silvercorp access to an additional investor base rather than replacing its existing one. If that broader pool of investors values the company more in line with comparable Chinese precious metals producers, the current discount could begin to narrow.

Importantly, a stronger valuation in Hong Kong could also increase visibility among North American investors. As liquidity improves and valuation moves closer to Chinese peer levels, the company may attract greater attention from investors who already value primary silver producers on higher multiples.

A balance sheet built for growth

Valuation discounts are easier to defend when a company is overleveraged, operationally stretched or dependent on a single speculative catalyst. Silvercorp does not fit that pattern.

The company ended its most recent quarter with approximately US$422 million in cash. It carries US$150 million in convertible debt, convertible at US$4.63 per share until 2029 and comfortably in the money at current levels. More recently, it secured roughly US$220 million through a Standard Chartered Hong Kong term loan, which remains undrawn.

For a mid-tier silver producer, that is a serious balance sheet.

It matters because Silvercorp is no longer only a China operating story. The pipeline now includes El Domo and Condor in Ecuador, projects in Kyrgyzstan and strategic investments elsewhere. Even so, the foundation remains Ying: scale, reserve longevity, stable costs and a long history of replacing mined reserves.

This is not an exploration promotion hoping the next drill hole changes the market’s mind.

It is an operating business with cash flow, funding and multiple ways to grow. In a stronger silver market, that combination should not trade as though investors are doing the company a favour by noticing it.

Expanding access to capital

A Hong Kong listing will not mechanically erase Silvercorp’s discount. Markets rarely behave so politely.

But it could remove one of the more obvious structural barriers to a re-rating: limited access to a broader pool of investors.

Listings influence more than where shares trade. They affect visibility, analyst coverage, liquidity and the range of investors able to participate. By expanding rather than replacing its shareholder base, Silvercorp has an opportunity to improve all four.

Mining valuations are not set by fundamentals alone. Coverage matters. Trading depth matters. Once a company appears on the screens of investors who previously had limited access to it, the conversation can change. Not always. Not instantly. But often enough that dismissing the listing as administrative would miss the point.

Silvercorp: Primary ownership

Silvercorp shares remain roughly 38% below their 52-week high. Several peers are similarly below prior peaks. This is not a market pricing perfection.

The silver market itself is no longer behaving like the old category. China’s role is changing. Asian investment demand is strengthening. Physical availability appears tighter than headline supply numbers suggest. Against that backdrop, one of the few sizeable primary silver producers with deep operational roots in China is preparing to list in the market where investor appetite for mining companies has been improving.

Silvercorp’s mines will look exactly the same the day after a Hong Kong listing. Its reserves will not suddenly increase, nor will its processing plants produce more silver simply because a new exchange begins trading its shares.

What could change is the range of investors able to own the company.

Today, Silvercorp is primarily followed by North American investors despite operating some of China’s largest primary silver assets. A Hong Kong listing would not replace that shareholder base. Instead, it would broaden it by giving Hong Kong and mainland investors a more direct route to invest alongside existing shareholders.

That broader investor base matters because different markets often value comparable businesses differently. Chinese precious metals companies have generally traded on higher multiples than companies with similar China-based assets listed only in North America. If Silvercorp can narrow part of that valuation gap through greater visibility, stronger liquidity and increased participation from Asian investors, the shares could begin to rerate toward Chinese peer valuations.

Such a rerating would not necessarily stop there. A stronger valuation and more liquid trading could also attract greater interest from North American investors, particularly those already prepared to pay higher multiples for quality silver producers. Over time, that combination could help close the remaining gap with North American silver peers as well.

Alibaba’s Hong Kong listing did not change the business it owned. It expanded the range of investors who could own it.

Silvercorp’s opportunity is similar. The business already exists. The assets are already operating. The opportunity lies in broadening the shareholder base, improving liquidity and allowing a wider range of investors to decide what those assets are worth.

Join the discussion: Find out what everybody’s saying about this mining stock on the Silvercorp Metals Inc. Bullboard and check out Stockhouse’s stock forums and message boards.

{kind=link}